DOWNLOAD A PDF OF THIS REPORT pdf(0.1MB)

Contact

Eric HoskenPartner [email protected] 212-921-9363 Kelly Malafis

Founding Partner [email protected] 212-921-9357

Highlights

- IPO compensation practices vary by industry, with higher cash compensation in more mature industries and greater equity compensation in high-growth Biotech and Internet companies

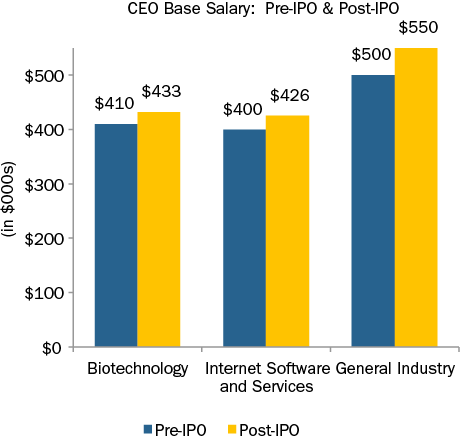

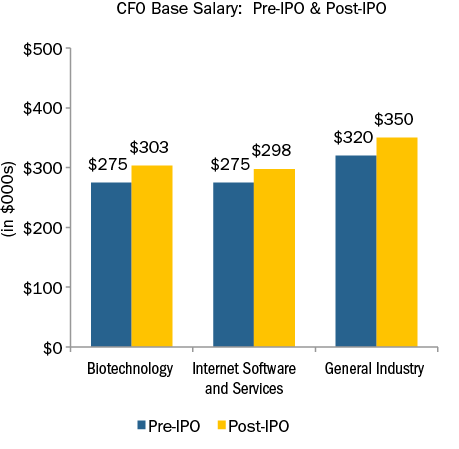

- Base salaries for CEOs in Pre-IPO Biotech, Internet, and General Industry companies are, at median, $410k, $400k, and $500k, respectively; for CFOs, base salaries are $275k, $275k, and $330k, respectively

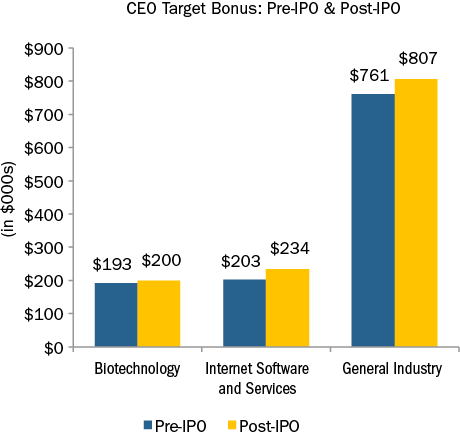

- 82% of Biotech companies and 52% of both Internet and General Industry companies have an annual target bonus for the CEO; of these companies, the median target bonus as a percent of base salary is 50%, 50%, and 100%, respectively

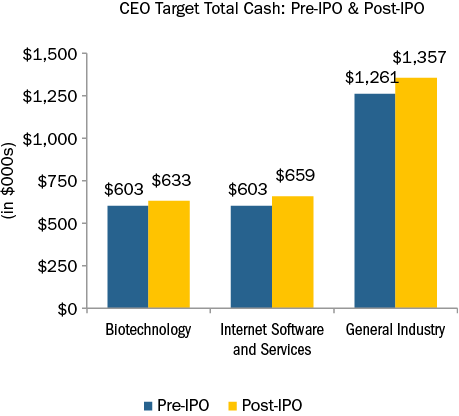

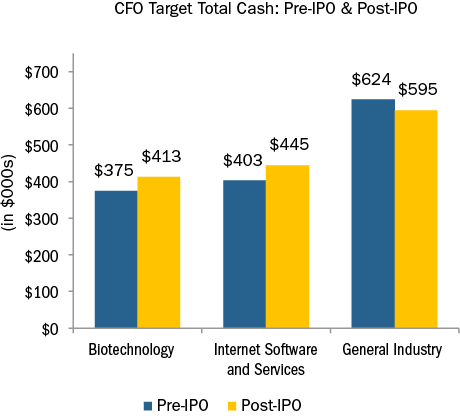

- Total Cash Compensation for CEOs in Pre-IPO Biotech, Internet, and General Industry companies is approximately, at median, $600k, $600k, and $1.24M, respectively; for CFOs, total cash compensation is approximately, at median, $375k, $400k, and $590k, respectively

