Management Say-on-Pay Proposals (U.S.)

ISS will recommend voting against advisory Say on Pay resolutions related to executive compensation if there is a perceived misalignment between CEO pay and company performance, based on both quantitative tests and a qualitative review of the pay program and related Compensation Committee decisions.

ISS is considering the following policy change for 2014:

Simplify the methodology for calculating the Relative Degree of Alignment (RDA) pay-for-performance screen. The proposed new methodology is to calculate the difference between the subject company’s TSR rank and the CEO’s total pay rank within a peer group, as measured over a three-year period (or for as many fiscal years that the company has been publicly traded and has disclosed pay data, if less than three years).

Currently the RDA screen is calculated as the difference between the company’s TSR rank and the CEO’s total pay rank within a peer group, as measured over one-year and three-year periods. The one-year and three-year periods are weighted 40% and 60%, respectively.

ISS Request for Comment – Proposed RDA Policy Change

Are there circumstances under which performance or pay from the most recent year should weigh more heavily in a pay-for-performance analysis?

CAP Perspective: We agree with ISS’ preliminary decision to apply a longer-term focus to the quantitative RDA test; i.e., solely a three-year timeframe for both pay and performance. However, we believe that recent Committee decisions best relate to company performance over time. We urge ISS to state that the qualitative assessment will place particular emphasis on recent Committee decisions that apply prospectively in a year following:

- Below par shareholder support for an advisory Say on Pay resolution (less than 70%)

- A CEO transition

- A corporate transformation (merger, major acquisition, etc.)

We also urge ISS to use realizable pay in the RDA test (with ISS’ current definition and assumptions), instead of grant date pay. Realizable pay would better show if pay was aligned with performance over time. This methodology change could also apply to the PTA test.

Finally, we urge ISS to address the following questions and concerns in its 2014 policy release.

- Under the ISS 2014 policy, as proposed, a three-year point-to-point TSR will be used for the quantitative RDA test, which in practice reflects a compound annual growth rate. This approach could lead to volatile RDA results since it uses a single day as the starting point and ending point in the performance analysis. An alternative approach that ISS should consider is to calculate TSR using the average starting and ending stock prices over a 20-trading-day period. This will reduce volatility and add credibility to the results.

- ISS should also consider adopting an alternative approach for calculating TSR performance that reflects the average relative position of TSR during each of the three most recent one-year periods, rather than a compound annual growth rate. Looking at performance trends over multiple time periods may yield additional insight into performance and related pay decisions.

- Also under the ISS 2014 policy, as proposed, three-year average (arithmetic mean) compensation will be used in the RDA test. We support this approach, but certain issues should be acknowledged. This approach does not fully address the problematic timing of proxy reporting where a Compensation Committee evaluates performance in the year just ended and makes a long-term incentive award in the beginning of the following year. This award is reported in the proxy in the following year and does not impact ISS’ analysis. We urge ISS to acknowledge that this timing (reporting) difference will be considered in its qualitative assessment of the pay program and related decision making. Given the imperfections in the compensation data analyzed, we support the simple, straightforward approach that is proposed for the compensation data included in the RDA quantitative test that focuses solely on a longer time horizon vs. the current approach. The approach, as proposed, will also smooth out some of the extremes seen in individual years.

- We ask ISS to provide its reasoning as to why it is appropriate to weigh recent pay and performance more in the PTA test, but not in the RDA test. Why does it make sense for these tests to incorporate inconsistent timeframes and weightings?

ISS Request for Comment – Proposed RDA Policy Change (cont’d)

Are there any unintended consequences from using a simple, unweighted three-year pay and performance measure as the basis for the RDA screen?

CAP Perspective: We believe the proposed approach for performance measurement is potentially too volatile since it depends heavily on a single “start” point and a single “end” point.

As stated above, we urge ISS to use an average stock price at the beginning and end points of the TSR calculations for its pay versus performance tests, which would align with methodology used in the ISS SVT tool. We believe that use of a 20-trading-day average stock price would limit the impact of very short-term stock price fluctuations on the results.

A second alternative, also noted above, would be to use the average relative position of TSR during each of the three most recent one-year periods, rather than a compound annual growth rate. This would be beneficial since it would reduce volatility in the TSR calculation.

ISS Request for Comment – Other

Please feel free to add any additional information or comments on the proposed policy change.

CAP Perspective: We have additional comments that relate to ISS Say on Pay vote recommendations. Outlined below, we describe additional changes that we urge ISS to consider.

RDA and PTA Tests – Time Period

We urge ISS to provide its reasoning for why the timeframe used for the RDA quantitative test (three years) is different than the timeframe used for the PTA quantitative test (five years). Why is the use of inconsistent time frames appropriate?

RDA Quantitative Thresholds

ISS has indicated that the thresholds for the Medium and High level of quantitative concern have not yet been set by ISS Research for 2014 pay vs. performance analyses. We urge ISS to expand the thresholds for the RDA test so that fewer companies are flagged with “Medium” or “High” concern levels and, in turn, increase consistency between the RDA test and the PTA test.

