- Non-binding advisory votes on Executive Pay and Golden Parachutes

- Independent Compensation Committees, with authority to hire advisors

- Compensation recoupment (“No Compensation for Lies”)

- Additional Disclosure Requirements of pay-for-performance, pay ratios, and employee and director equity hedging policies

Below is a brief description of each of the key provisions impacting executive compensation, along with considerations for companies as they begin to think of the implications of the legislation.

Shareholder Vote on Executive Compensation Disclosures (Section 951)

Advisory Vote on Executive Compensation (i.e., “Say on Pay”)

Description: Companies must submit a resolution to shareholders to approve the compensation of named executive officers

- Vote must occur at least once every three years

- Shareholders must be provided with an opportunity to determine if the vote will take place every one, two, or three years and must be given the opportunity to vote on the frequency every 6 years

- The new requirement will be effective for the first annual shareholder meetings taking place six months after the enactment of the bill, which for calendar year companies means their 2011 shareholder meeting, assuming the bill is signed as expected

Considerations: Companies should examine their compensation programs to ensure program design features have a solid rationale from a shareholder perspective. Consider meeting with key shareholders well in advance of filing the annual proxy statement to explain the compensation program and gain insight on shareholder views of compensation. A recent Compliance and Disclosure Interpretation by the SEC has provided reassurance to companies that they can communicate directly with key shareholders about compensation.

Advisory Vote on Golden Parachutes

Description: In connection with a shareholder vote on a merger or acquisition, companies must submit a non-binding advisory vote to shareholders, including:

- A clear description of any agreements with Named Executive Officers that will be impacted by the merger or acquisition

- Non-binding shareholder advisory vote on any agreements, to the extent not previously subject to the general shareholder advisory vote on executive compensation

Considerations: Vote may have narrow implications as it only covers new agreements or modified agreements in advance of a change in control that have not already been covered under a non-binding shareholder advisory vote. In addition, it does not cover the total change in control costs a company may incur, but only those that relate to the Named Executive Officers. However, as change in control agreements are a key area of focus, such agreements should be reviewed to ensure that agreements are in line with current and emerging practices.

Compensation Committee Independence (Section 952)

Compensation Committee Independence

Description: The Act requires companies to ensure that all members of the Compensation Committee are independent (with limited exceptions), otherwise they cannot be listed by a national securities exchange. Independence will be assessed considering sources of compensation received by the director and affiliation with the company.

Considerations: Companies that have directors not meeting these criteria will need to modify the Committee membership.

Independence of Compensation Consultants and Other Compensation Committee Advisors

Description: The Compensation Committee may only select an advisor after taking into consideration specific factors identified by the SEC. Factors to be considered will include the following:

- Provision of other service to the Company by the advisor

- Amount of fees received from the Company relative to the firms total revenue

- Policies and procedures of the advisor to resolve conflicts of interest

- Business or personal relationships between the advisor and Compensation Committee members

- Stock ownership in the Company by the Advisor

Considerations: Following guidance from the SEC, Compensation Committees will likely want to document that they have reviewed these factors prior to selecting outside advisors.

Compensation Committee Authority Relating to Compensation Consultants

Description: The Compensation Committee has the authority to retain the advice of a compensation consultant and the Company will provide appropriate funding. Compensation Committees are required to disclose the relationship and whether any conflicts of interest arose and how they are being addressed. However, Committees are not required to hire an advisor.

Considerations: Many companies have already provided clear disclosure of the nature of the reporting relationship with the compensation consultant. They may need to enhance the disclosure slightly to clarify that they are in compliance with the new legislation.

Executive Compensation Disclosures (Section 953)

Disclosure of Pay Versus Performance

Description: Companies are required to disclose the relationship between executive compensation and the financial performance of the company, possibly through a graphic presentation.

Considerations: Compensation appears to be defined as compensation actually paid as disclosed in the Summary Compensation Table. For share-based compensation, this may be misleading, as the realized value of the compensation may be very different from the grant value of the compensation. Specific guidance from the SEC is needed to implement this proposal.

Disclosure of Pay Ratio

Description: Companies are required to disclose the ratio of the median annual total compensation of all employees of the issuer (excluding the CEO) to the annual total compensation of the CEO.

Considerations: SEC guidance is required to implement this provision, as for most companies it will be challenging to determine the median compensation of all employees on a comparable basis to the Summary Compensation Table compensation of the CEO.

Recovery of Erroneously Awarded Compensation (Section 954)

Description: Companies will need to develop and implement a policy that provides for the recovery of compensation from current or former executive officers following a financial restatement due to material noncompliance with financial reporting requirements. Policy will apply to any incentive-based compensation (including stock options awarded as compensation) during the 3-year period preceding the date of the restatement.

Considerations: The proposal is more stringent than most clawback policies currently in-effect as it does not require executive misconduct to trigger recoupment. The policy may be challenging to implement in practice for some forms of compensation (e.g., stock options) as it may be difficult to determine the value that needs to be recovered following a restatement.

Disclosure Regarding Employee and Director Hedging (Section 955)

Description: Companies are required to disclose whether any executive or director is permitted to purchase financial instruments that are designed to hedge or offset a decrease in the market value of the company’s stock.

Considerations: Companies that have not already adopted an anti-hedging policy should consider doing so to ensure that they do not have to disclose that executives and directors are permitted to hedge positions in the company’s stock.

Conclusion

The Act will have a significant impact on executive compensation in the near-term as companies work to comply with the new requirements and prepare for “Say on Pay”. Additional guidance from the SEC is expected to assist companies in complying with the new rules. However, given the mandatory “Say on Pay”, a key area of focus for companies should be ensuring that shareholders understand and support the executive compensation program. Two actions that can assist in this are direct conversations with key shareholders and ensuring that the company’s CD&A provides a clear rationale for the compensation program and an easily understandable description of compensation decisions.

***

Please contact us at (212) 921-9350 if you have any questions about the issues discussed above or would like to discuss your own executive compensation issues. You can access our website at www.capartners.com for more information on executive compensation.

