Stronger Governance Practices

What We Found

In response to increased pressure from shareholders and proxy advisory firms, as well as recent Say on Pay legislation, companies continue to monitor their executive compensation programs. In the past, companies would re-evaluate their programs every 2-3 years. Given today’s intense scrutiny of executive compensation, we are seeing companies and compensation committees re-evaluate their programs annually. New governance standards include completing the annual risk assessment and implementing updated clawback policies. In addition, companies have removed excise tax-gross ups from change in control benefits and perquisites, continue to emphasize stock ownership guidelines and stock retention requirements, and have reduced supplemental retirement benefits.

Compensation Risk Disclosure

Clear and explicit disclosure of the compensation risk assessment process is becoming standard practice, especially after the recent economic downturn and passage of SEC rules on enhanced compensation disclosure. Of the 111 companies in our study, 105, or 95%, make some type of affirmative disclosure on risk assessment in the most recent proxy. Similar to 2009, none of the companies disclosed that their incentive programs create material adverse risks.

Most companies make their risk-related disclosure in the CD&A of the proxy statement, with the corporate governance section of the proxy statement ranking as the second most common place for this disclosure. The table below summarizes where risk disclosures were made:

| Section of the Proxy Statement with Compensation Risk Disclosure |

2010 | 2009 | ||

| % of Cos. | % of Cos. | |||

| No. of Cos. | n=105 | No. of Cos. | n=75 | |

| CD&A | 49 | 47% | 39 | 52% |

| Corporate Governance Section (Section 407) | 25 | 24% | 19 | 25% |

| CD&A and Corporate Governance Section (Section 407) | 14 | 13% | 7 | 9% |

| Separate Stand Alone Section | 11 | 10% | 8 | 11% |

| CD&A and Compensation Committee Report | 4 | 4% | 2 | 3% |

| Compensation Committee Report | 2 | 2% | n/a | n/a |

Responsibility for completing the risk assessment process varies by company. Of the companies disclosing a risk assessment, 35 companies (33%) had management and the compensation committee working together to conduct the assessment, while 17 companies (16%) reported that the compensation committee worked alone to conduct the assessment. One change we noted is that this year 95% of companies disclosed who conducted the risk assessment versus only 65% last year. The table below provides further detail on which groups were involved in the compensation risk review:

| Approach to Compensation Risk Reviews | 2010 | 2009 | ||

| % of Cos. | % of Cos. | |||

| No. of Cos. | n=105 | No. of Cos. | n=75 | |

| Management & Compensation Committee | 35 | 33% | 10 | 13% |

| Compensation Committee | 17 | 16% | 7 | 9% |

| Compensation Committee & Consultant | 15 | 14% | 9 | 12% |

| Management | 13 | 12% | 7 | 9% |

| Management, Compensation Committee & Consultant | 12 | 11% | 15 | 20% |

| Management & Consultant | 8 | 8% | 1 | 1% |

| Not Disclosed | 5 | 5% | 26 | 35% |

Clawbacks

Despite the SEC’s delay in proposing policies to recoup executive compensation under Dodd-Frank, companies have been proactively adopting clawback policies. Even though clawbacks are mandated by the SEC for all public company CEOs and CFOs under SOX and for the top 25 executives in TARP participants, companies have implemented their own clawbacks to obtain broader protection.

A significant majority of our research companies – 89 of 111 (80%) – maintain some form of clawback provision. For 2010, 17 of the 89 companies adopted a new clawback policy and 10 modified existing policies by expanding the type of compensation that can be recouped, the executives covered or the events that trigger a clawback. The majority of companies are awaiting final SEC regulations, however, before making comprehensive changes to update existing policies.

Similar to our findings in 2009, a financial restatement is required to trigger a clawback in nearly all cases (74 companies or 83% of those with a clawback). Further, 66 companies (74% of those with a clawback) disclosed that misconduct is a triggering event and 45 companies (51%) disclosed fraud as a trigger.

Based on our review of CD&A disclosures, companies with a clawback include the ability to clawback or recoup the following types of compensation: earned, exercised, outstanding, vested or unvested.

| Compensation Subject to Clawback | % of Cos. | |

| No. of Cos. | n=89 | |

| Prior annual incentive | 81 | 91% |

| Prior LTI | 79 | 89% |

| Future annual incentive | 20 | 22% |

| Future LTI | 14 | 16% |

Note: Percentages add up to greater than 100% due to multiple responses.

Of the type of compensation that is subject to a clawback, clawbacks of both cash and equity are equally prevalent.

While the majority of companies do not explicitly state who their clawback policy applies to, it is clear that coverage extends to the NEOs at 83 companies (93%).

A minority of companies (18 companies or 20%) indicate the time period which compensation can be recovered after a restatement. Of the 18 companies that disclosed a time frame, the most common is 1 year from the date of restatement and the range is 1-3 years.