In the December 20, 2011 ISS white paper titled “Evaluating Pay for Performance Alignment”, in the “Back-testing the Measures” section, a table was included:

|

Measure |

Level that may trigger high concern in conjunction with other measures (“Medium” concern) |

Level that triggers high concern by itself |

|

RDA |

-30 (~25th percentile) |

-50 (~10th percentile) |

|

MOM |

2.33x (~92nd percentile) |

3.33x (~97th percentile) |

|

PTA |

-30% (~10th percentile) |

-45% (~5th percentile) |

As shown above, 1 in 4 companies is expected to receive “Medium” concern from the RDA test, but only 1 in 10 companies is expected to receive “Medium” concern from the PTA test.

- We believe the amount of companies expected to receive “Medium” and “High” concern within each of ISS’ quantitative screens should be more consistent

- We find the thresholds (~10th percentile and ~5th percentile) in the PTA test to be most reasonable to identify outliers, and believe expecting one in four companies to receive “Medium” concern from the RDA test is unreasonably high

Performance Goals – Evaluation of “Rigor”

ISS reviews the rigor of performance goals in its qualitative pay-for-performance assessment. We urge ISS to be more transparent regarding the parameters for this assessment.

Multi-year Long-term Grants

When recruiting new CEOs, companies often grant long-term incentives that are intended to make up for compensation forfeited from a previous employer (often called “make-whole” grants). In these instances, we urge ISS to exclude these grants from the pay-for-performance testing since the grants fill a very specific need and would not be granted in the absence of forfeited compensation.

Time-based Stock Options

In our experience, many investors and most corporate directors view time-based stock options as a performance-based long-term incentive vehicle; i.e., they disagree with ISS’ classification of this form of compensation as “non-performance-based pay”. We urge ISS to include questions on this topic in its next policy survey.

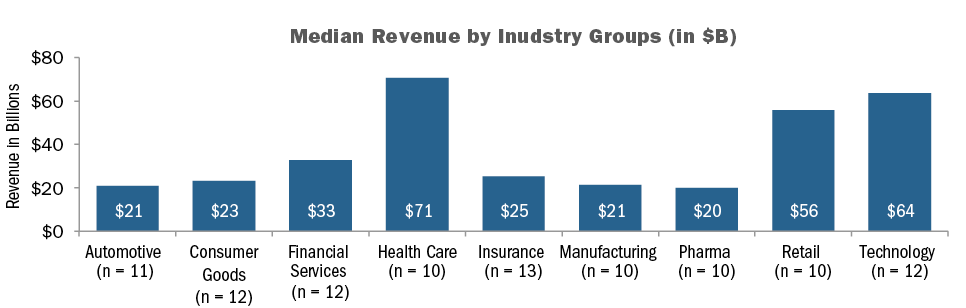

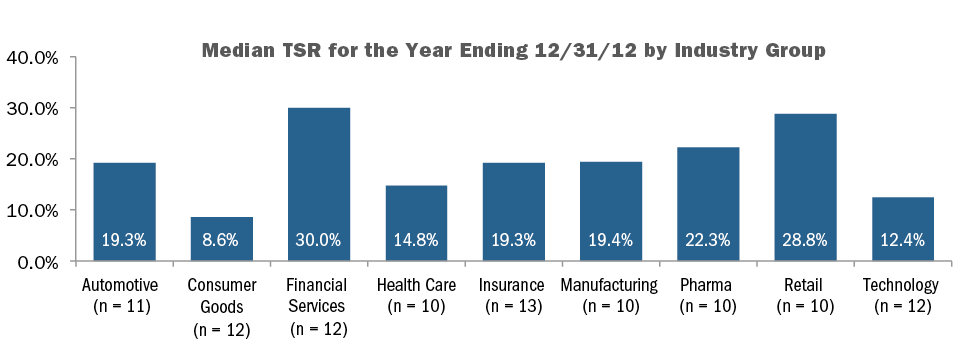

Among the 100 company sample, median revenue was $33B, median market capitalization was $37B and median Total Shareholder Return (TSR) was 19% in 2012. As indicated in the charts below, there is significant variation in company size and performance by industry.

COMPENSATION PHILOSOPHY

Nearly 60% of companies in our study disclose a target total pay position for the Named Executive Officers (“NEOs”). Of these companies, approximately 75% target total pay at median, up from 60% a year ago; indicating that companies are shifting their compensation pay philosophy to a market median standard in reaction to increased scrutiny from shareholders and proxy advisory firms.

|

Target Total Compensation Pay Positioning (n=57) |

CEO |

CFO |

|

Below Median |

1% |

0% |

|

At Median |

74% |

75% |

|

Above Median |

25% |

25% |

CAP Perspective: Change in targeted pay position to median reflects movement to adopt more conservative target pay practices that demonstrate a strong link to performance.

