HIGHLIGHTS

- Companies rarely make wholesale changes to plans, but frequently revisit the performance metrics used

- Most companies use multiple measures to ensure the plan provides balance and aligns with overall business strategy

- Overall, 2013 annual incentive payouts were higher than in 2012 indicating stronger performance

Survey Sample

Compensation Advisory Partners (“CAP”) reviewed 2014 proxy disclosures at a sample of 100 companies among the Fortune 500 representing nine industry groups. Industry groups included: Automotive, Consumer Goods, Financial Services, Health Care, Insurance, Manufacturing, Pharmaceutical, Retail, and Technology. For the companies studied, the median revenue size and market capitalization was $32B and $52B, respectively. The median 2013 total shareholder return (TSR // change in stock price plus dividends) was 43%.

CHANGES IN ANNUAL INCENTIVE PLAN DESIGN

Overall, 34% of companies in CAP’s study changed their annual incentive plan design in 2013 or 2014. The most common changes were to the performance metrics used to fund awards (47% of the companies making a change) or to the weightings applicable to performance metrics (32%). Another frequent change was to increase the target award opportunities offered to Named Executive Officers; reductions in target awards were made much less frequently. These changes, as well as other modifications shown in the chart on the right, illustrate that companies continue to review and enhance the pay-for-performance relationship through changes to the annual incentive program.

|

Type of Change Reported in CD&A |

2013 No. of Cos. |

% of Cos. Reporting Changes |

||

|

2013 (n = 34) |

2012 (n = 37) |

2011 (n = 43) |

||

|

Change in performance metrics used to fund awards |

16 |

47% |

43% |

28% |

|

Change in performance metric weighting/mix |

11 |

32% |

35% |

42% |

|

Increased/Reduced target award opportunities (CEO and/or CFO) |

11 |

32% |

11% |

21% |

|

Other changes |

4 |

12% |

22% |

19% |

|

Change in maximum award payout |

3 |

9% |

8% |

12% |

Note: Due to multiple changes, does not add up to 100%.

Change in Performance Metrics

Among the companies that changed the annual incentive performance metrics, about one-half of companies modified plan metrics while maintaining the current number of metrics to better align pay with performance:

- Ten (10) companies kept the same number of metrics but replaced a metric in the incentive plan

- Four (4) companies reduced the number of metrics, and

- Two (2) companies added metrics to the current plan.

Several companies indicated that their rationale for changing annual incentive metrics was, in large part, to have a more holistic view of overall company performance and to better align incentives with their business strategy:

- AFLAC Inc: Added Operating Return On Equity (OROE) as a performance metric for senior vice presidents and above; this metric allows shareholders to evaluate AFLAC’s financial achievements relative to other organizations in terms of how effectively capital is used to generate earnings

- Danaher Corp: Added Return On Investment Capital (ROIC) in order to help validate the efficiency of earnings and complement the cash flow metric

- United Technologies Corp: Changed the earnings metric from EPS to Net Income since Net Income is not impacted by share repurchases

- Bristol-Myers Squibb: Replaced Adjusted Net Cash Flow from Operations with a metric for pipeline performance that consists of regulatory submissions and approvals and is a better indication of long-term growth potential.

Change in Target Bonus Opportunity

In 2013, median target bonus opportunities for CEOs increased (by 9 percentage points), while the opportunities for CFOs decreased (by 3 percentage points). Most notably, target bonus opportunity for CEOs in the Automotive, Insurance, and Retail industries increased by 10 percentage points year over year. However, the Technology industry experienced a significant decrease (21 percentage points) due to an increase in the base salary for Cisco’s CEO (from $375,000 to $1,100,000) and a decrease in the target opportunity for the new CEO at Intel (from 462.7% of base salary to 239.2%).

Median target bonus opportunity for CFOs in the Automotive industry experienced a decrease of 5 percentage points in 2013 largely due to the promotion of a new CFO at Goodyear (target opportunity decreased from 91% to 63% of base salary). Conversely, target bonus opportunity for CFOs in the Insurance industry increased (8 percentage points) in 2013; all other industries saw little movement to the target bonus opportunity.

|

Industry |

Median Target Bonus as a % of Salary |

|||||

|

CEO |

CFO |

|||||

|

2013 |

2012 |

2011 |

2013 |

2012 |

2011 |

|

|

Automotive |

135% |

125% |

130% |

85% |

90% |

88% |

|

Consumer Goods |

160% |

160% |

170% |

93% |

95% |

100% |

|

Financial Services |

n/m |

n/m |

n/m |

n/m |

n/m |

n/m |

|

Health Care |

150% |

145% |

145% |

100% |

101% |

100% |

|

Insurance |

210% |

200% |

200% |

133% |

125% |

120% |

|

Manufacturing |

157% |

154% |

156% |

100% |

97% |

95% |

|

Pharmaceutical |

150% |

150% |

150% |

98% |

97% |

91% |

|

Retail |

180% |

170% |

168% |

85% |

83% |

85% |

|

Technology |

210% |

231% |

200% |

130% |

131% |

121% |

|

Total Sample |

166% |

157% |

153% |

100% |

103% |

100% |

Note: Financial Services industry is excluded since most companies in our study do not disclose target bonus opportunities for the Named Executive Officers.

ANNUAL INCENTIVE PLAN DESIGN / PRACTICES

Award Leverage

Disclosure of the payout range (i.e., both threshold and maximum payout as a percentage of target) is a limited practice as most companies reviewed did not disclose a threshold level of performance required to receive a bonus payment. For the 37 companies that disclose a threshold bonus, 50% of target is the most common payout percentage. However, 20 companies disclose a minimum bonus payout of less than 50% of target; a majority of these companies provide a payout based on multiple plan metrics.