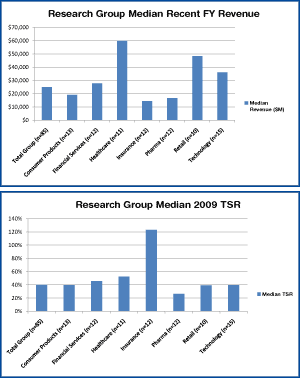

The component companies are large industry leaders. The total sample had median revenue of $25B, market cap of $37B and Total Shareholder Return (TSR) of 40% during 2009. The charts below include summary statistics by industry group. Practices at these leading companies are scrutinized closely by shareholders and the shareholder advisory groups. The responses of these companies to the financial strains in the economy during 2009 gives valuable insight into current practice and changes we expect to see in 2010.

What We Found

Highlights of our research results for the entire sample are below. Future CAP-Flashes will focus on particular industry groups and important topical areas, such as annual and long-term incentive design trends.

Compensation Strategy Changes

Outside of Financial Services, few companies reported changes to compensation strategy—i.e., the targeted pay positioning for executives and the targeted pay mix. Most stayed the course despite the challenging economic conditions in 2009.

Within the Financial Services group, most companies reported changes to compensation strategy, responding to their experience under TARP. Changes within the financial services industry include different pay mixes—examples include:

- Increased emphasis on fixed compensation by reducing incentive compensation and increasing base salary

- Increased emphasis on at risk, incentive compensation

- Majority of compensation delivered in restricted stock, deferred for 5 years

- Reduced portion of bonuses paid in cash and increased the portion of bonuses paid with deferred long-term awards subject to clawback

We expect Financial Services companies to continue to re- evaluate their compensation strategies as they exit TARP and emerge from the financial crisis and enter a more steady state.

Peer Groups Used For Benchmarking

Most companies did not make significant changes to their peer groups used for compensation benchmarking. Of those that did make changes, the majority of changes reported were primarily due to M&A activity in the Consumer Products, Insurance and Pharmaceutical industries. Others tweaked their selection criteria to focus more on companies in their industry and within a reasonable size range.

Base Salary Actions

Senior executive base salary actions continued to be restrained by the poor economy in 2009. Slightly more than half the sample did not increase or reduced salaries in 2009. Industry groups where salary freezes and reductions were widespread included Consumer Products, Health Care, Retail and Technology. Industries where salary increases were more common included Insurance and Pharmaceuticals. Merit increases were generally in the range of 2 – 3% when they were awarded.

| Type of Salary Change Reported in 2010 CD&A | No. of Cos. | % of Cos. (n = 85) |

| No Increase / Salary Freeze – All NEOs | 32 | 38% |

| No Increase / Salary Freeze – CEO Only | 6 | 7% |

| No Increase / Salary Freeze – Select NEOs | 1 | 1% |

| Salary Reduction – All NEOs | 4 | 5% |

| Salary Reduction – CEO Only | 1 | 1% |

| Salary Increase – All NEOs | 17 | 20% |

| Salary Increase – Select NEOs | 14 | 16% |

| Salary Increase – CEO Only | 1 | 1% |

| Salary Increase – TARP Related | 6 | 7% |

| Not Specified | 11 | 13% |

Note: Percentages do not add up to 100% due to multiple responses.

Annual Incentive Plan Design

Overall, 34 companies (40% of the full sample) disclosed making a change to their AIP design in 2009 or for 2010. While there was not a universal trend in the type of design changes being made, most companies are dealing with challenges in the goal setting process and maintaining meaningful performance linkages, linking rewards to the company’s ability to pay, and appropriately considering the impact of overall market conditions. In a nutshell, companies are trying to maintain a precise pay and performance calibration while also allowing for appropriate recognition of significant executive accomplishments.

The breakdown of reported AIP changes is as follows:

| Type of Change Reported in 2010 CD&A | No. of Cos. | % of Cos. Reporting Changes (n = 34) |

| Change in performance metrics used to fund awards | 15 | 44% |

| Increased target award opportunities | 9 | 26% |

| Reduced maximum award payout leverage | 4 | 12% |

| Added discretionary award component | 3 | 9% |

| Use of performance scorecard | 3 | 9% |

| New annual incentive plan (overhaul) | 2 | 6% |

| Other changes | 3 | 9% |

Note: Percentages do not add up to 100% due to multiple responses.

Change in Performance Metrics

Of the companies that changed their performance metrics and/or the mix of those metrics, a majority created a stronger linkage to corporate performance results and strategic priorities to support business changes forced by economic conditions. For example,

McKesson: For FY 2010, bonus goals need to significantly exceed the strategic plan to earn a target payout

Computer Sciences: Reduced the number of performance criteria to focus on key financial goals consistent with the company’s business strategy

T. J. Maxx – Eliminated divisional performance measures and focused on total company income

Sara Lee: Eliminated individual objectives and reallocated to corporate adjusted operating income goal

Merck: For 2010 incentive pool will be determined solely on company performance (as reflected by company scorecard)

There was no distinct trend in the changes made to the financial metrics used, though many changes included more emphasis on earnings, and to a lesser degree, revenue growth. Companies in the Insurance, Pharmaceutical and Retail industries made the most changes to metrics.

Discretion and Broad Performance Assessments

Some companies are increasing the role of discretion or broader retrospective performance assessment, to help ensure that significant market factors are considered at year end. For example, Genworth’s compensation committee uses discretionary judgment of performance against strategic objectives, including key financial criteria, to determine payouts. Microsoft’s compensation committee uses business judgment to help determine awards, and considers executive performance across a range of financial, operational, and strategic measures.

Another approach used by some companies includes use of a scorecard, which typically provides parameters for financial, operational, strategic, customer, and/or individual performance measurement. BNY-Mellon adopted such an approach to determine annual bonuses; and for 2010 Merck disclosed new incentive pool funding based on a company scorecard (solely company performance).

Changing Long-Term Incentive Practices

Most companies made changes to long-term incentive programs that either took effect in 2009 or will become effective in 2010—70% (60 out of 85) of companies reported changes. The most commonly reported changes involved changes to the mix of long-term incentive award vehicles granted and changes to the metrics used for long-term incentives. Here is a breakdown of what we found:

| Type of Change Reported in 2010 CD&A | No. of Cos. | % of Cos. Reporting Changes (n = 60) |

| Different mix of award vehicles | 33 | 55% |

| Different long-term performance metrics | 23 | 38% |

| Change in size of long-term award guidelines | 12 | 20% |

| Limits on dividend equivalents | 7 | 12% |

| Change in leverage in performance scales | 6 | 10% |

| Other changes | 9 | 15% |

Note: Percentages do not add up to 100% due to multiple responses.