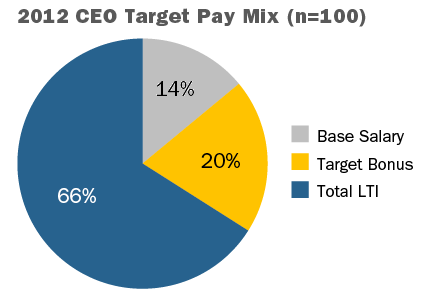

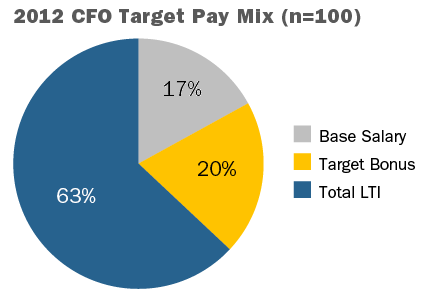

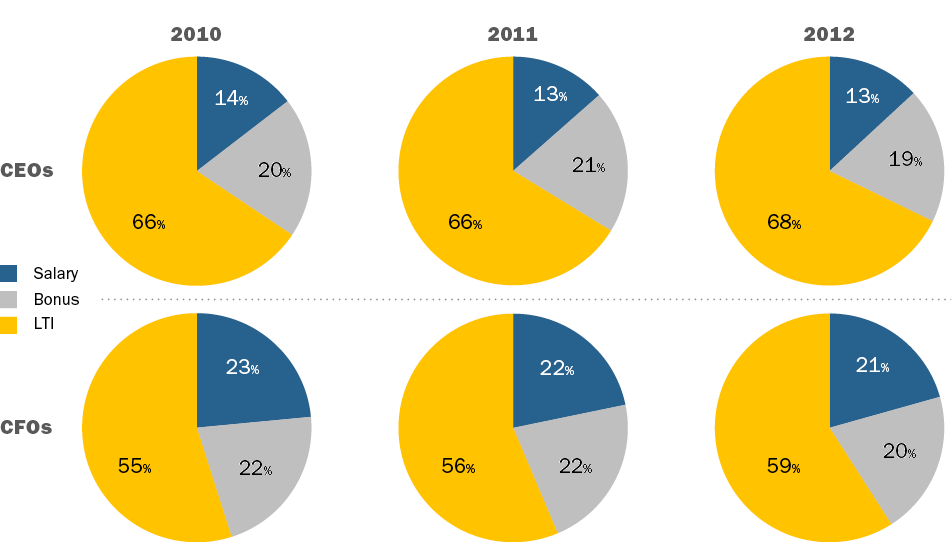

PAY MIX

Overall, companies did not make significant shifts in the total pay mix in 2012 vs. 2011. CEO and CFO total pay continues to place significant emphasis on long-term incentives (“LTI”); on average, LTI reflects 66% of pay for CEOs and 63% for CFOs.

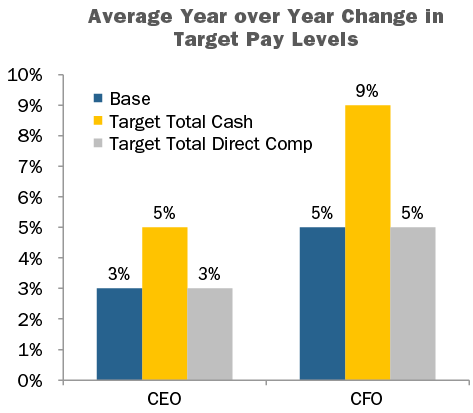

CHANGES IN TARGET PAY LEVELS

The chart below shows average year over year change in target pay levels for CEOs and CFOs in our study.

Note: Excludes newly hired/promoted executives and one-time sign-on/retention equity awards. Percentages include zeroes.

CAP Perspective: We see increases in target pay levels in the low single digits, though the most significant increase is in target annual incentive opportunities suggesting that companies are increasing performance-based pay to reinforce the pay-for-performance link.

Base Salary

CEO base salaries in 2012 increased 3%, on average, though only 46% of companies provided salary increases. Base salaries for CFOs increased by 5% though fewer companies provided an increase in 2012 (68%) vs. 2011 (78%) suggesting salary increases were made less frequently for senior executives than other employees.

Executives in the Health Care and Pharmaceutical industries were more likely to receive a salary increase (70% of CEOs in the Health Care industry and 90% of CFOs in the Pharmaceutical industry) than those in other industries. Financial Services, Insurance and Technology industries were less likely to provide a salary increase for the CEO in 2012.

|

Base Salary Action |

CEO |

CFO |

||

|

2012 |

2011 |

2012 |

2011 |

|

|

Increase |

46% |

47% |

68% |

78% |

|

No Change |

52% |

50% |

26% |

20% |

Note: Does not include newly hired CEOs or CFOs. Therefore, percentages do not add up to 100%.

Target Bonus

Target bonus for both the CEO and CFO increased modestly at median levels. At the 75th percentile, the bonus opportunity for CFOs increased by almost 20 percentage points. Target bonuses for CEOs in the Automotive, Consumer Goods and Technology industries increased the most in 2012. CFOs in the Automotive, Retail and Technology industries saw significant increases as well.

|

Summary Statistics |

Target Bonus as a % of Salary |

|||||

|

CEO |

CFO |

|||||

|

2012 |

2011 |

Change in %age Pts. |

2012 |

2011 |

Change in %age Pts. |

|

|

75th Percentile |

200% |

200% |

0% |

143% |

125% |

+18% |

|

Median |

157% |

153% |

+3% |

103% |

100% |

+3% |

|

25th Percentile |

133% |

135% |

-2% |

90% |

85% |

+5% |

Target Total Cash Compensation

Target total cash compensation increased for both the CEO (5%) and CFO (9%) in 2012, mainly due to increases in annual incentive opportunities.