Approximately 75% of companies disclose the maximum bonus opportunity. A majority (60%) have a maximum bonus opportunity of 200% of target bonus. Ten (10) companies have a maximum bonus of 250% of target or higher. A majority of these companies are in the Consumer Goods, Pharmaceutical, and Technology industries.

|

Threshold as a % of Target (n=37) |

Maximum as a % of Target (n = 73) |

|||||

|

Range |

# of Cos. |

% of Cos. |

Range |

# of Cos. |

% of Cos. |

|

|

< 25% |

10 |

27% |

> 125% < 150% |

2 |

3% |

|

|

> 25% < 50% |

10 |

27% |

> 150% < 200% |

14 |

19% |

|

|

50% |

13 |

35% |

200% |

44 |

60% |

|

|

> 75% < 100% |

4 |

11% |

> 200% < 250% |

3 |

4% |

|

|

> 250% |

10 |

14% |

||||

Annual Incentive Plan Metrics

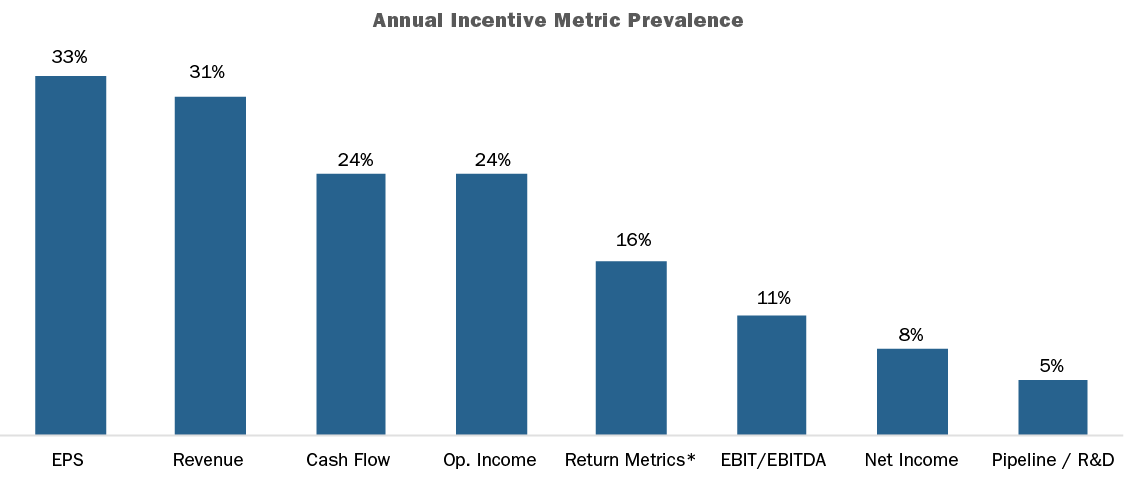

EPS, Revenue, Cash Flow and Operating Income are the most prevalent metrics used in annual incentive plans. Although EPS is the most common metric overall, it is the most common metric for only two industries (Financial Services and Healthcare). Revenue, the second most common metric, is the most prevalent in four industries (Consumer Goods, Pharmaceutical, Retail and Technology). Our findings suggest that EPS is used more broadly across industries while Revenue tends to be used in consumer-driven industries.

Most companies (approximately 70%) use more than one performance metric in the annual incentive plan. 25% of companies disclose using two (2) metrics in their annual incentive programs, 25% use three (3) metrics, and 21% of companies use four (4) or more metrics. Approximately 62% of these companies use a profit-based metric in combination with Revenue and/or Cash Flow.

The chart below shows the three (3) most metrics by industry in 2013:

|

Industry |

Metric #1 |

Metric #2 |

Metric #3 |

|

Automotive |

Cash Flow (45%) |

EBIT (45%) |

ROA (27%) |

|

Consumer Goods |

Revenue (67%) |

EPS (58%) |

Cash Flow (33%) |

|

Financial Services |

EPS (33%) |

ROE (17%) |

Op. Income (8%) |

|

Health Care |

EPS (40%) |

Op. Income (30%) |

EBIT (30%) |

|

Insurance |

Op. Income (46%) |

Op. ROE (23%) |

Op. EPS (15%) |

|

Manufacturing |

Cash Flow (30%) |

EPS (30%) |

Revenue (20%) |

|

Pharmaceutical |

Revenue (70%) |

EPS (70%) |

Pipeline/R&D (50%) |

|

Retail |

Revenue (40%) |

Op. Income (40%) |

EBIT (30%) |

|

Technology |

Revenue (58%) |

Cash Flow (50%) |

Op. Income (33%) |

Note: Percentages reflect the prevalence of companies disclosing the metric.

*Return metrics include: ROE, Op. ROE, ROA, and ROI/ROIC

2013 Actual Bonus Payout

Nearly all companies (98%) in our research awarded bonuses to their Named Executive Officers for 2013 performance. Overall, the median CEO bonus was 121% of target compared to 112% in 2012, indicating that 2013 performance was generally stronger than 2012. Most industries exceeded target bonus payouts by 11 – 65 percentage points. However, two industries (Retail and Technology) fell short of expectations by 22 and 12 percentage points, respectively.

Use of deferral mechanisms in the annual incentive plan is a limited practice and is more common in the Financial Services industry given regulations from the Federal Reserve. However, a few companies across industries also have a deferral policy in place. Companies typically defer annual incentive payment in the form of restricted stock/units.

|

Industry |

Actual Bonus as a % of Target Bonus – CEO |

||||||||

|

75th Percentile |

Median |

25th Percentile |

|||||||

|

2013 |

2012 |

2011 |

2013 |

2012 |

2011 |

2013 |

2012 |

2011 |

|

|

Automotive |

183% |

131% |

186% |

165% |

102% |

153% |

127% |

69% |

130% |

|

Consumer Goods |

133% |

137% |

149% |

112% |

103% |

132% |

70% |

94% |

78% |

|

Financial Services |

142% |

120% |

130% |

126% |

80% |

114% |

101% |

44% |

111% |

|

Health Care |

149% |

157% |

159% |

127% |

127% |

127% |

116% |

103% |

116% |

|

Insurance |

170% |

144% |

130% |

150% |

130% |

106% |

123% |

112% |

85% |

|

Manufacturing |

119% |

146% |

162% |

111% |

107% |

136% |

98% |

100% |

119% |

|

Pharmaceutical |

158% |

156% |

161% |

138% |

142% |

144% |

122% |

125% |

130% |

|

Retail |

119% |

136% |

147% |

78% |

117% |

129% |

68% |

79% |

112% |

|

Technology |

121% |

124% |

149% |

88% |

99% |

100% |

69% |

90% |

75% |

|

Total Sample |

151% |

144% |

156% |

121% |

112% |

133% |

96% |

93% |

105% |

Note: Most companies in the Financial Services industry does not disclose target bonus. Figures for the Financial Services industry reflects bonus as a percentage of 3-year average actual bonus.