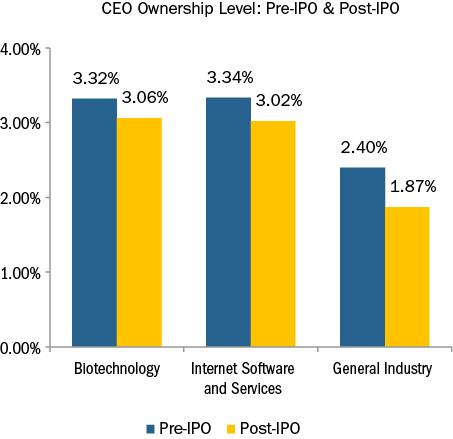

- Typical CEO equity ownership for Biotech and Internet companies is approximately 3.3% at median; CEO ownership in General Industry companies is slightly lower, at approximately 2.8% at median

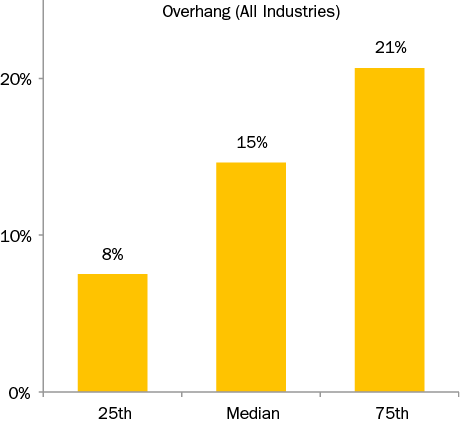

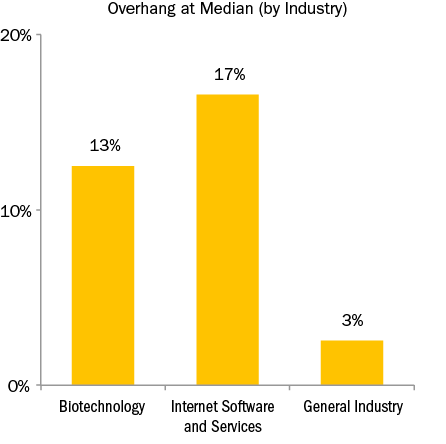

- Median total potential dilution (overhang) at the time of the IPO for all of the companies researched is approximately 15%, with many companies having overhang levels of 25% or greater; overhang levels for Biotech & Internet companies are higher than General Industry

Introduction

In 2014, the number of Initial Public Offerings (“IPOs”) reached its highest level in the United States since the early 2000’s. Compensation Advisory Partners (“CAP”) has reviewed a subset of companies in the Biotechnology (“Biotech”), Internet Software & Services (“Internet”) and General Industry1 (a cross-industry sample) that went public over the last two years (beginning January 1, 2013) to analyze the trends in executive compensation Pre-IPO. Additionally, CAP reviewed compensation levels for these companies Post-IPO.

Who / WHat we studied

CAP’s research includes data from 21 Biotech companies (median revenue = $15M), 22 Internet companies (median revenue =$158M), as well as a look into 22 companies in General Industry ($458M)2. Within the set of companies studied, CAP analyzed cash and equity compensation levels and pay practices pre-IPO (IPO Registration Statements – 424B) and post-IPO (Definitive Proxy Statements – DEF14A).

CASH COMPENSATION

Base salaries of CEOs and CFOs Pre-IPO in General Industry tend to be higher than those in the Biotech and Internet industries. One reason for the higher salaries may be attributed to the relative size and maturity of the companies; additionally, Biotech and Internet Companies typically focus their compensation packages on granting more equity than cash, given their strong growth prospects.