Total Long-term Incentives (LTI)

Increases in total LTI in 2012, on average, were fairly modest; total LTI increased by 3% for CEOs and 5% for CFOs. However, some industries saw significant increases in LTI year over year: CEOs in the Health Care and Consumer Goods industries, on average, received increases in LTI of 30% and 20%, respectively. CFOs in the Technology and Retail industries received the highest increases of 24% and 9%, respectively.

Target Total Compensation

Target total compensation increased over 2011 levels primarily through increases in target annual incentives and, in some industries, through increases in LTI. These findings varied by industry. Financial Services, Pharmaceutical and Retail companies, on average, provided the most significant increases in target annual incentives over other pay components, while Consumer Goods and Health Care industries had the greatest increase in target LTI opportunities.

CONCLUSIONS

Overall, companies had modest increases in target pay levels for the CEO and CFO, through changes in annual and long-term incentives. The Consumer Goods and Health Care industries saw increases in the 15%-20% range driven by higher LTI opportunity while other industries saw more modest changes in total pay levels. Compensation philosophies continue to migrate to median as companies adopt a more conservative pay philosophy. Overall pay mix for the CEO continues to maintain a strong LTI component (66% of pay) with salary representing smaller component of pay (14%), on average. We expect shareholders and proxy advisory firms to continue to influence company pay strategy, as companies to continue to provide modest increases in target total pay mainly through incentive compensation.

|

Industry |

Average Year over Year Change in CEO Target Pay – Top 3 Industries and Overall Sample |

|||

|

Base |

Target Bonus |

LTI |

Target Total Compensation |

|

|

Health Care |

2% |

4% |

30% |

19% |

|

Consumer Goods |

3% |

13% |

20% |

17% |

|

Automotive |

4% |

7% |

7% |

6% |

|

Overall Sample |

3% |

8% |

3% |

3% |

Competitive benchmarking is a critical step in the development of executive compensation programs. Companies typically define their pay philosophies, benchmark competitive pay and practices, design incentive programs and then set pay levels accordingly. Until recently, competitive benchmarking was one of the least contentious steps in the whole process.

Those days are over. Recent corporate governance reports criticized sloppy competitive pay benchmarking practices. One issue with competitive benchmarking is the fact that nearly all companies position executive compensation at median or above. In this case, the competitive data artificially escalates year after year. Second, many governance experts believe that compensation committees have relied too heavily on benchmarking studies and have failed to apply good judgment to the numbers.

Despite the recent backlash, executive compensation benchmarking remains a useful tool when it is carefully executed and balanced with other reference points. Some of the most common—and avoidable—benchmarking pitfalls we see:

- Selection of the screening criteria that will produce an appropriate benchmarking peer group

A variety of criteria can be considered, including industry, size, business economics, business focus, business strategy, common pool for management talent, historical performance and geography. Identification of the critical screening criteria will lead to relevant peer group selection.

- Review and selection of compensation surveys

Just as selecting peers is critical, so is the choosing the appropriate published surveys. Several factors should be considered, including the participation of direct peer or comparison firms, the availability of necessary data (for example, salary, bonus and long-term incentives) and the presence of relevant data cuts. It’s also important to review survey methodology to ensure consistency of approach when multiple surveys are used (three sources per position is ideal).

- Blending proxy and survey data

Several pitfalls can arise when combining proxy and survey data: overweighting proxy data for some positions, using survey or proxy data that are outliers relative to other data sources, and overweighting sources with a small sample size. Look for large enough sample sizes and consistent data and assess whether the data you review is reasonable as part of your assessment.

- Actual versus target bonuses

When analyzing competitive bonus levels, it is important to consider whether the competitive data is reporting target or actual bonus levels. If your company is lagging the industry, target bonus levels may be preferable for the analysis. Your company may provide a competitive target opportunity, but actual payouts are lagging, as they should, because of performance.

For companies challenged by these and other pitfalls or those who do not want to rely entirely on benchmarking to set their executive pay levels, other analyses can be conducted:

- Reviewing internal equity to ensure relative pay levels are reasonable

- Taking performance into account when determining executive pay levels

- Using wealth-accumulation analysis to assess the richness of executive compensation practices

While these analyses are quantitative and number-driven, they too depend heavily on subjectivity and judgment. Selecting the benchmarking approach that’s right for your organization requires an understanding of various resources and methodologies available and the application of them in the context of your business. Despite recent criticisms, competitive pay benchmarking continues to be a useful tool, although it is admittedly an imperfect one.

The full article entitled “The Devil is in the Details: Analytical Pitfalls in Executive Compensation Benchmarking”, written by Bonnie Schindler, appears in the recently published book Survey Best Practices: A Collection of Articles from WorldatWork.

Notable Findings

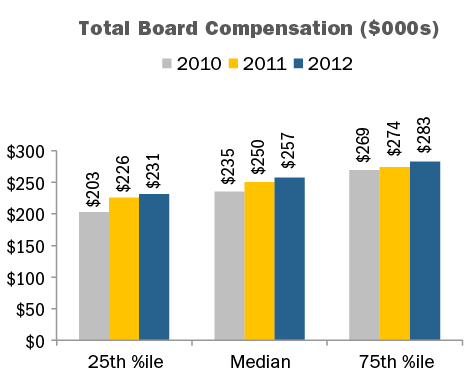

Total Board Compensation

At median, non-employee director compensation increased three percent in 2012, to $257K, after a six percent increase in 2011 and a flat period in 2010. Year-over-year, median Total Board Compensation increased from $250,000 to $257,0003.