Long-Term Award Mix

Among the companies that changed the mix of long-term award vehicles, two trends emerged. More than 50% of companies reporting a change in long-term award mix increased the emphasis on performance-based awards. Increased use of time-based awards – particularly among companies that had difficulty setting long-term financial goals during the recent period of economic uncertainty—was also common, but much less so. Finally, a few companies used options to a greater extent citing the difficulty in setting goals and attractive stock prices.

| Changes In Long-Term Incentive Award Mix | No. of Cos. | % of Cos. Reporting Changes (n = 33) |

| Greater emphasis on performance-based awards | 18 | 55% |

| Greater emphasis on time-based restricted stock/unit awards | 8 | 24% |

| Greater emphasis on options | 3 | 9% |

| Other | 4 | 12% |

Size of Long-Term Award Guidelines

Relatively few companies – only 14% of the total sample of 85 companies and 20% of the companies reporting changes to long-term programs—reported changing the size of long-term award target guidelines in 2009. Of the companies reporting a change, 67% decreased award guidelines and 25% increased award guidelines. One company reported migrating from fixed share guidelines to value-based guidelines, but did not indicate whether the change represented an increase or a decrease in value.

Long-Term Performance Metric Changes

Changes in long-term performance metrics were widespread. 25% of the total sample reported changing long-term incentives by adding new metrics; an additional 4% reduced the number of metrics used. Both relative and absolute TSR were selected as metrics by a number of companies. Return on equity/capital, revenue growth and cash flow were also popular choices.

| New Performance Metric | No. of Cos. | % of Cos. (n = 21) |

| Relative TSR | 5 | 24% |

| Absolute TSR of Stock Price Growth | 3 | 14% |

| Return on Equity or Capital | 4 | 19% |

| Revenue Growth | 3 | 14% |

| Cash Flow | 3 | 14% |

| Other Financial Metrics | 7 | 33% |

Note: Percentages do not add up to 100% due to multiple responses

Treatment of Dividend Equivalents and Other Plan Changes

Changes in the treatment of dividend equivalents was the most common plan design change reported. Seven companies moved to limit the payment of dividend equivalents until shares were earned or vested. Other design changes were more subtle, such as changes to the length of performance periods or the amount of leverage in performance scales.

Conclusions

Absent regulatory constraints, we did not see wholesale changes in 2009. Companies tended to stay the course in 2009 as the economic cycle bottomed out and the first signs of a recovery began to appear, but several clear trends did emerge. These include continued restraint on base salary increases, refinements to annual incentive and long-term incentive plan metrics and greater use of performance based long term incentives. These are all shareholder friendly developments that should improve the alignment between executive compensation and shareholders. We expect companies to continue to re-examine their programs as the economy improves and shareholders continue to demand performance and compensation program alignment.

***

Please contact us at (212) 921-9350 if you have any questions about the issues discussed above or would like to discuss your own executive compensation issues. You can access our website at www.capartners.com for more information on executive compensation.

| Each pay consulting relationship is unique. Once the consultant is selected, the committee should define in advance its objectives and expectations. |

Board compensation committees must not only deal with the competing demands of regulators and shareholders, but must now operate in an environment where their actions and decisions are highly visible and often criticized. For many boards, hiring an out-side compensation consultant to help them navigate this highly complex environment is a worthwhile and prudent business decision. A consultant can help the committee fulfill its oversight and governance responsibilities while maintaining competitive, compliant, and responsible executive pay.

In this article, we discuss how the compensation committee and the compensation consultant can have an effective relationship. The process begins with the compensation committee defining its objectives and expectations and hiring the consultant. We then discuss procedures that emphasize communication and facilitate productivity.

A mutually beneficial consulting relationship will require considerable dialogue. When the relationship is built on a solid foundation, differing points of view can be addressed without detriment to the ongoing consulting relationship.

An effective consulting relationship begins with the selection process. The human resources department or procurement may begin the process with a “request for proposal.” However, the process should be driven by the compensation committee itself. Selection criteria should be identified as well as any required skills, knowledge, or experience. Often, experience in a particular industry, or experience with a specific transaction, such as an IPO or merger is important. If the company is expanding internationally, global resources and data may be needed.

The full compensation committee should be involved in interviewing the consultant or team, and they should assure that those they are interviewing will be the ones involved in the engagement. The committee must be comfortable with the consultant’s experience on similar issues facing the company, with the consultant’s technical acumen, access to available resources, and ability to present a coherent and well thought-out point of view. The consultant’s references should also be checked.

| Where the committee is not experienced in working with outside advisors, the consultant can help structure objectives and processes that work. |

Each consulting relationship is unique. A start-up company, an IPO, or a newly merged or acquired company may need help with virtually every aspect of employee pay design. Other companies may need an overall review of management’s pay recommendations and expert opinion to the committee at each meeting. Others may need specific technical expertise (a company in Chapter 11; one that has received TARP monies, etc.)

Once the consultant is selected, the committee should define in advance its objectives for the year and its expectations of the consultant. This need not be an involved or lengthy process, but in any working relationship, purpose and context need to be provided.

For example, if the compensation committee needs education and training on executive pay issues and practices, it should inform the consultant. If the committee is not comfortable with the design of the incentive plans that have provided lucrative payouts while stock price remained flat, the consultant should know about it. If there is disagreement over Ike CEO’s pay or the pay and performance linkage, the consultant should be alerted.

Certainly, if the prior consultant did not meet the expectations of the committee, the new consultant should be told why. Where the compensation committee is not experienced in working with outside advisors, the consultant is in an excellent position to help structure objectives and processes that work.

Most of all, the committee relies on the consultant for experience and expertise, to help ensure that the company is not exposed in terms of inappropriate pay practices. Ultimately, the overall goals of the compensation committee and consultant are the same: to help the board perform its governance and oversight role in an informed manner.

| It is surprising how often committee chair/ consultant dialogue does not happen or comes too late to avoid a problem. |

Throughout the year, the compensation committee and consultant should adhere to certain practices that will lead to a successful working relationship. There will still be challenges and tough issues to work through together, but these processes will help materially in achieving committee objectives.