It is apparent from reviewing CD&A disclosure that most companies are waiting for the SEC to rule before modifying their current policies. Companies will need to develop and implement a policy to provide for recovery of compensation that aligns final rules issued by the SEC. The proposed rules apply to both current and former executives and cover all incentive compensation within 3 years of a financial restatement (with or without intentional misconduct). It is unlikely that companies will make final modifications to their policies that apply to the 2012 proxy season, since the SEC is not expected to issue final rules until the first half of 2012.

Stock Ownership Requirement Changes

Companies continue to monitor their stock ownership requirements in order to align executives with shareholders. This year 25 companies (23%) initiated a change with respect to stock ownership or stock holding requirements. The most prevalent change was an increase in stock ownership guideline levels, with 12 of the 25 companies (48%) disclosing an increase. This is likely attributed to a recovery in the economy as well as stock prices, and increasing pressure from regulators and proxy advisory firms. Other common changes were 24% of companies added a new stock holding requirement and 20% modified or added a penalty for non-compliance. Further detail on changes made to executive stock ownership guidelines are below:

| Changes made to Executive Stock Ownership Guidelines | 2010 | 2009 | ||

| % of Cos. | % of Cos. | |||

| No. of Cos. | n=25 | No. of Cos. | n=17 | |

| Increased | 12 | 48% | 3 | 18% |

| Added holding requirement | 6 | 24% | n/a | n/a |

| Modified penalty for non-compliance | 5 | 20% | n/a | n/a |

| Changed to multiple of salary | 2 | 8% | n/a | n/a |

| Increased holding requirement | 2 | 8% | n/a | n/a |

| Decreased holding requirement | 2 | 8% | n/a | n/a |

| Newly adopted | 1 | 4% | 10 | 59% |

| Decreased | 1 | 4% | 1 | 6% |

| Adopted mandatory holding of shares through retirement | 1 | 4% | n/a | n/a |

Note: Percentages add up to greater than 100% due to multiple changes by several companies.

Stock Ownership Requirements Detail

For companies disclosing shares counted toward ownership requirements, it is interesting to note that one-third of companies count unvested restricted stock towards meeting the guidelines, since companies expect executives to vest in these shares. However, only 6% count vested/unexercised options and 5% count unearned performance shares since these shares are viewed as being subject to greater risk. See below for further detail:

| Shares Counting For Guideline Requirements | % of Cos. | |

| No. of Cos. | n=99 | |

| Shares directly owned | 55 | 56% |

| Unvested RS | 33 | 33% |

| Shares in 401(k) plan | 33 | 33% |

| Shares indirectly owned | 29 | 30% |

| Shares purchased on open market | 29 | 29% |

| Not disclosed | 29 | 29% |

| Deferred Compensation | 25 | 25% |

| Vested but unexercised options | 6 | 6% |

| Unearned performance shares | 5 | 5% |

| Unvested options | 1 | 1% |

Note: Percentages add up to greater than 100% due to multiple types of equity counted by various companies.

Among CEOs, most companies (82%) express their guidelines as a multiple of base salary and 17% of companies express their guidelines in fixed share amounts. The fixed share approach is more prevalent among financial services and technology companies.

The median guideline for all company CEOs in our study sample is a 5x multiple of base salary or a fixed share guideline of 150,000 shares. The median value of these guidelines is $6,700,000.

| CEO Stock Ownership Guidelines (n=99) |

Prevalence |

25th Percentile Level | Median Level | 75th Percentile Level |

| Multiple of Base | 82% | 5.0x | 5.0x | 6.0x |

| Fixed Share | 17% | 100,000 | 150,000 | 300,000 |

| Fixed Value | 1% | $5,000,000 | $5,000,000 | $5,000,000 |

| Total Value | – | $5,389,894 | $6,700,000 | $8,600,000 |

15% of companies disclose some type of penalty for non-compliance with stock ownership guidelines. The most common penalties disclosed include mandatory payment of a portion of the annual bonus in stock and requiring executives to hold shares after an option exercise or the vesting of stock awards.

Stock Holding Requirements Detail

Having stock holding or stock retention requirements in addition to stock ownership guidelines is a growing trend. In our sample of 111 companies, 30 companies (27%) disclose some type of stock holding requirement. Over half of the 30 companies have a stand-alone stock holding requirement. This type of requirement is most prevalent among financial services companies in place at 75% of financial services companies.