In line with emerging practices, large companies are relying on annual retainers to compensate outside directors. Use of Board meeting fees remained a minority practice in 2012, with only 18 percent of companies paying board meeting fees. This is similar to 2011 and 2010, where 19 percent and 23 percent of companies provided meeting fees, respectively.

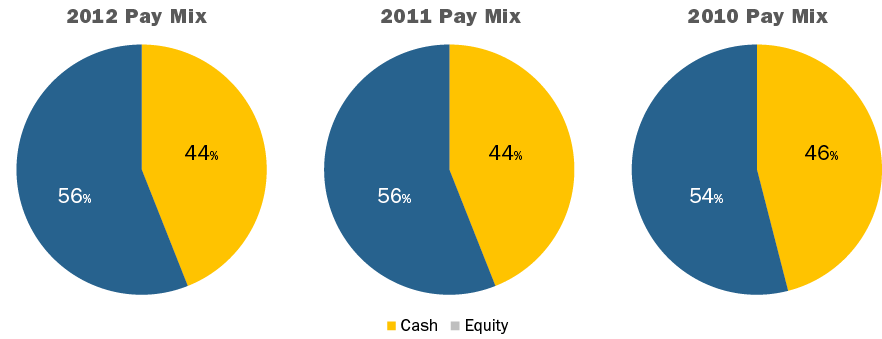

Pay Mix

The mix of cash and equity paid to outside directors was generally consistent between 2010 and 2012. On average, the majority of compensation delivered to directors continues to be in the form of equity.

Equity Compensation

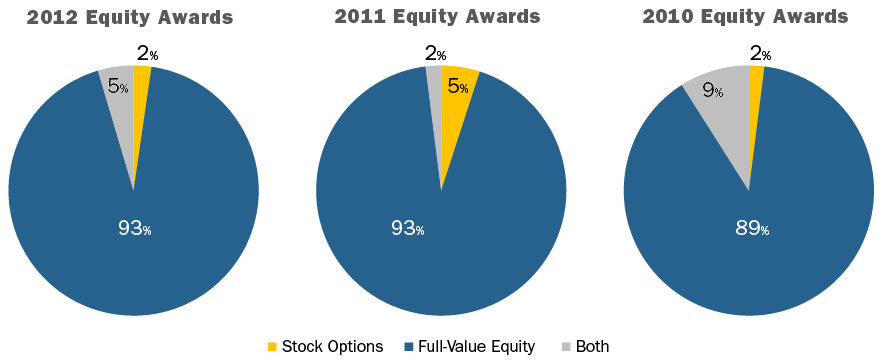

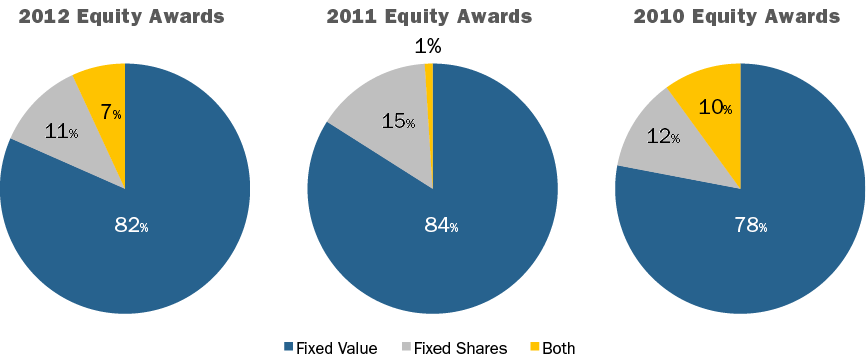

Full-value share equity, including restricted stock units, restricted stock, deferred stock units and outright awards of common stock, continues to be by far the most common form of equity delivered to non-employee directors, with only seven percent of companies using stock options as part of the director compensation package.

In the recent years, equity awards denominated as a fixed value increased in prevalence, as opposed to awards based on a fixed number of shares.

CAP Perspective: Over the next few years, we expect the following changes in director compensation to take place: 1) low-to-mid single-digit annual increases in Total Board Compensation; 2) more companies moving to fixed retainer pay structures with a component in cash and a component in equity as opposed to paying meeting fees; and 3) a continued emphasis on full-value equity awards. Delivering a majority of compensation in the form of equity coupled with stock ownership / retention requirements creates strong alignment with long-term shareholders and is considered a best practice.

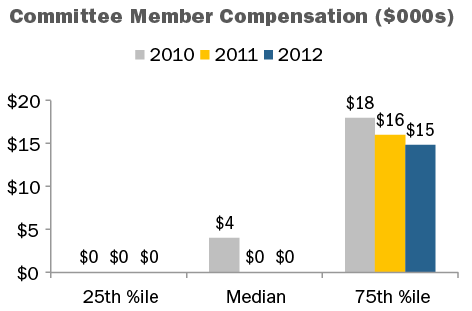

Committee Compensation

Companies have de-emphasized committee member compensation, instead focusing on overall Board compensation. Our research found that just over 50 percent of companies pay no committee-specific fees to members of any of the three major committees4, similar to 2011 and up from just over one-third in 2010. Since a slight majority of companies do not pay separate fees for committee service, at median committee member compensation is now $05. Among companies that do pay separate fees for committee service, median committee member compensation is $16K.