Use of Discretion

Approximately 50% of companies in our research disclose the use of discretion in the annual incentive plan. Among these companies, approximately 40% allow only for downward adjustments of the final payout. Approximately 55% allow for both upward and downward adjustments by funding bonuses for Name Executive Officers at maximum based on a financial metric (this is unrelated to the final award allocation which may have additional performance requirements) to ensure compliance with Section162(m) of the Internal Revenue Code. This approach provides the Committee with the most flexibility in determining the bonus payout.

Conclusion

Given significant changes to the annual incentive plan design in recent years, companies rarely made wholesale changes to the overall plan design in 2013 or for 2014. Among the companies that made changes, most were focusing on refining the incentive metrics to ensure a more complete view of company performance and alignment with the overall business strategy. Despite these changes to the incentive metrics, EPS, Revenue, Cash Flow and Operating Income continue to be most common. While we would not expect to see extensive changes to the incentive plan design in the future, we anticipate that companies will continue to refine their metrics and the metric weightings as they continue to ensure executive pay is aligned with performance.

Highlights

- Companies continue to refine their existing stock ownership guidelines and stock retention requirements to demonstrate good governance and support shareholder alignment

- 98% of companies have one or both of these types of guidelines

- Median CEO stock ownership guideline has increased to 6x base salary from 5x since 2010

- Stock retention requirements have increased in prevalence since 2010, with 49% of companies using stand-alone stock retention requirements and/or stock retention requirements associated with a stock ownership guideline

Survey Sample

Compensation Advisory Partners (“CAP”) reviewed 2014 proxy disclosures at a sample of 100 companies among the Fortune 500, representing nine industry groups. Industry groups included: Automotive, Consumer Goods, Financial Services, Health Care, Insurance, Manufacturing, Pharmaceutical, Retail, and Technology. For the companies studied, the median revenue size and market capitalization was $32B and $52B, respectively. The median 2013 total shareholder return (TSR // change in stock price plus dividends) was 43%.

PREVALENCE OF STOCK OWNERSHIP GUIDELINES AND STOCK RETENTION REQUIREMENTS

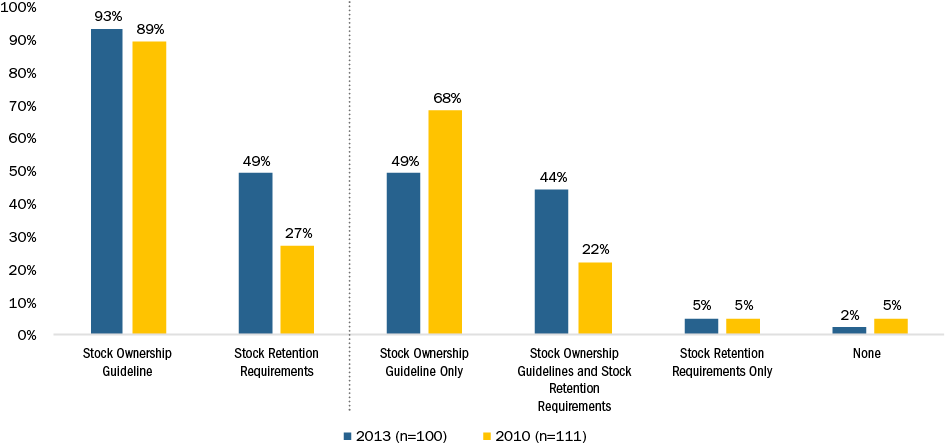

The prevalence of stock ownership guidelines among companies reviewed is approximately 93%, showing a slight uptick since 2010, when approximately 89% of companies had stock ownership guidelines in place. Between 2010 and 2013, companies with both stock ownership guidelines and stock retention requirements increased to 44% from 22%, while the prevalence of having only stock retention requirements remained flat at 5%. The number of companies with no form of stock ownership guidelines or stock retention requirements decreased to 2% from 5%. Companies are demonstrating increased efforts toward good corporate governance by ensuring executives hold a meaningful amount of equity.

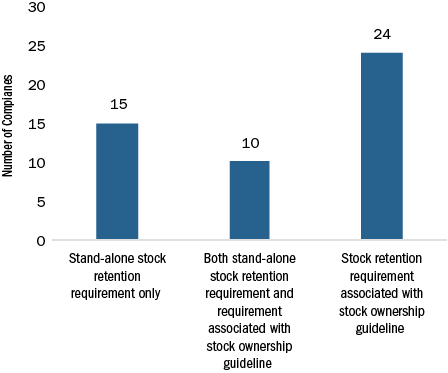

The most common stock retention requirement is to require executives to hold shares until a stock ownership guideline is achieved (34 companies). Implementation of stand-alone stock retention requirements that apply even after a stock ownership guideline has been achieved (25 companies) is a growing trend that we have seen over the last 3 years.

Prevalence of Different Forms of Stock Retention Requirements (n=49)

EXAMPLES OF STOCK RETENTION REQUIREMENTS

Stand-alone stock retention requirement only: AT&T

“Executive officers are required to hold 25% of the AT&T shares they receive (after taxes and exercise costs) from an incentive, equity, or option award granted to them after January 1, 2012, until one year after they leave the Company.”

Both stand-alone stock retention requirement and requirement associated with stock ownership guideline: Lincoln Financial Inc.

“If at any point the ownership guideline is not met with shares otherwise owned by the executive, the executive would be required to retain 50% of the net profit shares resulting from previously granted equity-based long-term incentive plan awards that are exercised or vest as applicable. Additionally, once an executive has met the minimum share ownership levels, they are also required to retain an amount equal to 25% of the net profit shares resulting from equity-based long-term incentive plan grants for five years from the date of exercise for stock options or the date of vesting for other awards.”