- At the beginning of every year, the consultant should develop a “statement of work” that defines the scope of their consulting activities for the coming year, including deliverables, fees, timing, and reporting relationships to the committee. If there is an annual calendar of meeting dates and activities, the statement of work is straightforward. Since the human resource function is typically responsible for the annual calendar, this planning helps to ensure that all parties have a common understanding for the year ahead.

- If the committee has not done so already, its goals and objectives should be articulated to the consultant. This should include objectives for the consultant, but might also include objectives for the committee itself. The committee chairperson should also alert the consultant to any critical issues facing the committee.

- In a new relationship, the committee will often request that the consultant provide a high-level review of the company’s executive pay program, highlighting any atypical or uncompetitive pay practices or plan features that should be reviewed in detail. It is incumbent on the consultant to uncover potential problem areas that need to be addressed.

- The committee chairperson and consultant should review meeting materials in advance of each meeting, preferably before the materials are mailed, which allows for revisions. This allows both parties to understand each other’s point of view and pose questions that will help in meeting preparation.

- The consultant should assure that the chair under-stands the key messages to be delivered on a particular topic. The chair, in turn, can use the opportunity to bring the consultant up to speed on any strong committee views or business issues that may be relevant to the subject matter at hand. This could include plan design, competitive analysis, the CEO’s contract or pay recommendations. It is surprising how often this dialogue does not happen, or comes at the last minute when it is often too late to resolve an issue or avoid a problem during the meeting.

- The consultant should be available for every meeting and executive session, as requested by the chairperson. Time should be scheduled for debriefing, particularly when follow-up activities are required. When the meeting agenda is full, or when many decisions have been made, follow-up ensures that everyone has similar takeaways.

- The committee’s annual calendar typically includes a review of compensation strategy, annual pay benchmarking, assessment of the pay and performance relationship, and risk assessment. At the most basic level, both parties should work to avoid controversial pay practices, ensure that pay programs support company strategy, and establish appropriate performance linkages for incentive plans. These are joint responsibilities. Any review of CEO pay (with recommendations) should go to the chairperson first, without prior review by the CEO.

- The performance of outside advisors should be evaluated as part of the committee’s annual self -evaluation. Even if the consultant assists the committee with the evaluation, it is important that the members review the overall relationship each year to determine if the consultant is meeting expectations. Feedback should be provided to the consultant.

- At the end of each year, management (usually human resources) should provide the committee with documentation on the consultant’s fees and deliverables for the year. A summary of all services and fees provided by the consultant’s firm to the company overall should also be provided.

- As part of the committee’s review of the proxy Compensation Discussion and Analysis (CD&A), the required language describing the consultant’s involvement in pay decisions should be reviewed, as well as other needed disclosure.

- There should be a clear process for requesting and approving additional work for the consultant during the year. If management has a need for additional work, the committee should approve it. If the amount of work the consultant’s company does overall is significant, the committee may want to know about such work in advance.

| In today’s environment, the compensation committee cannot be passively waiting for problems to occur. It relies on the consultant to uncover relevant and timely pay issues. |

The processes described above will contribute to a productive relationship between the compensation committee and its consultant. The following success factors can strengthen the relationship even more.

| The consultant should not play both sides of an issue, and has a responsibility to express an opinion even if it is not one shared with the chair, the committee or the CEO. |

- The chairperson and consultant must have access to one another during the year. They should communicate before and after each meeting, and whenever necessary.

- Both parties must have realistic expectations about the relationship. They may not always agree on every issue, but this is not a signal of failure or dysfunctional relationship. The committee must be open to views and opinions different from its own, and consultants must understand that their responsibility is to voice opinions to the committee, even if it is not what the board (or CEO) wants to hear.

- The committee and consultant should proactively review company pay programs and practices, while anticipating potential issues or necessary changes. In today’s environment, the compensation committee cannot be reactive and wait for problems to occur. The consultant must uncover relevant and timely issues.

For example, if the company intends to seek shareholder approval of a new long-term incentive plan share reserve, the committee should research the voting policies of their largest institutional investors before making the request. When advisory groups introduce new policies, companies should review their programs to anticipate any problem areas that could arise. The committee should also involve the board’s audit or risk committee in an annual evaluation of pay programs as it relates to risk.

- Understand that the ultimate decision-making is the responsibility of the compensation committee, not the consultant. The committee needs to exercise its own judgment after getting the best information and advice possible.

In the past year, consultant independence has come to the forefront. Since 2006, if a consultant played a role in determining or recommending executive or director pay, the consultant had to be identified in the company’s proxy and the scope of services and reporting relationship had to be noted. SEC rules approved in December 2009 expanded the requirement to include the fee disclosure if a consultant provides additional services to the company beyond $120,000 in the aggregate. Also in 2009 draft legislation delivered from the Treasury Department to Congress included a provision that any compensation consultant or legal counsel hired by the compensation committee must be “independent” from management.

Most full-service consulting firms have independence standards to manage any potential conflicts, while a boutique firm specializing only in executive compensation is generally structured to reduce the potential for conflict.

Treasury Department Fact Sheet

Providing Compensation Committees With New Independence

Draft legislation was delivered by the Treasury Department to Congress in 2009 to promote the independence of compensation committees. Key elements would include:

- Compensation committee members will be required to meet stronger standards for independence that are to be issued by the SEC.

- To ensure that compensation committees receive objective advice, any compensation consultants and legal counsel hired by the committee must be independent from management.

- Committees must be given the authority and funding to hire independent consultants, outside counsel, and other advisors who can help ensure that the committee bargains for pay packages in the best interests of shareholders.

The compensation committee should also have procedures in place regarding the consultant relationship (hiring and firing authority, direct access to the committee, performance evaluation, executive sessions, etc.) that help ensure objective advice, as well as a protocol on mitigating conflicts. Absent a mandated definition of consultant independence, what is important is that the committee be satisfied with the relationship and that there are procedures to avoid conflict.

A related issue which has attracted increased attention is the use of more than one compensation consultant. If two consultants are used (one reporting to the compensation committee, the other to management) the roles should be clearly defined and agreed to in advance. The predominant view is that one consultant reporting to the committee is a more effective arrangement, but the dual consultant model is certainly workable.

To have an effective working relationship, both the compensation committee and the consultant have specific roles to play.