Most of these companies (46%) require executives to hold equity after vesting or exercise for 1 year. Holding shares until retirement (33%) is the second most prevalent holding period, although it is relatively rare. 70% of companies disclose that the equity to be held is the net after-tax shares retained by the executive after option exercise/equity vesting. See below for further detail:

| Definition of LTI subject to Hold | % of Cos. | |

| No. of Cos. | n=30 | |

| RS/RSUs | 25 | 83% |

| Options | 22 | 73% |

| Performance Shares | 12 | 40% |

| Net after tax shares | 21 | 70% |

Note: Percentages add up to

- Going forward, a Say on Pay vote will be an annual event at most companies

- A simple majority should not be considered a passing grade

- Companies with stronger performance generally received higher levels of shareholder support

- Say on Pay voting has already been a catalyst for change

As background, on January 25, 2011, the SEC issued final rules implementing Section 951 of the Dodd-Frank Wall Street Reform and Consumer Protection Act (“Dodd-Frank”), which generally provides shareholders of US public companies with the right to cast three types of advisory votes related to executive compensation:

- A vote to approve the compensation of the Named Executive Officers (NEOs), effective for shareholder meetings occurring on or after January 21, 2011;

- A vote on the frequency with which shareholders should be entitled to cast Say on Pay votes (every one, two or three years), effective for shareholder meetings occurring on or after January 21, 2011; and

- A vote on golden parachute arrangements for NEOs related to a sale, consolidation or merger, effective April 25, 2011.

Say on Pay Frequency Vote Results (2011 Proxy Season)

An annual vote frequency has emerged as the clear shareholder preference. Among 93% of S&P 500 companies reporting vote results, a majority of shareholders supported annual Say on Pay vote frequency. This differs from vote recommendations, where only 68% of the companies had recommended an annual vote.

Company Recommendation (n=455)

| Vote Frequency | # of Companies | % of Companies |

| Annual | 310 | 68% |

| Bienniel | 13 | 3% |

| Triennial | 111 | 24% |

| No Recommendation | 21 | 5% |

Vote Results: Received Majority Shareholder Support (n=438)

| Vote Frequency | # of Companies | % of Companies |

| Annual | 409 | 93% |

| Bienniel | 1 | 0% |

| Triennial | 21 | 5% |

| None (only plurality)1 | 7 | 2% |

The strong support for annual votes is not a surprise. 39 institutional investors, representing more than $830 billion in assets, issued a public call for companies and investors to support annual advisory votes on executive compensation in 2011 proxy statements. Similarly, a number of major mutual funds have also indicated support for annual Say on Pay votes, and ISS’ policy recommends that shareholders support annual votes (Glass Lewis has indicated a similar preference).2

CAP Comment: Following the frequency vote, the SEC rules mandate disclosure of how often the company will hold future Say on Pay votes, generally through an 8-K. Issuers must also provide proxy-based disclosure of the current frequency of Say on Pay votes and when the next scheduled Say on Pay vote will occur.

CAP Comment: When companies conduct their Say on Pay vote in line with the frequency preferred by a majority of shareholders, they may exclude shareholder frequency proposals from the proxy for six years.

Say on Pay Vote Results (2011 Proxy Season)

Say on Pay resolutions received majority shareholder support at all but eight S&P 500 companies, with average support of 89% (most companies received greater than 80% support for their NEO pay program).3

| %inFavor | #of Companies | %of Companies | Average1-Yr TSR @12/31/10 | A “threshold” for acceptable passage rates seems to have emerged; to-date, results indicate this threshold is around 80% shareholder support. |

| 90%-100% | 274 | 62% | 25.2% | |

| 80%-90% | 73 | 17% | 24.3% | |

| 70%-80% | 43 | 10% | 16.5% | |

| 50%-70% | 40 | 9% | 7.4% | |

| 0%-50% | 8 | 2% | 9.6% |

As shown above, companies with stronger TSR on a 1-year basis generally received a higher level of support from shareholders on their executive pay programs.

CAP Comment: While a company does not “fail” its Say on Pay vote unless a majority of shareholders vote against the compensation program, many companies have received 90+% shareholder support and an “acceptable” shareholder support threshold has emerged around 80%. Below this level of support, we have found that there often is a notable level of shareholder discontent that should be carefully reviewed.

CAP Comment: While these votes are non-binding, we expect that most companies will carefully evaluate their vote results, taking some action if there is low shareholder support (not just in the limited cases where a majority of shareholders did not support the company’s executive compensation program).

CAP Comment: The final SEC rules require additional disclosure in the CD&A regarding whether, and if so how, companies have considered the results of the most recent Say on Pay vote.

CAP Comment: As a result of the Dodd-Frank legislation, the SEC will eventually adopt rules requiring proxy-based disclosure of the pay-for-performance relationship at each U.S. public company (rules currently schedule to be adopted during 2012).