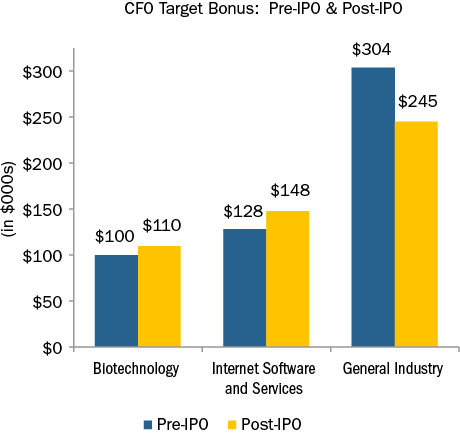

Similar to the trend in base salaries, target bonuses for CEOs and CFOs in General Industry tended to have higher bonuses as a percent of base salary than in the Biotech and Internet industries. Typical target bonus percentages for CEOs are 50% of base salary in the Biotech and Internet industries, and 100% of base salary in General Industry. CFOs in the Biotech, Internet, and General Industry have target bonus percentages of 35%, 50%, and 60%, respectively.

CAP found that bonus targets generally increase and there is a slight shift of plans from a discretionary model to a formulaic annual bonus plan / goal attainment approach following an IPO. The percentage of companies with target bonus percentages in place for CEOs increased after IPO from 82% to 86%, 52% to 62%, and 52% to 65% in the Biotech, Internet and General Industry, respectively. The shift is primarily driven by expectations of more sustainable growth in financial metrics and ability to set short-term goals.

Consistent with the findings that base salaries and target bonuses tend to be higher in General Industry, target total cash compensation is higher at median as well ($1.24M in General Industry companies compared to $603k in both Biotech and Internet companies for CEOs; $588k in General Industry companies compared to $375k and $400k in Biotech and Internet companies for CFOs).

EQUITY COMPENSATION

For early stage companies, equity grants are typically analyzed as a percentage of the company’s total shares outstanding, rather than a grant date value, as the company’s value pre-IPO is often significantly below the value at the time of the IPO. For our study, CAP analyzed the equity ownership levels that CEOs and CFOs had Pre-IPO and Post-IPO.

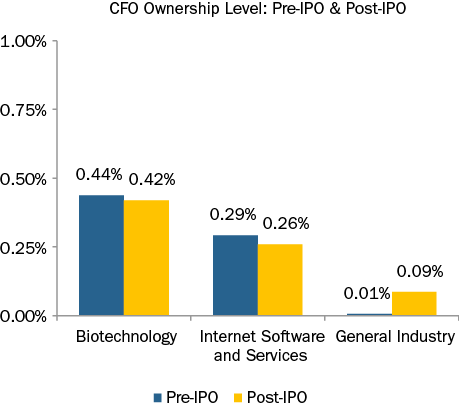

In the Biotech and Internet industries, CEOs have median ownership of over 3.3% of the common shares outstanding (“CSO”) pre-IPO. This is higher than the ownership levels for the CEOs in General Industry companies, as the median ownership is approximately 2.75%. A similar trend was found for CFOs, with median equity ownership levels of .44%, .29%, and .02% in the Biotech, Internet, and General Industry companies, respectively. Post-IPO, equity ownership levels generally decrease, reflecting dilution from the additional shares issued by companies at the IPO.

Median total potential dilution (or overhang) at the time of the IPO for all of the companies researched is approximately 15%, with many companies having overhang levels of 25% or greater. There are typically large numbers of conversions of shares from executives and other individuals (founders, other investors, etc.) that increase the number of shares outstanding upon an IPO. Companies pre-IPO will also generally authorize a larger number of shares for their equity plans as there is less resistance from shareholders or proxy advisory firms, which allows the company to have more flexible plan features.