Outside compensation consultant. It is expected that the consultant know the company and industry and stay current on all regulatory issues, as well as best practices in plan design, performance measurement, and pay practices. The consultant should not play both sides of an issue, and has a responsibility to express an opinion even if it is not one shared with the chairperson, the committee, or the CEO. Above all else, the consultant needs to be a “trusted advisor” helping the committee think strategically, raising questions and issues the committee should be thinking about.

Compensation committee. Many committee activities are dictated by various regulatory bodies (stock exchanges, the SEC. FASB, etc.), or specific legislation, such as Sarbanes-Oxley. At a tactical level, each committee must follow its charter to ensure members are fulfilling their responsibilities.

The committee also needs to work with other committees of the board (audit, nominating/governance, risk, etc.) and keep the full board informed of decisions, particularly on CEO compensation. The compensation committee chairperson should develop a healthy working relationship with the CEO.

The committee itself should maintain adequate skills among its members. Diverse areas of expertise and complementary skills are a plus, and basic financial acumen a necessity. Most importantly, the committee must represent the shareholders.

While the formal reporting relationship of the consultant must be to the committee, a good working relationship between the consultant and management can have an extremely positive impact. Management provides necessary compensation data and financial or legal information. Management can also confirm data accuracy and timeliness, and provide a historical perspective or rationale for unusual pay practices. It can explain how certain programs are implemented (such as company specific definitions for metrics used in incentive plans.)

A good relationship with management can also help provide information on the various viewpoints held on pertinent issues, and offer insights on culture and business strategy. In many cases, pre-committee meeting conference calls and preparation may involve the consultant, the compensation committee chair, and human resources. When all three parties are involved, productivity in the committee meetings can be greatly enhanced. Open communication, where appropriate, contributes to better working relationships overall.

| A good working relationship between the consultant and management is a positive. Management provides necessary pay and financial information, plus insights on culture and business strategy. |

Executive compensation is a sensitive area. Such factors as company performance, personal views on pay, or a shareholder vote against committee members can temporarily change committee dynamics. Additionally, problem areas can arise: a mistake may be made as a result of not having current data; meeting participants may not be fully prepared when a specific issue arises that was not on the agenda; a committee member may question a methodology used by the consultant; or the consultant may be caught in the middle of two disparate views. Most issues can be worked out. The important thing is for the chairperson and consultant to acknowledge a problem when it occurs, accept responsibility for their role in the misunderstanding, and focus on action to correct the problem.

In the future, the need for compensation committees to work effectively with consultants will increase as new regulations take effect and companies work their way out of the current recession. The committee’s role and potential impact – as well as its exposure to public scrutiny – will not diminish.

Nonetheless, along with greater demands and challenges comes the opportunity to make meaningful decisions in shaping pay programs. In many companies, this will ultimately result in pay strategies and programs that are tightly aligned with the competitive market and meaningful returns to shareholders

Please contact us at (212) 921-9350 if you have any questions about the issues discussed above or would like to discuss your own executive compensation issues. You can access our website at www.capartners.com for more information on executive compensation.

Reprinted by THE CORPORATE BOARD

4400 Hagadorn Rd, Okemos, MI 48864-2414, (517) 336-1700

www.corporateboard.com @ 2010 by Vanguard Publications, Inc.

Following the collapse of Enron and WorldCom, compensation committees became aware of the dangers of loading up executives with outsized stock option grants which might tempt them to “inflate” short-term earnings and stock price. Companies and their compensation committees did one or more of the following: they reduced the size of option grants, introduced stock ownership guidelines and share retention programs, and diversified the portfolio of incentive vehicles by adding restricted stock and performance plans. These long-term incentives contain less leverage than options, reducing the temptation to swing for the fences.

Incentive compensation, whether for executives or the broader employee population, has been identified as a significant contributor to the financial crisis. To protect the “safety and soundness” of our financial system and provide remediation, the Federal Reserve and the Securities and Exchange Commission have proposed guidance and disclosure requirements which require companies to conduct a thorough review of the relationship between pay and risk taking. The objective of a “risk assessment” is to identify plans or practices that may encourage employees to take unnecessary or excessive risk which could threaten the company or, in the case of financial firms, the safety of the broader financial system.

Conducting a Risk Review

There are four steps in conducting a risk review:

- Create the process

- Develop a framework to examine incentive plans and practices

- Assess current plans

- Communicate results and identify refinements

Creating the Process

A comprehensive risk review requires a multi-disciplinary team composed of human resources, risk management, legal, finance, and corporate and business unit leaders. In the initial phase human resources professionals (including compensation) compile comprehensive information about the company’s incentive plans. This includes identifying all incentive plans, revisiting the organization’s compensation philosophy (including the appropriateness of the comparators used for benchmarking), summarizing key incentive plan design features, and reviewing historic pool levels and pay mix to determine if a “risk adjustment” is needed. Concurrently, risk and finance professionals compile a risk profile by bringing together their individual assessments of where risk exists or is likely to originate.

Developing a Framework for Examining Incentive Plans and Practices

The next step is to develop a framework for determining to what extent risk impacts incentive plans and practices. The team identifies the types of risk — operational, credit, market, and reputational — that exist in the company and the behaviors and actions that need examination and monitoring. Although all incentive plans should be reviewed, the focus initially will be on the lines of business and the individual contributors with higher risk profiles. The framework includes a series of questions relating to how the incentive plans operate. The following address the key areas of concern:

- How are incentive pools developed?

- Are the incentive pools capped or uncapped?

- Are the metrics appropriate given the type of business?

- Are operational controls in place to prevent participants from manipulating results?

- Is the plan unduly focused on short-term results?

- Do incentive timeframes match income recognition?

It is also important to examine incentive plan governance:

- Who designs the plans?

- Who approves the plans and how are they tracked?

- Who validates the performance and payments?

- What is the level of oversight by finance, risk management, human resources, senior management?

The framework can also identify design features that help to mitigate risk, e.g., a combination of performance metrics (ideally including multi-year results), a pay mix that balances short-term and long-term compensation, and incentive leverage scales that encourage performance improvement without requiring home runs.