The eight companies where a majority of shareholders did not support the executive compensation program, and the Say on Pay vote results for these companies, are:

| Company | 1-Yr TSR | % Votes in Favor |

| Hewlett-Packard | -17.7% | 48.2% |

| Freeport-McMoran Copper & Gold | 52.6% | 45.5% |

| Jacobs Engineering | 21.9% | 44.8% |

| Masco Corp. | -6.1% | 44.6% |

| Nabors Industries | 7.2% | 42.5% |

| Janus Capital Group | -3.2% | 40.1% |

| Constellation Energy Group | -10.3% | 38.0% |

| Stanley Black and Decker | 32.7% | 38.0% |

Impact of Proxy Advisor Recommendations

On average, shareholder support for Say on Pay votes was considerably lower when ISS recommended an “Against” vote to shareholders.4,5

|

|

|||||||||||||||||||||

CAP Comment: Where ISS recommended an “Against” vote for Say on Pay, 90% of companies received less than the 80% percent shareholder support threshold discussed above.

As shown below, companies that received an “Against” vote recommendation from ISS generally had lower TSR.

| ISS Vote Recommendation | # Companies that Passed | # Companies that Failed | Total | Average 1-Yr TSR @ 12/31/10 |

| For | 377 | 0 | 377 | 24.3% |

| Against | 53 | 8 | 61 | 10.3% |

| Total | 430 | 8 | 438 | 22.5% |

CAP Comment: Of the 438 companies reporting vote results, to-date, ISS recommended an “Against” vote for Say on Pay at 61 S&P 500 companies (14%). Only 8 of the 61 companies (13%) did not receive majority support for their Named Executive Officer compensation program.

Responding to Proxy Advisor Recommendations

Some notable companies took additional steps related to executive compensation during this proxy season, filing supplementary soliciting materials and/or making last minute modifications to their CEO pay program. Select examples include: General Electric, Disney, ExxonMobil, Johnson & Johnson, Hewlett-Packard, Lockheed Martin, and Northern Trust. While these filings were generally in reaction to negative vote recommendations from shareholder advisory services such as ISS, ExxonMobil went a step further by filing supplementary materials (essentially an executive pay brochure) on the same day as the proxy. ExxonMobil still received a negative vote recommendation from ISS, and later filed additional soliciting material rebutting ISS’ vote recommendation.

Conclusion

During the 2011 proxy season, a clear shareholder preference for annual Say on Pay votes emerged. In terms of the actual Say on Pay vote, an 80% threshold emerged as an “acceptable” level of shareholder support, a significantly higher hurdle than simple a pass / fail test.

Say on Pay has already been a catalyst for change. Companies are more willing to address controversial pay practices than they were a year earlier. Disclosure of executive compensation in proxy statements has evolved, and the influence of proxy/shareholder advisory services (such as ISS) has increased.

Looking forward, companies will need to carefully evaluate their Say on Pay vote result from the 2011 proxy season, and determine how to best incorporate any findings into planning for 2012.

1 None of the three frequency options (annual, biennial, or triennial) received majority support (greater than 50%).

2 For additional detail, see 12/5/10 CAPFlash: “ISS 2011 Policy Updates – Here Comes Say on Pay.”

3 Outside of the S&P 500, an additional 29 companies did not receive majority shareholder support for their NEO compensation program.

4 ISS refers to Institutional Shareholder Services, an influential proxy advisory service. Source of vote recommendations was ISS Voting Analytics.

5 Sample = 434 companies that filed vote results to-date.

Notable 2010 Findings

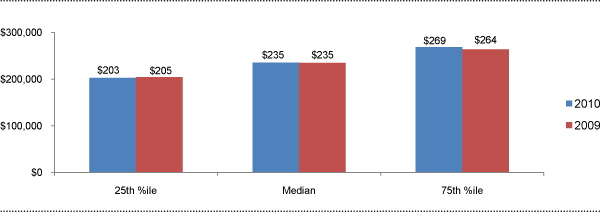

Total Board Compensation

At median, pay levels for non-employee directors were flat from 2009-10. Year-over-year, median Total Board Compensation remained steady at $235,000 i.

Total Board Compensation ($000s)

In line with emerging practices among large companies, use of Board meeting fees was minority practice in 2010, with only 23% of companies paying meeting fees.

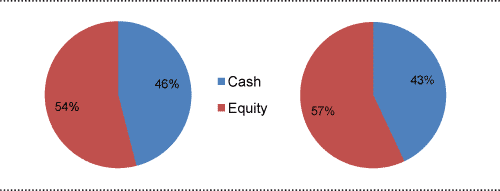

Pay Mix

On average, the cash vs. equity pay mix was generally consistent between 2009 and 2010. The majority of compensation delivered to non-employee directors continues to be in the form of equity.

2010 Pay Mix | 2009 Pay Mix

CAP Perspective:

Over the next few years, we expect the following trends in director compensation to take place: 1) low to mid single-digit annual increases in Total Board Compensation; 2) more companies moving to fixed cash pay structures; 3) a continued emphasis on full-value equity awards.