Stock retention requirement associated with stock ownership guideline: Gap, Inc.

“Executives not meeting the requirement must retain 50% of after-tax shares acquired through stock compensation programs until the requirement is reached.”

STOCK OWNERSHIP GUIDELINES

83% of companies express stock ownership guidelines as a multiple of salary and 13% express guidelines as a fixed number of shares. Fixed share guidelines tend to be more prevalent in the Financial Services (50%), Technology (33%), and Retail (33%) industries. Companies that use a fixed share approach generally have a volatile stock price, so locking in on a number of shares helps mitigate the potential challenges of meeting the stock ownership requirement.

|

CEO Stock Ownership Requirement Prevalence |

2013 (n = 93) |

2010 (n = 99) |

||

|

# of Cos |

% of Cos |

# of Cos |

% of Cos |

|

|

Multiple of Salary |

77 |

83% |

80 |

81% |

|

Fixed Shares |

12 |

13% |

15 |

15% |

|

Lesser Of Approach |

1 |

1% |

2 |

2% |

|

Other* |

3 |

3% |

2 |

2% |

*Other includes: Fixed Value, Multiple of Target Cash and Multiple of Notional Base

Stock ownership guidelines for CEOs have increased since 2010, with the median requirement increasing from 5x to 6x multiple of salary in 2013. The median fixed share guideline also increased to 250,000 shares compared with 150,000 shares in 2010. This suggests that companies may be increasing their fixed share guidelines to align with companies that have adopted higher multiples of salary. In 2013, the median stock ownership requirement value for the CEO is $7.7M compared with $6.7M in 2010, a significant increase of approximately 15%.

|

CEO Stock Ownership Requirement |

2013 (n = 100) |

2010 (n=99) |

||||

|

25th %ile |

50th %ile |

75th %ile |

25th %ile |

50th %ile |

75th %ile |

|

|

Multiple of Salary |

5x |

6x |

7x |

5x |

5x |

6x |

|

Fixed Shares |

125,000 |

250,000 |

500,000 |

100,000 |

150,000 |

300,000 |

|

Total Value |

$6.3M |

$7.7M |

$9.7M |

$5.4M |

$6.7M |

$8.6M |

Most companies require executives to achieve an ownership guideline requirement within 5 years. Thirteen companies (14%) disclosed a penalty for not achieving the required ownership level. The most common penalties for non-compliance include restrictions on selling shares (75% of companies), followed by reductions in future total compensation (25% of companies).

When determining which shares count towards ownership requirements, companies must consider whether to include unvested full-value shares, unexercised options or unearned performance shares. Of the companies reviewed, 69 out of 93 disclose the type of shares that count toward the guideline. Approximately 40% of companies count unvested restricted stock toward the requirement, (up from 33% in 2010) and less than 10% count unvested options or vested but unexercised options.

|

Shares Counting Toward Guideline Requirement |

2013 (n = 93) |

2010 (n = 99) |

||

|

# of Cos |

% of Cos |

# of Cos |

% of Cos |

|

|

Shares directly owned |

65 |

70% |

55 |

56% |

|

Shares in 401(k) plan |

37 |

40% |

33 |

33% |

|

Unvested restricted stock |

36 |

39% |

33 |

33% |

|

Shares indirectly owned |

32 |

34% |

29 |

29% |

|

Deferred compensation |

26 |

28% |

25 |

25% |

|

Vested but unexercised options |

7 |

8% |

6 |

6% |

|

Unvested options |

1 |

1% |

1 |

1% |

|

Not disclosed |

24 |

26% |

29 |

29% |

Note: Percentages add up to greater than 100% due to multiple types of equity counted by various companies.

Companies generally do not count unearned performance shares toward stock ownership guidelines. It is more common to included unvested restricted stock, as the eventual vesting of these shares is much more certain, since achievement of performance hurdles is not guaranteed.

STAND-ALONE STOCK RETENTION REQUIREMENTS

Companies with stock retention requirements most often require executives to hold net shares from option exercises, restricted stock share/unit vesting or performance share payouts. Requiring executives to hold net shares for one year post exercise or vest (64%) has remained the most prevalent holding period, increasing from 46% prevalence in 2010. Other companies require executives to hold shares for a 1 year period post-retirement (20%), while fewer companies require shares to be held until retirement (8%).

|

Period Subject |

2013 (n = 25) |

2010 (n = 24) |

||

|

# of Cos |

% of Cos |

# of Cos |

% of Cos |

|

|

1 year post exercise/vest |

16 |

64% |

11 |

46% |

|

2 years post exercise/vest |

0 |

0% |

1 |

4% |

|

Retirement |

2 |

8% |

8 |

33% |

|

Post-retirement |

5 |

20% |

1 |

4% |

|

Other |

2 |

8% |

4 |

17% |

|

Not disclosed |

0 |

0% |

1 |

4% |

Note: Holding requirement only for companies with stand-alone holding requirement. Percentages may add up to greater than 100% due to different holding periods for the CEO vs. other NEOs.

STOCK RETENTION SHAREHOLDER PROPOSALS

While companies may maintain stock ownership guidelines and/or stock retention requirements, they are not shielded from receiving shareholder proposals that require executives to hold a meaningful percentage of equity until requirement. Among the Russell 3000, 30 companies in 2014 and 46 companies in 2013 received shareholder stock retention proposals. In all cases, the proposals failed or were withdrawn. The median level of shareholder support for these proposals was less than 25%.