SEC Disclosure Rules (approved December 16, 2009)

- The SEC requires a narrative disclosure about the company’s compensation policies and practices for all employees, not just executive officers, if the compensation policies and practices create risks that are reasonably likely to have a material adverse effect on the company

- This disclosure threshold is similar to the one used for the Management Discussion and Analysis

- Disclosure would be included in a separate section of the proxy, not in the Compensation Discussion and Analysis

- The SEC provides a non-exclusive list of situations that potentially could trigger disclosure:

- At a business unit of the company that carries a significant portion of the company’s risk profile;

- At a business unit with compensation structured significantly differently than other units within the company;

- At a business unit where the compensation expense is a significant percentage of the unit’s revenues; and

- At a business where bonuses are awarded upon accomplishment of a task, while the income and risk to the company from the task extend over a significantly longer period

- Smaller reporting companies are excluded

- Companies are not required to make an affirmative statement that compensation plans are not risky

Note: While the SEC does not require disclosure if a company determines that its incentive plans are not reasonably likely to create risks with material adverse consequences, we expect companies to describe the risk assessment process in their proxy statements, highlighting features of their programs that mitigate risk and changes they have made to improve risk and incentive alignment.

Assessing Current Plans

The first plan to review is the executive incentive plan. It is important to validate both the plan and the compensation philosophy against the company’s risk profile as other plans will be aligned with these principles. In fact, many of the issues addressed with respect to senior executives will apply to other employees.

The compensation committee and the chief risk officer (and often the risk committee or audit committee of the board of directors) participate in this process. An analysis of the metrics used to fund the corporate pool is particularly important. For example, financial firms need to address whether incentive plan metrics include capital adjusted results. Companies also need to demonstrate that incentive plan payments reflect a broad view of performance that extends beyond short-term earnings. The balance in the senior executive pay package between short-term, intermediate, and long-term results, and between cash and equity compensation are important to consider.

Many plans have features which can mitigate risk, such as multi-year performance periods, stock ownership guidelines and stock retention requirements, bonus and equity claw backs if results are later found to be inaccurate, and mandatory bonus deferrals. While these practices do not guarantee that unnecessary risk taking is being averted, they do encourage the desired alignment between senior executive pay and long-term performance.

Next, the multi-disciplinary team conducts a similar analysis of other incentive plans. This usually begins by analyzing how the bonus or incentive pools are funded, i.e., whether they use corporate, business unit, or individual results, and whether the pools are based solely on formulas or include an element of management judgment. It is important to examine how the metrics used align with corporate plan metrics and business goals. One important practice to mitigate risk includes incorporating time horizons in the incentive plan that reflects the company’s time horizon for recognizing income or losses. When products or transactions contain a long tail that can only be assessed over time, multi-year performance should impact incentive payouts. A major mismatch can occur when large upfront bonuses are awarded before the company is able to recognize profitability from a product or transaction. Other questions to be addressed are similar to those already covered in the assessment of the executive incentive plan:

- Does fixed compensation represent an appropriate percentage of the total pay package?

- Are safeguards (such as caps, discretionary components, deferrals and controls over how products are priced) in place for revenue-based plans?

- Does the mix of cash and equity reflect the preferred alignment between the business unit or individual participant and the company?

- What is the process for goal setting and approving payouts? Is the Audit Committee involved in the performance measurement approval for the executive plans?

- Are claw backs and mandatory deferrals in place? If not, should they be adopted?

Finance, risk management, and human resources should have an ongoing role in developing and reviewing business unit compensation plans. They need to have the authority to make recommendations for change. They also need to be compensated in a manner that ensures that their independent oversight of the process is not compromised.

Communicating Results

Led by the chief risk officer, the team presents its assessment to management and the compensation committee. This consists of an evaluation of executive and other employee incentive plans that have the potential to create unnecessary or excessive risk (the threshold for financial institutions) or that are reasonably likely to create a material adverse effect on the company (see SEC Disclosure Rules).

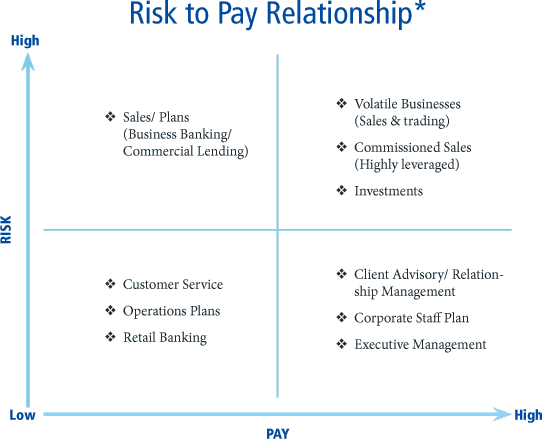

The presentation highlights businesses with higher (and lower) risk profiles, the criteria used to assess the risk, and an analysis of the corresponding incentive plans and how they are structured to mitigate these risks. In organizations with multiple incentive plans, it is common to sort the plans by level of risk, (from high to low) and by the level of pay (from high to low) for purposes of prioritizing the review process, examining individual plan features, and presenting findings and recommendations (see Risk to Pay Relationship chart on page 4). The team offers an opinion on whether any of the incentive plans are likely to constitute a material adverse risk, or in financial firms, whether the incentive plans align with the Federal Reserve’s guidance on “safety and soundness.” Finally, the team presents to the compensation committee recommendations on how the company’s incentive plans, policies, and practices should be structured or modified to address risk. These modifications may be company-wide (e.g., a shift in some portion of variable to fixed pay for all employees), or may be refinements affecting a smaller group of employees (e.g., a three-year deferral program with payment tied to future business unit results). In almost all cases, some changes are to be expected.

* Based on a financial services firm but the principle is applicable across industries

Given the increased focus on risk management and the responsibility of compensation committees and boards to supervise the potential for incentive plans to encourage excessive risk taking, we expect most companies will develop processes to identify and address these issues. Additionally, while the SEC does not require companies to make any affirmative disclosure if they do not believe that their incentive plans create risks with material adverse consequences, we expect many companies to describe the risk assessment process in their proxy statements.

A risk review is not a one-time event. In the future, incentive plans will be more regularly monitored and reviewed by a designated internal group with the authority and independence to raise issues and make recommendations. This kind of enhanced management oversight represents sound business practice. Companies that establish an accepted and understood pay to risk relationship will be better positioned to achieve strategic business goals while maintaining responsible and defensible incentive compensation programs.

Please contact us at (212) 921-9350 if you have any questions about the issues discussed above or would like to discuss your own executive compensation issues. You can access our website at www.capartners.com for more information on executive compensation.