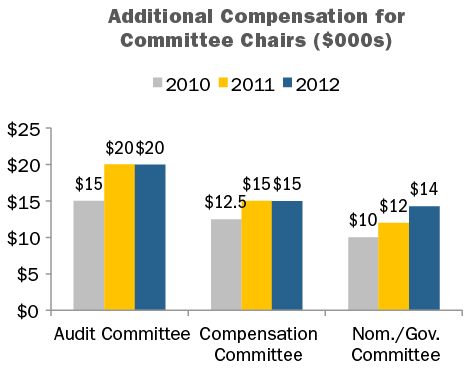

From 2011 to 2012, median additional compensation for committee Chairs remained flat for the Audit and Compensation committees, and increased +17 percent for the Nominating / Governance Committee. Relatively flat year-over-year changes may be associated with a better understanding of the time requirement of the leadership role versus that of a committee member.

CAP Perspective: We expect the trend away from committee member fees to continue, at a slow-to-moderate pace, with the value being rolled into Board cash or equity retainers.

Serving as a committee Chair is generally viewed as a Board leadership role, with additional time requirements, responsibilities, and reputational risk; as a result, additional compensation is often provided for the role.

Near-term, we expect a differential to continue between the additional compensation paid to the Chair of the three major board committees.

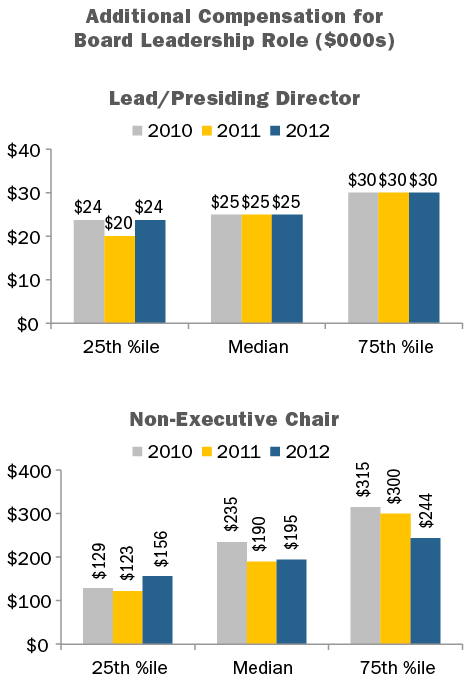

Lead/Presiding Directors and Non-Executive Chairmen of the Board

During 2012, the prevalence of providing additional compensation for Lead/Presiding Directors and non-Executive Board Chairs increased to nearly 80 percent, up from approximately 70 percent in 2011 and 65 percent in 2010. In terms of additional compensation for the role, median pay was unchanged at $25,000 in from 2010 to 2012 for Lead/Presiding Directors, and increased slightly for non-Executive Chairs.

CAP Perspective: While not all non-executive Board leaders receive additional pay for the role, prevalence of additional compensation for these roles is expected to continue to increase over time. The differential in pay between Lead/Presiding directors and non-Executive Chairs is in line with the typical responsibilities of each position.

Conclusion

With the increased scrutiny Boards are under and the time commitment required, in the last five years we have seen a relatively significant increase in non-employee director compensation, though at this point we have hit more of a “steady state” and expect more modest pay level changes going forward. In terms of practices, pay programs have continued a trend towards simplification, as director compensation has become viewed more as an “advisory fee” than an “attendance fee.”

It continues to be important to comprehensively evaluate director pay programs on a regular basis or risk falling behind the curve in terms of desired market positioning and best in class program design. When programs are evaluated, the process and practices listed below should be considered.

|

Best in Class Director Compensation PROCESS |

|

|

Best in Class Director Compensation PRACTICES |

|

1 Analysis includes public Fortune 100 companies (excludes privately held companies).

2 Research assistance for this report was provided by Alex Stahl, Kevin Scott, Armando Rivera and Ryan Colucci.

3 Total Board Compensation reflects all cash and equity compensation for Board and committee service, excluding compensation for additional leadership roles such as committee Chairman, Lead/Presiding director, or non-executive Chairman of the Board.

4 Audit, Compensation and Nominating / Governance committees.

5 Reflects all compensation for committee member service (excludes additional fees for leadership roles), across all Board committees.

The SEC’s proposed rule requires companies to disclose in their registration statements, proxy statements and other annual reports where compensation is mentioned, the following three items: 1.) The annual total compensation of its median employee, 2.) The annual total compensation of the CEO, and 3.) The ratio of the two amounts above. While this calculation seems like straightforward arithmetic, it may prove to be difficult for many companies, especially those whose operations are complex and global.

- Employees Included. As a first step in the process of identifying the median employee, companies must incorporate all employees including full-time, part-time, temporary, non-US employees, and employees of a subsidiary, all of which have been employed on the last day of the fiscal year.

- Identifying the Median Employee: The proposed rule does not specify methodologies for identifying the median employee, aside from the requirement that all employees be considered. Instead, the proposed rule allows companies to choose a methodology for identifying the median employee in a way that is logical and appropriate for the company’s size and structure. Companies can, depending on their complexity, use the median employee of the full-employee population, or rely on statistical sampling to estimate what the median employee earns.