Disclosed Changes to Stock Ownership Guidelines and Stock Retention Requirements

22% of companies disclosed making a recent change to their stock ownership guidelines. Of those companies that modified their guidelines, the two most common changes were adopting a stock holding requirement (32%) and increasing the ownership guideline (27%).

|

Changes To Stock Ownership Guidelines and Stock Retention Requirements |

2013 (n = 22) |

2010 (n = 25) |

||

|

# of Cos |

% of Cos |

# of Cos |

% of Cos |

|

|

Added holding requirement |

7 |

32% |

6 |

24% |

|

Increased guideline requirement |

6 |

27% |

12 |

48% |

|

Newly adopted stock ownership guideline |

5 |

22% |

1 |

4% |

|

Changed fixed value / multiple approach |

2 |

9% |

n/a |

n/a |

|

Adopted mandatory holding of shares through retirement |

1 |

5% |

1 |

4% |

|

Extended participation |

1 |

5% |

n/a |

n/a |

|

Modified penalty for non-compliance |

n/a |

n/a |

5 |

20% |

SUMMARY

In 2014, companies continued to practice good governance by enhancing their stock ownership guidelines. Additionally, companies continue to implement stock retention requirements, albeit at a slower rate. Stock retention requirements most often serve as a supplement to existing stock ownership guidelines. Overall, we expect companies to continue to strengthen their stock ownership and stock retention requirements because these policies address issues important to both shareholders and proxy advisory groups, and align executives with shareholders.

Highlights

- Nearly all companies (94%) have adopted a clawback policy, even without SEC guidance on Dodd Frank requirements for clawbacks

- Consistent with our past findings, the most common forms of compensation that are potentially subject to recoupment are prior year’s cash and stock incentives

- Hedging policies are in place at most companies, with 95% disclosing a hedging policy (vs. 91% in 2013)

- Pledging policies can vary in scope as companies, but 63% of companies have a policy of some type in place

- Some companies ban all pledging (68%), while others require advance approval for pledged shares (20%) or only prohibit pledging of shares subject to stock ownership guidelines (12%)

Survey Sample

Compensation Advisory Partners (“CAP”) reviewed 2014 proxy disclosures at a sample of 100 companies among the Fortune 500 representing nine industry groups. Industry groups included: Automotive, Consumer Goods, Financial Services, Health Care, Insurance, Manufacturing, Pharmaceutical, Retail, and Technology. For the companies studied, the median revenue size and market capitalization was $32B and $52B, respectively. The median 2013 total shareholder return (TSR // change in stock price plus dividends) was 43%.

Clawbacks

Although companies are still waiting for SEC guidance on Dodd Frank, many have already implemented clawback policies on their own. Dodd Frank requires a broader definition of clawback compared to Section 304 of SOX, which applies to CEOs and CFOs.

Similar to our findings last year, 94% of companies we studied have some form of clawback policy, compared to 86% and 80% in 2011 and 2010, respectively. Because the majority of companies have now adopted robust clawback policies, the number of changes made in 2013 as compared to prior years has decreased. In 2013, there were no companies that adopted a new clawback policy, while only 7 modified existing provisions. The most common changes made were to expand the compensation subject to clawbacks and expand the triggers for clawbacks beyond financial restatements.

As in prior years, a financial restatement (87%) and misconduct (77%) are the most common triggers for a clawback. For the first time in our study, fraud (50%) will trigger a clawback for a majority of the companies analyzed.

Under nearly all policies, it is most common for companies to include the ability to recoup compensation previously granted. Some companies will also have clawback provisions in place that allow them to either adjust the amounts of future incentive compensation given or cancel any outstanding performance-based stock or cash awards.

|

Compensation Subject to Clawback |

2013 |

% of Cos. |

2012 |

% of Cos. |

2011 |

% of Cos. |

2010 |

% of Cos. |

|

Prior LTI |

91 |

98% |

88 |

95% |

95 |

97% |

79 |

89% |

|

Prior Annual Incentive |

89 |

96% |

86 |

92% |

92 |

94% |

81 |

91% |

|

Future Annual Incentive |

20 |

22% |

19 |

20% |

16 |

16% |

20 |

22% |

|

Future LTI |

21 |

23% |

18 |

19% |

15 |

15% |

14 |

16% |

Note: Percentages add up to greater than 100% due to multiple responses

Coverage extends to all NEOs in 97% of companies, which is higher than our findings in 2010, 2011, and 2012. Interestingly, many companies extend coverage beyond the NEO level, with 50% of companies having clawback policies in place for all Section 16 officers. Companies are not required to disclose the level of program detail in the proxy, but we expect most program provisions are more broad-based.

Similar to our findings in prior years, less than a quarter of companies indicate the length of the look-back period during which compensation can be recovered. Of the 21 companies that disclosed a time frame, the most common is 1 year (52% of companies) from date of restatement, followed by 3 years (38% of companies).

As we wait for the SEC to propose final rules, there are several practical challenges to clawing back compensation, such as how to clawback equity gains, how to claw back from former employees and the tax implications of clawbacks.

Hedging and Pledging

With increasing scrutiny from shareholder services such as ISS, hedging and pledging policies have become more significant governance / shareholder issues. ISS has taken the stance that any hedging and significant pledging by insiders to be indicative of a potential failure of risk oversight on behalf of a company’s Board. The Board’s policy regarding these practices is most commonly reflected in the company’s insider trading policy, but it can be addressed through Board resolutions or a stand-alone policy.

Hedging is viewed as a poor practice as it insulates executives from stock price movement and reduces alignment with shareholders. Pledging, in modest amounts, may not be viewed as negatively, yet can become problematic if there were a significant decline in stock price which necessitated a sale of shares from a senior executive. Given the potential negative perception of insider hedging and pledging, as well as the pending Dodd Frank guidance, companies have begun to adopt policies to limit these provisions. Anti-hedging and pledging policies are in place at 95% and 63% of companies studied, respectively; 63% of companies have both policies in place and 32% only have a hedging policy.

|

Hedging / Pledging Policies |

2013 |

% of Cos. n=100 |

2012 |

% of Cos. |

|

Hedging Policy |

95 |

95% |

91 |

91% |

|

Pledging Policy |

63 |

63% |

59 |

59% |

|

Both |

63 |

63% |

59 |

59% |

|

Hedging Only |

32 |

32% |

42 |

42% |

Note: Percentages add up to greater than 100% due to multiple responses

An example of typical disclosure of a prohibition on hedging/pledging is reflected in 3M’s proxy disclosure:

“The Company’s stock trading policies prohibit directors and the Company’s executive officers from (i) purchasing any financial instrument that is designed to hedge or offset any decrease in the market value of the Company’s common stock, including prepaid variable forward contracts, equity swaps, collars and exchange funds; (ii) engaging in short sales related to the Company’s common stock; (iii) placing standing orders; (iv) maintaining margin accounts; and (v) pledging 3M securities as collateral for a loan.”