Based on the dialogue we have seen among compensation committees, we believe the 2010 proxy season will demonstrate that a new level of responsibility has taken hold. Management and committees are struggling to ensure they are doing the right thing when it comes to compensation and that pay is closely aligned with performance. Additionally, some of the incentive program designs and governance practices imposed on financial services companies operating under TARP have had an impact on other industries.

Some of the early trends we are seeing in 2010 are detailed below.

Base Salaries

In 2009, roughly one-third of companies did not give salary increases. Many companies even cut salaries for executives, typically by 5-10%. With the economy showing early signs of a recovery, close to 90% of companies are planning for salary increases in 2010. Merit pools are expected to be lower than pre-recession levels, typically ranging from 2-3%. While many companies are providing salary increases, they will use these smaller pools more strategically, by targeting top performers and highest potential executives, and withholding increases to others.

RiskMetrics Group Problematic Pay Practices

While not a complete list, RMG views the following as problematic pay practices:

- Multi-year guarantees for salary increases, non-performance based bonuses, and equity compensation;

- Including additional years of unworked service that results in significant additional benefits, without sufficient justification, or including long-term equity awards in the pension calculation;

- Perquisites for former and/or retired executives, and extraordinary relocation benefits (including home buyouts) for current executives;

- Change-in-control payments exceeding 3 times base salary and target bonus; change-in-control payments without job loss or substantial diminution of duties (“single triggers”); new or materially amended agreements that provide for ‘modified single triggers’ (under which an executive may voluntarily leave for any reason and still receive the change-in-control severance package); new or materially amended agreements that provide for an excise tax gross-up (including “modified gross-ups);

- Tax reimbursements related to executive perquisites or other payments such as personal use of corporate aircraft, executive life insurance, bonus, etc;

- Dividends or dividend equivalents paid on unvested performance shares or units;

- Executive using company stock in hedging activities, such as “cashless” collars, forward sales, equity swaps or other similar arrangements; or

- Repricing or replacing of underwater stock options/stock appreciation rights without prior shareholder approval (including cash buyouts and voluntary surrender/subsequent regrant of underwater options)

In the financial services industry, given the impact of TARP and other regulatory initiatives, compensation is being re-mixed. Many financial service firms had increases to rebalance the mix between fixed and variable compensation. This helps avoid any perception that leveraged compensation packages encourage excessive risk-taking. In addition an annual risk assessment is becoming integral to the committee’s process across industries (this topic will be covered in the upcoming CAPflash on Risk Assessment).

Annual Incentives

Many companies’ experiences during two recessions within the last decade have highlighted the challenges with setting targets for incentive plan purposes. Beginning in 2009, many companies have started to incorporate a greater level of discretion in their annual incentive plans.

Companies found that strictly formulaic incentive plans sometimes failed to capture the true quality of the financial performance delivered. Additionally, Committees increasingly want the ability to improve the alignment between pay and performance. Providing for a level of discretion over incentive payouts allows Committees to recognize non-financial factors, individual performance and the challenges management faced in delivering the financial results on a retrospective basis.

For 2009 payouts, we expect to see an increased use of discretion by compensation committees, with more in-depth analysis of the factors influencing payout decisions. This may include a review of multiple financial metrics, analysis of performance relative to peers, strategic and operational results.

While results will vary by industry, we expect 2009 annual incentives payouts to exceed 2008 levels, when many companies paid zero or below target awards.

Long-term Incentives

In 2009, companies struggled to reconcile collapsing share prices with the need to recognize and reward their top performers and rising stars. Many companies did not grant equity as deeply or as broadly as they had in the past. In many cases, we saw a reduction in long-term incentive awards ranging from 10% – 30%. This decrease was partly due to efforts to manage annual share usage in a year with significantly lower stock prices In 2010, we are expecting grant values to level off or increase slightly as stock prices recover. We also expect to see a continued focus on performance-based long-term incentive plans and a decline in the use of or emphasis on stock options.

In 2010, individual differentiation will continue to be a key theme in long-term incentives as companies continue to manage their share usage and overall expense. The most dramatic examples occur deeper in the organization. At middle management levels, 100% may be eligible for awards, but typically 50%, and in some companies as few as 25%, actually receive awards.

Time-vested restricted stock and “salary stock” has become commonplace for companies operating under TARP. Outside of financial services, however, compensation committees have sharpened their focus on performance, employing a variety of performance-based awards. Shareholders and the various shareholder advocacy groups support these approaches, encouraging the trend.

Pay Mix

In 2009, many companies reviewed the mix of pay they offered. Companies want to ensure there is an appropriate balance between short and long-term compensation as well as fixed vs. variable pay. Within financial services, many companies re-balanced the amounts executives received in salary, annual cash incentives and equity. This rebalancing is intended to align the time horizon of compensation with the risk profile of the company and will vary by industry.

Clawbacks

Clawback provisions for annual and long-term incentives are becoming more common across industries. This is another example of a practice required by TARP spilling over into general industry. Clawbacks come in a variety of flavors. Some require employees to forfeit or reimburse compensation for a period of time if an executive engages in conduct that results in a restatement of financial results. Other clawbacks are fashioned more broadly, allowing companies to recoup compensation if results deteriorate over time for any reason. Providing for clawbacks helps further align pay and performance and mitigates the potential risks of executives making short-term decisions that have a detrimental impact on the company over time. Some companies, especially in financial services, are increasing the use of deferred compensation to make it easier to recoup compensation later, if the need arises.

Stock Holding Requirements

The requirement to hold stock for a period of time following vesting or exercise of options has become increasingly prevalent over the last few years, although still not a majority practice. Companies with such requirements generally ask executives to hold 50% to 100% of net shares for a period of one to three years, or even to retirement or beyond for a minority of companies. Stock holding requirements continue to be a focus for companies as they are viewed as another practice to mitigate risk in compensation programs. Stock ownership guidelines, most often expressed as a multiple of base salary, are common for most companies. Some companies are re-evaluating their stock ownership guidelines and denominating the guideline in shares as opposed to a multiple of salary as a response to the volatility in the market.