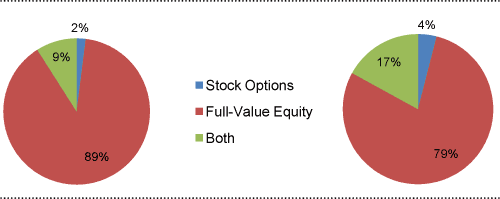

Equity Compensation

On average, an increased portion of 2010 equity-based compensation for non-employee directors was paid in the form on full-value awards, as compared to 2009.

2010 Equity Awards | 2009 Equity Awards

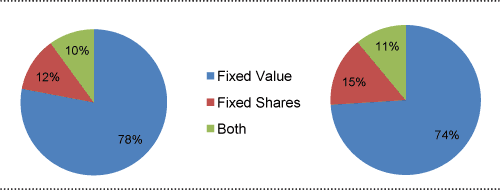

Year-over-year (2010 vs. 2009), equity awards denominated as a fixed value increased in prevalence, as opposed to those based on a fixed number of shares.

2010 Equity Awards | 2009 Equity Awards

Committee Compensation

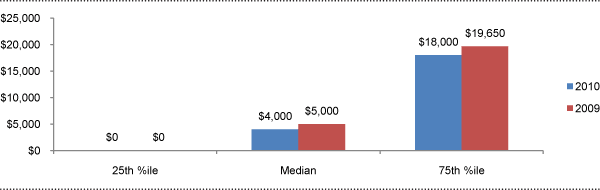

During 2010, median committee member compensation was generally consistent with 2009ii. Our research also found that approximately one-third of companies studied pay no committee-specific fees to members of any of the 3 major committeesiii.

Committee Member Compensation

CAP Perspective:

We expect the trend away from committee member fees to continue, with the value being rolled into board cash or equity retainers, as many companies now view all Board members as active participants in committee-level work.

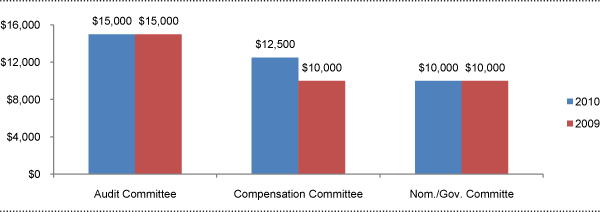

At median, additional compensation for committee Chairs remained flat for the Audit and Nominating / Governance committees, and rose by 25% for the Compensation Committee, driven by increased time requirements and scrutiny of executive compensation.

Median Additional Compensation for Committee Chairs

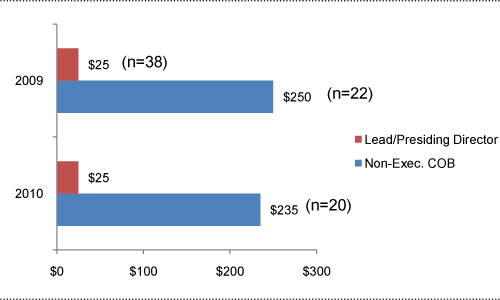

Lead/Presiding Directors and Non-Executive Chairs of the Board

During 2010, the prevalence of additional compensation for Lead/Presiding Directors and non-Executive Board Chairs remained flat as compared to 2009. While, at median, additional compensation for Lead/Presiding Directors remained flat, additional compensation for non-Executive Chairs decreased slightly.

Median Additional Compensation for Board Leadership Roles ($000s) (excl. 0s)

CAP Perspective:

While not all non-executive Board leaders receive additional pay for the role, prevalence of additional compensation for these roles is expected to increase over time. The differential in pay between Lead/Presiding directors and non-Executive Chairs is in line with the typically different responsibilities of each position.

Conclusion

As shown above, there was nominal change in director pay levels and practices year-over-year (2010 vs. 2009) among the largest public U.S. corporations.

It is important for companies to regularly evaluate their overall non-employee director compensation program, or risk falling behind the curve in regards to desired relative market positioning and best in class program design. While reviews should be conducted regularly, it is usually unnecessary for design or pay level changes to take place more often than every 2-3 years.

CAP will release its full report on non-employee director compensation during Fall 2011. The report will provide a detailed analysis of year-over-year changes in pay levels, pay practices and other program design considerations, as well as a discussion of best in class director compensation program setting process.

- i Compensation reflects all cash and equity compensation for Board and committee service, excluding compensation for additional leadership roles such as committee Chair, Lead/Presiding director, or non-executive Chair of the Board.

- ii Reflects all compensation for committee member service (excludes additional fees for leadership roles), across all Board committees.

- iii Audit, Compensation and Nominating / Governance committees.