Our analysis of pledging policies was broken down further to show that there are variations to prohibit pledging. A company can ban all pledging (68% of companies with anti-pledging policies), prohibit pledging of shares unless an employee receives advance approval (20%) or prohibit any shares subject to stock ownership guidelines to be pledged (12%).

An example of the latter two anti-pledging policies can be found in Best Buy and ACE’s proxy statements, respectively:

Best Buy: “…our executive officers and Board members are prohibited from holding Company securities in a margin account or pledging Company securities as collateral for a loan, unless approved in advance by the Compensation Committee.”

ACE: “The Company prohibits NEOs from pledging shares that are held in satisfaction of the share ownership guidelines.”

Pledging was not addressed in Dodd-Frank per se, and we do not know what the SEC’s position will be in the future. We do however expect more companies to adopt pledging policies going forward given ISS’ 2012 policy statement that identified pledging of company stock by executives as a poor practice.

Conclusions

We continue to see companies stay ahead of the curve and track “best practices” in order to satisfy shareholders and proxy advisory firms. This results in reevaluations of company pay and governance practices, and as our research shows, continued modification of clawback policies, and adoption of hedging and pledging policies. While formal guidelines have not been given to date, companies are adopting these policies as good governance, regardless of any final SEC guidance.

Highlights

- The look and feel of proxy statements have changed

- Best practices for CD&A include a concise executive summary

- Pay mix charts, other charts, a list of “best practices” that the issuing company follows and a proxy summary are now commonly included

- Financial performance frames the discussion of executive compensation

- A trend in recent years is the disclosure of realized/realizable pay

Compensation Discussion & Analysis (CD&A)

Survey Sample

Compensation Advisory Partners (“CAP”) reviewed 2014 proxy disclosures at a sample of 100 companies among the Fortune 500, representing nine industry groups. Industry groups included: Automotive, Consumer Goods, Financial Services, Health Care, Insurance, Manufacturing, Pharmaceutical, Retail, and Technology. For the companies studied, the median revenue size and market capitalization was $32B and $52B, respectively. The median 2013 total shareholder return (TSR // change in stock price plus dividends) was 43%.

The Say on Pay vote has succeeded in improving and increasing communication with shareholders regarding executive compensation programs. Many companies have adopted what are commonly referred to as “best practices” for proxy disclosure.

|

Elements Included in 2014 Proxy Disclosure Among Fortune 500 companies |

||

|

# of Cos |

% of Cos |

|

|

Executive Summary |

89 |

89% |

|

Pay Mix Chart(s) |

79 |

79% |

|

Use of Other Charts and/or Graphics |

73 |

73% |

|

List of “Best Practices” |

67 |

67% |

|

Realized and/or Realizable Pay |

15 |

15% |

- Executive Summary: Most important part of the CD&A. Continued enhancement over past few years. Typically includes thorough discussion of financial performance and key company achievements, a summary of CEO compensation, and key changes to executive compensation programs, if any

- Pay Mix Charts: Very common. Typically reflect variable vs. fixed pay or performance-based vs. non-performance-based pay

- Use of Other Charts and/or Graphics: Very common. Most often used to directly, and concisely, describe company performance. May include absolute and/or relative performance

- Realized Pay and Realizable Pay: Emerging practice. Intended to illustrate the impact of performance outcomes on pay over time. In contrast, while the Summary Compensation Table reflects actual cash payments, equity awards reflect target values

- List of “Best Practices”: Very common. Often takes the form of “What We Do/Don’t Do” list. Eliminates need for shareholders to take the time to seek these things out

Another trend related to enhanced proxy disclosure of executive compensation programs and decision-making, is increased disclosure of incentive plan goals. Shareholders and proxy advisory firms have expressed the desire for more information on short- and long-term incentive compensation performance targets/goals. Two examples of companies that increased proxy-based incentive plan goal disclosure in reaction to shareholder input are Coca-Cola and Dow Chemical.

|

Company |

Shareholder Feedback |

Action by Company |

|

Coca-Cola |

|

|

|

Dow-Chemical |

|

|

Conclusions

We have observed companies more frequently modifying and enhancing their executive compensation and governance practices, given increasing influence and input of shareholders (and proxy advisory firms). Shareholder communication has also been enhanced, including the proxy statement.

During the 2015 proxy season, we expect more companies to disclose realizable and/or realized pay, particularly if TSR or Say on Pay support are low, and enhance transparency and highlight best practices in executive compensation disclosure. The goal is for executive compensation programs to best support business strategy, while aligning with shareholder interests. Disclosure is an opportunity to highlight all the good work and thought that goes into the design of these programs and the related decision-making.

The SEC recently updated its regulatory agenda. As part of the update, the deadline to adopt final pay ratio rules was pushed back to October 2015 (from October 2014).

- Implication: companies with a Dec 31 fiscal year end are not expected to be required to comply with pay ratio rules/disclosure until publication of 2017 proxy statements

The deadline for other outstanding compensation-related rulemaking coming out of the Dodd-Frank Act was also delayed to October 2015: standardized pay vs. performance disclosure, hedging policies, and clawbacks requirements.

- Note: Timeline changes reflect a new deadline, not the date at which rulemaking will be published or adopted

We will provide additional updates as this issue continues to evolve.

Key CAP Findings

Board Compensation. little/no change

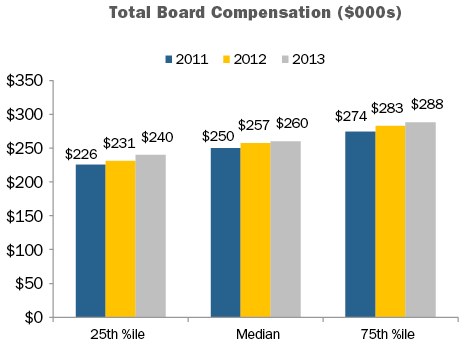

- Total Fees. At median, flat from 2012 to 2013 ($257K vs. $260K)2. Only increased four percent since 2011.