- Determining Compensation of the Median Employee. One of the greatest challenges in calculating the CEO pay ratio was identifying pay for employees in a consistent manner in order to calculate median pay. The proposed rule has provided wide latitude to companies in using alternative definitions of pay for purposes of estimating the median paid employee (e.g., total direct compensation, total cash compensation, W-2 compensation). However, the SEC is more stringent about annualizing pay. While companies may annualize compensation for workers hired mid-year, they would not be permitted to make full-time equivalent adjustments for part-time workers.

- Calculating the Ratio. Once the median employee is identified, compensation for that employee has to be determined. The Dodd-Frank Act requires that employee total compensation would be calculated using the same methodology as required for named executive officers, a requirement that is not currently applied to non-executive employees. A key advantage of the proposed rule is that this more complicated pay calculation only needs to be done for the employee identified as “the median employee”.

CAP Comments: While some commentators hoped that the rule would apply to only U.S. employees or only full-time employees, the proposed rule includes the total employee population. This will make the determination of the median employee more complicated for global employers. In addition, it may create challenges for investors in interpreting the ratio or comparing across companies, as the ratio will vary based on the number of workers employed in low wage countries or the number of part-time or temporary workers employed.

CAP Comments: It is a positive sign that the SEC recognizes the complexity of determining the median employee. Unfortunately, compensation professionals will have to dedicate time and resources to understanding the potential approaches available to them and will likely have to pay external experts to conduct the analysis, particularly if they rely on statistical sampling.

CAP Comments: The latitude provided should simplify calculating pay in a way that facilitates identifying the median employee. The downside of the proposal is that differences in approach may make comparisons of the ratio across companies less meaningful. The limitations on annualizing compensation will result in less favorable CEO pay ratios for companies employing temporary or part-time workers.

CAP Comments: This calculation should be relatively straightforward as the greatest complexity is in identifying the median employee.

Additional aspects to this regulation would require companies to disclose methodologies, estimates and assumptions used in the calculation. As provided by the JOBS Act, the proposed rule would not apply to emerging growth companies, nor would it apply to smaller reporting companies or foreign private issuers.

Implementation Time-frame

Following this proposal, there will be a 60 day public comment period. Companies would be required to report the pay ratio with respect to compensation for its first fiscal year beginning after the effective date. Depending on the effective date of the final rule (2013 vs. 2014), fiscal year companies will first have to report the ratio in their 2015 or 2016 proxy statement, covering pay for the 2014 or 2015 fiscal year.

Overall Comments

The intent of this legislation is to raise awareness around the disparity between pay levels for top executives and the typical worker. However, from our perspective the primary outcome of the rule is an additional burden on companies to comply with this law. Companies will need to spend time and resources collecting and compiling compensation records and will likely require the assistance of technical and legal advisors to establish and implement the approach to identify the median employee. In the cost-benefit analysis section of the proposal, the SEC struggled to identify any quantifiable benefits of the rule, while the costs of compliance are fairly obvious.

The CEO pay ratio will be challenging to interpret. The ratio may vary across companies due to corporate structure and business decisions, rather than the pay philosophy of the company. For example, companies in industries that depend on part-time and seasonal workers will have a pay ratio that looks less egalitarian than a company with only a full-time workforce, regardless of whether each company pays a competitive and market-based wage to each class of employees. Moreover, for companies with concentrations of employees in one or more developing countries, this ratio will exaggerate the difference between executive and employee pay, not to mention the additional administrative responsibilities necessary to convert workers’ wages abroad to US dollars. In contrast, a company that has outsourced all of its low paid administrative functions to India or China, may have a better CEO pay ratio than a company that completes these tasks in-house. While we expect that most investors will ignore the CEO pay ratio, there will likely be reporting of the ratio in the press. Companies should also monitor whether ISS and Glass-Lewis take interest in the pay ratio. While our sense is that the CEO pay ratio is not a primary concern of institutional investors, the shareholder advisory firms are active in finding new areas of executive pay to target for criticism.

Conclusion

Starting now, the SEC will review comments received within the 60 day window, and comments are already being submitted. While it is unknown how such comments will be received and/or incorporated by the SEC, it is important to be thinking ahead to future disclosure and the necessary changes corporate human resources professionals will need to make to comply with the new rule.

Many groups as well as factions within congress lobbied to have this provision of Dodd-Frank removed as the resources required to implement it are anticipated to outweigh the benefits of the additional disclosure. While there has been limited information released from the SEC, it is likely that the guidance will be somewhat less onerous than originally expected, possibly only requiring companies to compare CEO compensation to a sample of employees as opposed to the entire population. More questions than answers still remain, including when the disclosure will be effective. However, as soon as preliminary guidance is released, we will send a comprehensive CAPFlash on the guidance.

Last year, the study showed an increase in compensation for both CEOs and CFOs, but at much lower levels than the prior year. This leveling off of pay was partially driven by a stabilizing economy and increased confidence in goal setting, leading to less volatility in corporate performance results in incentive plans. To determine if this trend is continuing, we conducted a similar study in 2013 using a sample set of 62 US public companies. The study analyzes executive pay data disclosed by companies with revenues ranging from $1 to $145 billion, with median revenues of $9 billion. Only companies with the same CEO and CFO incumbents from 2010 to 2012 were included in order to focus on year-over-year changes for an individual incumbent. Similar to our methodology in prior years, financial services firms were excluded from the study, as this industry’s compensation practices continue to evolve in the years post the financial crisis.