Change in Control Protections

Pressure from shareholder advisory groups and activist investors are leading to reductions in change in control protections. As companies review their programs, many are committing to eliminate gross-ups on 280(g) excise taxes going forward. Some of these companies are grandfathering this provision for existing participants, while select companies are eliminating them completely for all participants. A few companies are asking executives with contractual rights to gross-ups to waive them. These companies recognize that gross-ups are a red flag in the current environment and acknowledge that the potential cost to the company, or acquiring company, far exceeds the benefit to the executive. As companies eliminate the gross-up feature, some provide the executive with the choice to receive the full amount of their change in control benefits and pay the excise tax themselves or reduce the benefits to a level just below the level which would trigger the excise tax payment.

In addition to eliminating gross-ups, more companies are moving to double-trigger vesting on equity following a change in control (i.e., executive must be terminated without cause or terminate for good reason following the change in control).

Summary

The magnitude of the economic crisis increased the level of scrutiny of executive compensation practices over the past two years to unprecedented levels. The actions we have seen companies take in 2009 have been greatly impacted by the environment. As companies release their proxy statements in the next few months, we will get a better sense of the final decisions, but we believe that both senior leaders within companies and compensation committees are supporting a new level of responsibility and accountability.

Please contact us at (212) 921-9350 if you have any questions about the issues discussed above or would like to discuss your own executive compensation issues. You can access our website at www.capartners.com for more information on executive compensation.

We view the report as required reading for outside directors, senior management and HR professionals. The report amounts to a call for action for boards of directors and compensation Committees to re-examine their compensation programs to ensure that the link between pay and performance is strong and the programs reflect best practices and high governance standards.

The report recommends that executive compensation programs reflect the five guiding principles:

- Principle One – Paying for the right things and paying for performance

“Compensation programs should be designed to drive a company’s business strategy and objectives and create shareholder value, consistent with an acceptable risk profile and through legal and ethical means. To that end, a significant portion of pay should be incentive compensation, with payouts demonstrably tied to performance and paid only when performance can be reasonably assessed.” - Principle Two – The “right” total compensation

“Total compensation should be attractive to executives, affordable for the company, proportional to the executive’s contribution, and fair to shareholders and employees, while providing payouts that are clearly aligned with actual performance.” - Principle Three – Avoid controversial pay practices

“Companies should avoid controversial pay practices, unless special justification is present.” - Principle Four – Credible board oversight of executive compensation

“Compensation committees have a critical role is restoring trust in the executive compensation setting process and should demonstate credi ble oversight of executive compensation. To effectively fulfill this role, compensation committees should be independent, experienced, and knowledgeable about the company’s business.” - Principle Five – Transparent communications and increased dialogue with shareholders

“Compensation programs should be transparent, understandable and effectively communicated to shareholders. When questions arise, boards and shareholders should have meaningful dialogue about executive compensation.”

In addition to the guiding principles, the report contains concrete recommendations on how to implement effective executive compensation programs. Click on the link http://www.conference-board.org/pdf_free/ExecCompensation2009.pdf to access the full report of Conference Board?s Task Force on Executive Compensation.

Please contact us at (212) 921-9350 if you have any questions about the issues discussed above or would like to discuss your own executive compensation issues. You can access our website at www.capartners.com for more information on executive compensation.

We found that 20 out of 25 companies (80%) retained the services of an executive compensation advisory firm in 2008. The large multi-service human resource consulting firms dominated, with either Towers Perrin, Mercer or Watson Wyatt providing services to 12 of the 20 companies (60%). The remaining eight companies (40%) retained smaller boutique firms that are unlikely to provide other services, including Pearl Meyer & Partners, Frederick W. Cook, Total Reward Strategies LLC, Compensation Strategies LL, ExeQuity and icca .

Two of the 20 companies (10%) reported changing advisors, but a trend toward the boutique firms was not apparent. Chevron replaced Hewitt, a multi-service firm, with ExeQuity, but Unitedhealth Group moved in the other direction, replacing Semler-Brossy, a boutique, with Towers Perrin, a multi-service firm.

Seventeen of the 20 companies (85%) indicated that their executive compensation advisory firm was independent. Three companies (15%) did not address this issue in their disclosures.

Nine of the 20 companies (45%) defined an independent compensation consultant as a firm that did not do any other work for the company. One company (5%) applied this standard to the individual adviser, rather than the firm, noting that the individual consultant did no other work for the company. Seven of the 20 companies (35%) maintained that their compensation consultant was independent, while allowing the consulting firm to provide other services. Several noted that the extent of these services were modest or immaterial. In some cases, the Compensation Committee required advance approval of other services. In other cases, Committee approval was not required specifically.

Several companies added their own unique provisions to their definition of independence. Some examples include:

- Requiring that the consulting firm annually attest to compliance with the stipulation to do no other work;

- Rotating the consultant after five years, and prohibiting the Company from hiring any consulting firm staff involved with the account for one year;

- Requiring that the individual consultant not be involved in other work, prohibiting sharing of information on compensation with other staff of the consulting firm, and requiring that the consultant’s compensation not depend on cross-selling other services;

- Limiting payments to affiliates of the consulting firm to two percent of aggregate gross revenues of the consulting firm and its affiliates;

- Prohibiting the consulting firm from providing services directly to senior officers of the Company.

Two companies embraced the concept of enhanced disclosure. Home Depot disclosed fees paid to both its consulting firm and to an affiliate of its consulting firm that provides other services related to the retirement plan. Another company committed to disclose aggregate fees by category of service if it determined that its consultant was not independent. In this case, the consulting firm would not be deemed independent if it or its affiliates provide other services that exceed two percent of gross revenues; or if individuals serving the Compensation Committee provide other services not at direction and under supervision of the Committee. A third approach we have seen used outside of the Fortune 25 population is to publish the ratio of executive compensation consulting fees to fees for other services, with the consulting firm deemed independent provided fees for other services are less than compensation consulting fees.

In summary, the majority of companies are now defining independence strictly to prohibit the firm and the individual consultant from doing other work for the company. A minority of Compensation Committees allow their consultants to perform other work, but require Committee approval and/or a materiality threshold.

Assuming the SEC is ultimately called to develop standards for consultant independence, what approach will they take? If the SEC requires consulting firms to do no other work, the SEC will limit the ability of the large multi-service consulting firms to compete in the marketplace. On the other hand, if the SEC imposes less rigorous standards, it may be in the awkward position of espousing a set of standards that are less comprehensive than in place currently at the majority of large companies.

Please contact us at ((212) 921-9350 or [email protected]) if you have any questions about the independence issues discussed above or would like to discuss your own executive compensation issues.