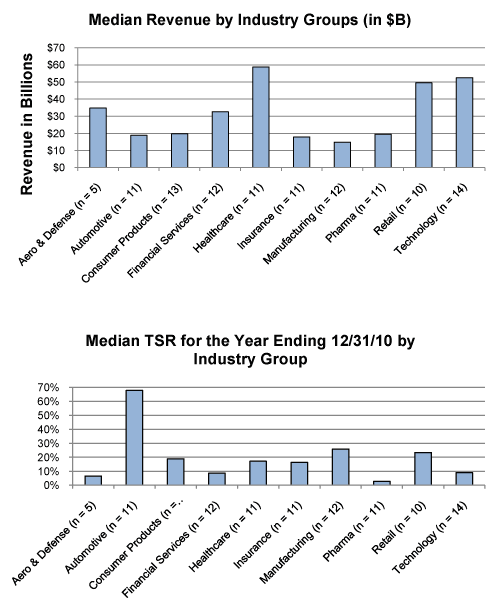

For the 111 company sample, median revenue was $27B, market capitalization was $30B and Total Shareholder Return (TSR) was 16% for 2010.

What We Found

Highlights of our research findings are below. Most companies did not make sweeping changes to their executive compensation programs. But many companies continued to refine annual and long-term incentive plans to strengthen the alignment between executive rewards and financial performance and to focus executives on the overall health of the organization.

Compensation Strategy Changes

Similar to 2009, most companies did not make significant changes to their compensation strategy. Financial Service firms were more likely to make changes to the strategy (e.g., increase at-risk pay) as they emerged from compensation restrictions imposed by TARP.

Peer Groups Used For Benchmarking

In 2010, companies continued to review and modify their peer group, although wholesale changes were not the norm. Approximately 40% of companies made some modification to their peer group by selecting peers that more closely aligned with their size and business mix. Pharmaceutical companies, in particular, continued to make changes to the peer group as industry consolidation continued.

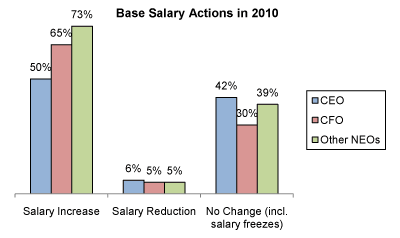

Base Salary Actions

2010 saw the return of salary increases for senior executives with a majority of companies providing salary increases to Named Executive Officers (NEOs) in 2010 (vs. 20% in 2009) as the economy improved. Within the NEO ranks, companies provided increases more frequently to executives below the CEO as they focused on retaining top talent and remaining competitive with the market. Salary reductions were most prevalent in companies that emerged from TARP, as these companies reverted to a compensation mix that provides a greater emphasis on incentive-based pay. Fewer companies froze base salaries for NEOs in 2010; companies in the Consumer Goods, Retail and Technology industry groups were more likely to maintain salaries at 2009 levels.

Annual Incentive Plan Design

Approximately 50% of companies disclosed a change in 2010 or planned changes for 2011 to their annual incentive plan design. Companies continued to refine the metrics and weightings that determine plan funding and payout as pay for performance remains a major focus for companies. 26% of companies increased the target annual incentive opportunity for at least one NEO illustrating that companies are focusing on the competitive market given the improvements in the economy. Although changes to annual incentive plans vary by company, there continues to be an attempt to reward executives based on appropriate indicators of company success.

The chart below presents the reported AIP changes:

| % of Cos. Reporting Changes | |||

| Type of Change Reported in CD&A | No. of Cos. | 2010 (n = 57) | 2009 (n = 34) |

| Change in performance metrics used to fund awards | 19 | 33% | 44% |

| Change in performance metric weighting mix* | 10 | 18% | n/a |

| Increased target award opportunities | 15 | 26% | 26% |

| Adopted / amended annual incentive plan | 13 | 23% | 6% |

| Modified performance scale | 6 | 11% | n/a |

| Reduced maximum award payout leverage | 2 | 4% | 12% |

| Other changes | 9 | 16% | 9% |

Note: Percentages do not add up to 100% due to multiple responses.

* Not captured separately in 2009 and is included in preceding category.

Change in Performance Metrics

Of the 19 companies that made changes to performance metrics, most (10 companies) added metrics to the plan design. Additionally, 10 companies changed the weighting of the AIP metrics. In general, these changes were focused on basic company performance indicators such as profitability and cash flow. For example,

- Computer Sciences: Added free cash flow as a measure to emphasize the importance of liquidity and profitability

- Morgan Stanley: Added capital adequacy and credit rating measures to the metrics used to determine financial achievements

- Visteon: Added product quality and free cash flow as performance metrics

Many companies added cash flow as an annual incentive metric in 2010 indicating that in the wake of the recent economic downturn, companies are balancing profitability with liquidity.