- Retainers. Pay programs have been simplified, now viewed more as an “advisory fee” than an “attendance fee.” In general, companies have moved to a fixed retainer pay structure, with a component in cash and a component in equity.

- Meeting fees. Provided by only 15 percent of companies, down slightly from 2012.

- Equity. Full-value awards (shares/units) are most common. Only five percent of companies use stock options. 92 percent of companies denominate equity awards (stock or options) as a fixed value, versus a fixed number of shares.

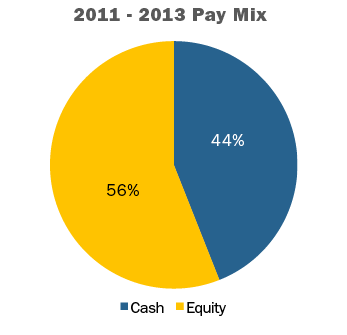

- Pay Mix. On average, 56% equity-based vs. 44% cash-based (consistent for past three years). Alignment with long-term shareholders is reinforced by delivering a majority of compensation in equity.

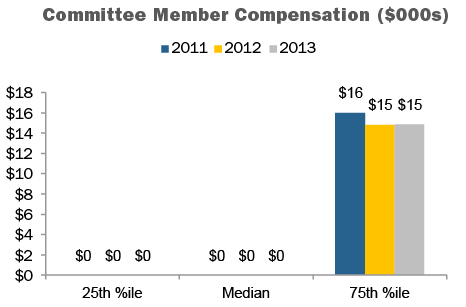

Committee Member Compensation. little/no change

- Less than half of companies paid committee-specific member fees3.

- At median, committee member compensation is $04. There has been a trend away from committee member fees; value typically rolled into Board cash or equity retainers.

Committee Chair Compensation. limited, but notable change

- Nearly all companies provided additional compensation to committee Chairs, versus committee members, typically through an additional retainer. The additional compensation recognizes additional time requirements, responsibilities, and reputational risk.

- At median, $20K in additional compensation (vs. members) was provided to Audit and Compensation Committee Chairs, and $15K to Nominating/Governance Chairs. This is the first year the premium, at median, provided to Compensation Chairs equaled that provided to Audit Chairs.

Independent Board Leader Compensation.

limited, but notable change

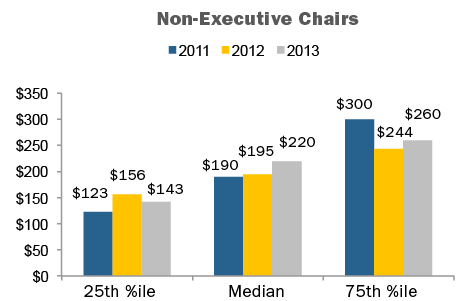

- Non-Exec Chair. Additional compensation is provided by all companies with this role, $220K at median.

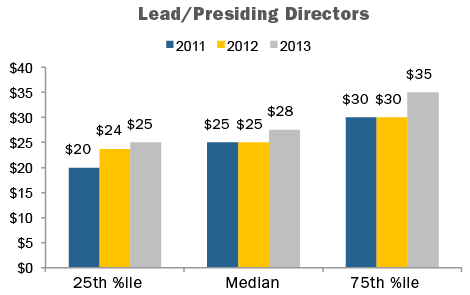

- Lead Director. Additional compensation is provided by nearly all companies with this role5, $28K at median. The differential in pay versus non-executive Chairs is in line with typical differences in responsibilities. Additional compensation was steady, at median, at $25K for the five years prior to 2013.

Perquisites. little/no change

- Overall, limited practice. One-third of companies continue to provide gift matching/charitable contribution.

Pay Limits. NEW to study

- Due mainly to advancement of litigation in Delaware court related to director compensation, several companies (23%) have adopted shareholder approved director compensation limits ($800K, at median). The limit most often applies only to equity-based compensation.

CAP Perspective

Board Pay Levels and Structure

We have hit somewhat of a “steady state” in terms of director pay levels. Over the next few years, we expect modest pay level changes; i.e., low-to-mid single-digit annual increases in Total Board Compensation6. among the broader data set. Individual companies typically make pay level changes every two-to-three years; when they do, the changes tend to be larger than those observed annually within the full data set.

In terms of practices, pay programs have continued a trend towards simplification, as director compensation has become viewed more as an “advisory fee” than an “attendance fee.” Companies have moved to fixed retainer pay structures, with a component in cash and a component in equity, as opposed to use of per-meeting fees.

Director Pay Limits

A number of companies have recently placed limits on director compensation. The limits are largely due to advancement of litigation in Delaware court. In these cases the issue has been that directors approve their own annual compensation, and the shareholder approved long-term incentive plan did not provide “meaningful limits” on the maximum award that could be granted to a director.

When seeking shareholder approval for amendment to an omnibus long-term incentive plan or director compensation plan, 23 percent of companies studied have included value- or share-based limits (13% and 10%, respectively) for non-employee director compensation. These limits range from $250K to $2 million, $800K at median, and typically apply to just equity-based compensation. Some companies have applied the limits to both cash and equity-based compensation while others have excluded initial at-election equity awards, committee Chair pay, and/or additional pay for Board leadership roles from the limit.

We expect prevalence of director pay limits to increase, becoming majority practice within the next three to four years.

Lead Director Compensation

The Lead Director role has evolved, oftentimes a more active role than three to five years ago. As a result, companies are looking at time commitment and responsibilities, and structuring compensation to appropriately reflect the current role and expectations. Boards are engaging in more outreach and meeting with shareholders to talk about governance practices, CEO succession and executive compensation, among other issues, and many investors want to hear from the Lead Director.

Prevalence of providing additional compensation for the Lead Director role has increased over the past five years. Currently, additional compensation is provided by nearly all companies studied with a Lead Director7.

Despite the increased activity of Lead Directors, additional compensation provided for the role continues to be quite different than non-executive Chairs. At median, $28K was provided for the Lead Director role, versus $220K for the non-executive Chair role. In terms of additional compensation, for Lead Directors the pay ranges from $25K to $35K and for non-executive Chairs it ranges from $143 to $260 at 25th and 75th percentiles, respectively. The differential in pay is in line with typical differences in responsibilities. Previously, additional compensation for Lead Directors was steady, at median, at $25K for the last five years. Still, differences exist, somewhat, in role/responsibilities across companies which can impact the level of premium compensation provided for the Lead director role.