Our findings, summarized below, indicate that overall, increases in total compensation levels for both CEOs and CFOs slowed in 2011-2012 compared to double-digit pay increases in the 2009-2010 period and mid-single-digit increases in the 2010-2011 period. This dramatic slowdown suggests that the halting economic recovery is having an impact. Percentage pay increases in all three years were higher for CFOs compared to CEOs, driven by slightly higher increases in long-term compensation and smaller decreases in annual bonus. The slower rate of growth in CEO compensation may be driven by the continued focus on CEO pay by shareholders and proxy advisory firms and the increased demand for pay and performance alignment. On an absolute basis, CFO pay continues to be approximately one-third of CEO pay.

Study Results

Salaries

In 2012, approximately 85% of CFOs received salary increases. The median increase was 3.0% and the 75th percentile increase was 4.9%. In comparison, only 53% of CEOs received salary increases and the increases were smaller — 0.5% at median and 3.1% at the 75th percentile. The prevalence of salary increases for CFOs remained similar to last year with about 85% of incumbents receiving a salary increase. Among CEOs, approximately 55% received a salary increase, similar to 2010.

|

Salary Increase Prevalence |

||||||

|

|

2009 – 2010 |

2010 – 2011 |

2011 – 2012 |

|||

|

|

No Increase |

Increase |

No Increase |

Increase |

No Increase |

Increase |

|

CEO |

43.8% |

56.3% |

34.4% |

65.6% |

46.8% |

53.2% |

|

CFO |

25.0% |

75.0% |

12.5% |

87.5% |

14.5% |

85.5% |

Actual Pay Levels

Overall, actual total direct compensation (salary plus actual annual incentive plus the grant date value of long-term incentives) for CEOs and CFOs leveled off in 2011-2012. These lower, single-digit changes in pay levels are consistent with the increased focus on pay for performance we have seen over the last few years. They also likely reflect the slow pace of economic recovery. At the median, salary increases were higher for CFOs than CEOs in 2011-2012. Bonus levels decreased for both CEOs and CFOs and long-term incentives increased modestly (2%) for CFOs and remained flat (0%) for CEOs.

|

Median Percentage Change in Pay Components |

||||||

|

|

2009 – 2010 |

2010 – 2011 |

2011 – 2012 |

|||

|

Pay Components |

CEO |

CFO |

CEO |

CFO |

CEO |

CFO |

|

Salary |

1.0% |

3.7% |

1.8% |

3.5% |

0.5% |

3.0% |

|

Actual Bonus |

19.0% |

22.7% |

0.0% |

3.5% |

-2.8% |

-1.2% |

|

Long-Term Incentives |

10.1% |

14.8% |

10.0% |

10.3% |

0.0% |

2.0% |

|

Actual Total Direct Comp. |

14.4% |

20.0% |

3.6% |

7.5% |

-0.3% |

1.4% |

|

Financial Performance (Median Levels) |

|||

|

Year |

Total Shareholder Return (as of 12/31) |

1-Year Revenue Growth |

1-Year Net Income Growth |

|

2010 |

24% |

10% |

19% |

|

2011 |

5% |

9% |

13% |

|

2012 |

14% |

3% |

2% |

While movement in pay among CFOs and CEOs was directionally aligned, absolute CFO total direct compensation levels, on average, have been approximately 30% of CEO total direct compensation levels over the last three years.

Target Pay Mix

In terms of target compensation levels, the overall pay mix remained largely unchanged from 2010 to 2012, with a greater emphasis on at-risk pay for CEOs than for CFOs.

Long-Term Incentive (LTI) Vehicle Prevalence and Mix

The use of at least two long-term incentive vehicles continues to be the majority practice when awarding LTI to CEOs and CFOs. The role of stock options has remained steady in the overall mix with companies delivering about 30% of LTI using this vehicle. On average, performance-based LTI continues to comprise approximately 50% of LTI for CEOs and CFOs. Data shows that 80% of CFOs and 85% of CEOs received some form of performance-based awards as part of their LTI program in 2012.

|

Number of LTI Vehicles Used in 2012 |

||

|

|

% in Total |

|

|

CEO |

CFO |

|

|

1 |

24% |

17% |

|

2 |

47% |

53% |

|

3 |

27% |

28% |

|

Average |

2 |

2 |

|

LTI Mix |

||||||

|

2010 |

2011 |

2012 |

||||

|

Vehicle |

CEO |

CFO |

CEO |

CFO |

CEO |

CFO |

|

Stock Options |

33% |

30% |

32% |

32% |

30% |

32% |

|

Time Vested Restricted Stock |

20% |

23% |

17% |

22% |

16% |

20% |

|

Perf. Based LTI |

48% |

47% |

51% |

46% |

53% |

48% |

Conclusion

As companies and Boards focus on the alignment between pay and performance, and the economic recovery continues at a slow pace, it is not surprising that pay increases have slowed over the last 3 years. The rates of increases continue to be for higher CFOs compared to CEOs; however, the increases for both have slowed dramatically in 2011-2012. We expect future changes in compensation for these positions to continue to be closely linked to overall company performance, as well stock price performance, since the majority of pay for CEOs and CFOs is delivered through long-term incentives.