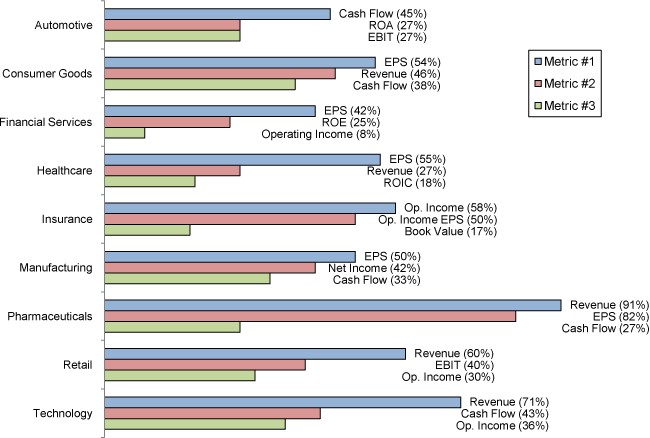

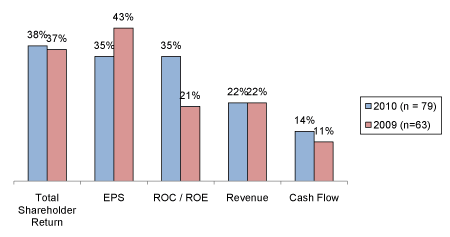

Annual Incentive Plan Metrics

In 2010, the most common metrics used across all industry groups were revenue or revenue growth, EPS and cash flow. Cash flow was one of the three most common metrics in five industry groups (Automotive, Consumer Goods, Manufacturing, Pharmaceuticals and Technology). More than other industries, annual incentive metrics for insurance companies tend to focus on industry-specific measures. The most prevalent metrics in the Automotive industry are cash flow and return on assets (ROA) denoting a focus on company operating performance during the economic recovery.

The three most prevalent metrics for each industry group are detailed below:

Note: Excludes Aerospace and Defense due to limited sample size (n = 5).

2010 Bonus Payout Details

Nearly all companies (95%) paid a bonus to an NEO for 2010. Most companies (90%) used financial performance to calculate the payout, although many of these companies (19%) also used discretion (positive and negative) to account for non-financial performance. Actual bonus payouts for CEOs on average were approximately 135% of the target incentive opportunity for 2010, indicating a rebound in financial performance in 2010 over 2009.

Long-Term Incentive Plan Design

A majority of companies (approximately 70%) reported making changes to their long-term incentive plan designs in 2010 or for 2011. Similar to the annual incentive plan changes, many companies (32%) reported changes to the performance metrics used to determine award payouts. 26% of companies reported changes to the LTI vehicle mix, with companies placing more emphasis on performance-based awards. This suggests that companies are focusing executives on longer-term goals. The table below outlines the reported changes:

| % of Cos. Reporting Changes | |||

| Type of Change Reported in CD&A | No. of Cos. | 2010 (n = 77) | 2009 (n = 60) |

| Changed long-term performance metric | 24 | 31% | 38% |

| Adopted / amended long-term incentive plan | 24 | 31% | n/a |

| Changed mix of LTI award vehicles | 20 | 26% | 55% |

| Added or eliminated LTI vehicle* | 22 | 29% | n/a |

| Changed LTI award opportunity level | 14 | 18% | 20% |

| Changed performance metrics/weighting | 6 | 8% | n/a |

| Other | 17 | 22% | 35% |

Note: Percentages do not add up to 100% due to multiple responses.

* Not captured separately in 2009 and is included in preceding category.

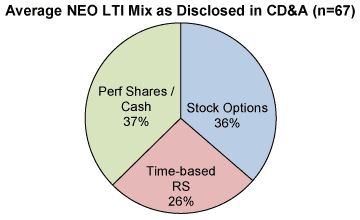

Long-Term Award Mix

From companies making changes to their LTI award mix, a majority (60%) disclosed that they increased the emphasis on performance by shifting a portion of total LTI value from time-based awards (options and restricted stock) to performance-based vehicles. On average, companies are providing approximately 25% of the total LTI awarded to NEOs in time-based restricted stock with the remaining value equally split between performance-based LTI and stock options.

| % of Cos. Reporting Changes | |||

| Type of Change Reported in CD&A | No. of Cos. | 2010 (n = 20) | 2009 (n = 33) |

| Greater emphasis on performance-based awards | 12 | 60% | 55% |

| Reduced emphasis on time-based restricted stock | 7 | 35% | n/a |

| Reduced emphasis on stock options | 5 | 25% | n/a |

| Other | 5 | 25% | 45% |

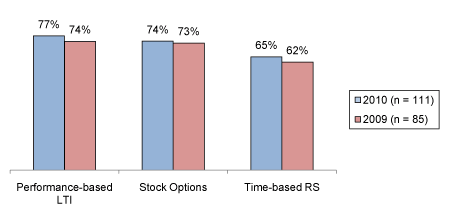

Long-Term Incentive Prevalence

Although companies making a change indicated they are placing a greater emphasis on performance-based awards, equity awards with time-based vesting continue to be prevalent. The prevalence of stock options and restricted stock with time-based vesting remained relatively flat in 2010, with 74% and 65% of companies using these vehicles, respectively.