TRENDS IN COMPENSATION

The trends CAP studied in terms of cash compensation are consistent with what we would expect from companies that recently filed their IPO. Base salary and target bonus are typically lower in smaller Biotech and Internet Service companies as they focus on equity compensation to conserve cash and promote growth in their companies. When a company becomes public they will increase the amount of shares outstanding during the offering, which dilutes current shareholders of the company. The one exception that we saw was with CFOs in the General Industry companies. Oftentimes Pre-IPO, CFOs received either very small, or no equity grants, leaving them with very low numbers of ownership levels. Upon IPO and the months after, companies started to grant CFOs more significant levels of equity, increasing their ownership.

Options are the most frequently used vehicle when granting equity to executives Pre-IPO within the Biotech and Internet companies (95% and 86%, respectively). These companies typically have lower revenue, so the option grants may reflect growth prospects within these companies. Surprisingly, only 48% of companies in the General Industry companies granted options. In some instances, restricted stock is the preferred equity vehicle of these companies and in other instances there was no equity granted at all. The companies that did grant restricted stock tended to be more mature and larger in size where options may not be as attractive.

CONCLUSION

The increase in IPO activity over the last few years is an exciting development. For companies approaching IPO, it is critical to ensure that the pay program is adequately competitive to motivate and retain key employees, as well as being responsible from the perspective of the company’s new public shareholders. For high-growth companies in the Biotech and Internet industries, IPO pay practices are similar to what we saw in the peak of the tech boom; however, when companies in a more mature business position go public, their pay practices are more comparable to the broad market pay practices we see in established public companies. For more information on IPO pay practices, or for assistance in transitioning to a public company pay program, please contact CAP directly.

|

List of Companies |

||

|

Biotechnology |

Internet Software & Services |

General Industry |

|

Acceleron Pharma, Inc. |

Barracuda Networks, Inc. |

American Homes 4 Rent |

|

ADMA Biologics, Inc. |

Benefitfocus, Inc. |

Armada Hoffler Properties, Inc. |

|

Agios Pharmaceuticals, Inc. |

Care.com, Inc. |

Aviv REIT, Inc. |

|

BIND Therapeutics, Inc. |

Cvent, Inc. |

Boise Cascade Company |

|

bluebird bio, Inc. |

Cyan, Inc. |

CDW Corporation |

|

Cancer Genetics, Inc. |

Endurance International Group, Inc. |

Chegg, Inc. |

|

Cara Therapeutics Inc. |

FireEye, Inc. |

Diamond Resorts International, Inc. |

|

Cellular Dynamics International, Inc. |

Gigamon Inc. |

Emerge Energy Services LP |

|

Chimerix, Inc. |

Gogo Inc. |

Empire State Realty Trust, Inc. |

|

Eleven Biotherapeutics, Inc. |

Marin Software Incorporated |

EP Energy Corporation |

|

Enanta Pharmaceuticals, Inc. |

Marketo, Inc. |

Fox Factory Holding Corp |

|

Epizyme, Inc. |

Model N, Inc. |

Houghton Mifflin Harcourt Company |

|

Five Prime Therapeutics, Inc. |

Professional Diversity Network LLC |

Installed Building Products, Inc. |

|

Foundation Medicine, Inc. |

RetailMeNot, Inc. |

Ladder Capital Corp |

|

GlycoMimetics, Inc. |

Rocket Fuel Inc. |

LDR Holding Corporation |

|

INSYS Therapeutics, Inc. |

Silver Spring Networks, Inc. |

Norwegian Cruise Line Holdings Ltd. |

|

Intrexon Corporation |

Textura Corporation |

RingCentral, Inc. |

|

MacroGenics, Inc. |

Tremor Video, Inc. |

SFX Entertainment Inc. |

|

Onconova Therapeutics, Inc. |

Twitter, Inc. |

Sprague Resources LP |

|

PTC Therapeutics, Inc. |

Viggle Inc. |

Stonegate Mortgage Corporation |

|

Receptos, Inc. |

Xoom Corporation |

UCP, Inc. |

|

YuMe, Inc. |

Violin Memory, Inc. |

|