Making the decision to provide additional compensation to the Lead Director can send a signal to investors regarding expectations for the role, including time commitment, responsibilities, and authority. Many times, companies have been able to settle (or argue against) shareholder proposals to split the CEO and Chairman roles by instituting (or emphasizing) a strong Lead Director and delineating the specific responsibilities of the position. Boards can also reassure investors concerned about overall governance practices at a company by increasing the Lead Director role/responsibilities. Stock Ownership Guidelines Based on our research, 83% of companies have formal stock ownership requirements. Approximately half of companies studied required directors to defer recognition of equity pay until retirement. The median value of required stock ownership level was $450K.

Detailed Findings

Total Board Compensation

At median, 2013 non-employee director compensation was $260K, generally consistent with 2012.

Pay Mix

The mix of cash and equity paid to outside directors has remained the same for the last 3 years. On average, 56 percent of compensation was equity-based, and 44 percent was cash-based.

Equity Compensation

Full-value equity awards (stock/units) are the most common form of stock-based compensation. Only five percent of companies used stock options in 2013.

|

Vehicle |

2013 |

2012 |

2011 |

|

Full-Value Equity |

95% |

93% |

93% |

|

Stock Options |

2% |

2% |

5% |

|

Both |

3% |

5% |

2% |

Equity awards denominated as a fixed value, as opposed to awards based on a fixed number of shares, continue to increase in prevalence. In 2013, 92 percent of companies denominated equity awards – stock and/or options – based on a fixed value.

|

Award Type |

2013 |

2012 |

2011 |

|

Fixed Value |

88% |

82% |

84% |

|

FIXED Shares |

8% |

11% |

15% |

|

Both |

4% |

7% |

1% |

Committee Compensation

In 2013, just under half of companies studied paid fees specific to committee members (Audit – 48%, Compensation – 35%, and Nominating/Governance – 32%). Given this, at median, committee member compensation was $0. Among companies that do pay separate fees for committee member service, median compensation during 2013 was $15K.

During 2013, additional compensation (premium vs. member) was provided to 96 percent of Audit Committee Chairs, 90% of Compensation Committee Chairs, and 89% of Nominating/Governance Committee Chairs.

Unlike prior years, during 2013 the additional compensation provided to Audit Committee Chairs, at median, was equal to that provided to Compensation Committee Chairs ($20K). The premium provided to Chairs of Nominating/Governance Committees, at median, was lower ($15K).

Lead/Presiding Directors and Non-Executive Board Chairs

Additional compensation is typically provided to Lead/Presiding Directors and non-Executive Board Chairs.

During 2013, median additional pay provided to Lead Directors and non-executive Chairs increased to $28K and $220K, respectively. Previously, median compensation provided to Lead Directors had been flat for five years.

Best in Class Director Compensation Process & Practices

|

Best in Class Director Compensation PROCESS |

|

|

Best in Class Director Compensation PRACTICES |

|

- 1 Analysis excludes privately held companies.

- 2 Total Board Compensation reflects all cash and equity compensation for Board and committee service, excluding compensation for leadership roles such as committee Chair, Lead/Presiding Director, or non-executive Board Chair.

- 3 Audit, Compensation and/or Nominating and Governance committee members.

- 4 Reflects all compensation for committee member service (excludes additional fees for leadership roles), across all Board committees.

- 5 Excludes controlled companies. Also excludes instances where Lead Director role is assumed by Chair of Nominating and Governance Committee, who receives additional compensation for that role.

- 6 Total Board Compensation reflects all cash and equity compensation for Board and committee service, excluding compensation for leadership roles such as committee Chair, Lead/Presiding Director, or non-executive Board Chair.

- 7 Excludes controlled companies. Also excludes instances where Lead Director role is assumed by Chair of Nominating and Governance Committee, who receives compensation for the role.

- Cost of Plan (45% Weighting) – This component will be driven by the SVT model, though ISS will be looking at the cost of plans based on two approaches

- Grants outstanding + shares available for grant + new shares being requested

- Shares available for grant + new shares being requested

- ISS is using this dual approach so as not to put companies who have significant options outstanding at a disadvantage when requesting new shares

- Grant Practices (35% Weighting) – This component will consider burn rate as well as the form of recent grants for the CEO as well as other factors (see ISS link below for complete list)

- Plan Features (20% weighting) – This component will consider factors such as single vs. double trigger on change in control, minimum vesting period, authority for Board to use discretion to vest equity (see ISS link below for complete list)

The results of the scorecard will be compared to relevant benchmark comparison groups[2]. For further details on the EPSC and non-compensation related policies, please visit http://www.issgovernance.com/file/policy/2015USPolicyUpdates.pdf. In addition, to read about CAP’s views on these policies, you can review the comment letter we submitted to ISS at: https://www.capartners.com/news/194/61/Comments-on-ISS-Draft-2015-Proxy-Voting-Policies-U-S

Glass Lewis Released Additional Context and Expectations For “One-Off” Awards

In its 2015 U.S. policy updates related to compensation, Glass Lewis included discussion of how it will analyze special “one-off” awards (e.g., special grants of long-term incentives). While being “wary” of such awards, Glass Lewis has left room to find such awards reasonable with robust disclosure.

“We generally believe that if the existing incentive programs fail to provide adequate incentive to executives, companies should redesign their compensation programs rather than make additional grants…In certain circumstances additional incentives may be appropriate… companies should provide a… convincing explanation of their necessity…”

In its 2015 policy release, Glass Lewis also included some clarification regarding its qualitative and quantitative Say on Pay analysis. For the complete guidelines, visit: http://www.glasslewis.com/assets/uploads/2013/12/2015_GUIDELINES_United_States.pdf

[1] Shareholder Value Transfer assesses the cost of an equity plan relative to a company’s market cap and then compares the cost to industry benchmark

[2] S&P 500, Russell 3000, Non-Russell 3000, Bankrupt companies, recent IPOs as applicable. Burn rate / SVT will be industry specific