Below is the breakdown of overall LTI vehicle prevalence for NEOs in 2010 vs. 2009:

Note: Percentages do not add up to 100% due to multiple responses.

Companies typically grant multiple LTI vehicles to NEOs to offer a balanced program with different performance metrics and time horizons. Most companies (77%) grant two or three award vehicles to provide LTI to executives.

Performance-Based LTI Metrics

For companies using performance-based LTI, TSR (38%) and EPS (35%) continue to be the most prevalent metrics. More companies are incorporating return on capital or return on equity as a metric in 2010 to increase the focus on longer term health/stability and the quality of earnings. The use of revenue and cash flow remained relatively flat year over year.

The chart below displays the prevalence of LTI metrics for performance-based awards in 2010 and 2009:

Note: Percentages do not add up to 100% due to multiple responses.

Treatment of Dividend Equivalents

Approximately 40% of companies that grant restricted stock (either time-based or performance-based) and 20% of companies that grant performance shares / units disclose that they pay dividend equivalents to executive officers. Companies typically pay dividends when the shares have vested or are earned.

Conclusions

2010 saw changes to annual and long-term incentive plan design in response to the rebounding economy, greater shareholder scrutiny, as a result of say on pay, and an attempt to further align pay and performance. With the economy on the rebound companies provided more frequent salary increases to NEOs in 2010 and were less likely to freeze base salaries. Companies modified incentive plan metrics, focusing on both company profitability and cash flow. The executive LTI mix continues to shift, with companies reporting more emphasis on performance-based awards. We expect to see companies continue to refine pay programs overall with the objective of strengthening pay and performance linkages and transparency.

Say on Pay Update

On January 25, 2011, the SEC issued final rules implementing Section 951 of the Dodd-Frank Wall Street Reform and Consumer Protection Act (“Dodd-Frank”), which generally provides shareholders of US public companies with the right to cast three types of advisory votes related to executive compensation:

- A vote to approve the compensation of the Named Executive Officers (NEOs), effective for shareholder meetings occurring on or after January 21, 2011;

- A vote on the frequency with which shareholders should be entitled to cast Say on Pay votes (every one, two or three years), effective for shareholder meetings occurring on or after January 21, 2011; and

- A vote on golden parachute arrangements for NEOs related to a sale, consolidation or merger, effective April 25th, 2011.

To date, 419 of the S&P 500 companies included Say on Pay resolutions in either a preliminary or definitive proxy statement. Vote results from annual meetings are available for 290 of these companies.

CAP Comment: While these votes are non-binding, we expect that most companies will carefully evaluate their vote results, taking some action if there is low shareholder support (not just in the limited cases where a majority of shareholders did not support the company’s executive compensation program).

Say on Pay Frequency Vote Results

An annual vote frequency is emerging as the clear shareholder preference. Among 94% of S&P 500 companies reporting vote results, a majority of shareholders supported annual Say on Pay vote frequency. This differs from vote recommendations, where only 67% of the companies had recommended an annual vote.

| Company Recommendation (n=419) | ||

| Vote Frequency | # of Companies | % of Companies |

| Annual | 281 | 67% |

| Biennial | 13 | 3% |

| Triennial | 108 | 26% |

| No Recommendation | 17 | 4% |

| Vote Results: Received Majority Shareholder Support (n=290) | ||

| Vote Frequency | # of Companies | % of Companies |

| Annual | 272 | 94% |

| Biennial | 1 | 0% |

| Triennial | 12 | 4% |

| None (only plurality)* | 5 | 2% |

The strong support for annual votes is not a surprise. 39 institutional investors, representing more than $830 billion in assets, issued a public call for companies and investors to support annual advisory votes on executive compensation in 2011 proxy statements. Similarly, a number of major mutual funds have also indicated support for the annual Say on Pay votes, and ISS’ policy recommends that shareholders support annual votes (Glass Lewis has indicated a similar preference)[1].

CAP Comment: As the 2011 proxy season continues, we expect the prevalence of annual vote frequency recommendations to increase.

CAP Comment: Following the frequency vote, the SEC rules mandate disclosure through an 8-K of how often the company will hold future Say on Pay votes[2]. Issuers must also provide proxy-based disclosure of the current frequency of Say on Pay votes and when the next scheduled Say on Pay vote will occur.

CAP Comment: When companies conduct their Say on Pay vote in line with the frequency preferred by a majority of shareholders, they may exclude shareholder frequency proposals from the proxy for six years.

Say on Pay Vote Results

Say on Pay resolutions received majority shareholder support at all but five S&P 500 companies, with support ranging from 55% to 100%[3]. The five companies where a majority of shareholders did not support the executive compensation program were Hewlett-Packard, Jacobs Engineering, Janus Capital Group, Masco Corp. and Stanley Black & Decker.

| % in Favor | # of Companies | % of Companies |

| 90% – 100% | 192 | 66% |

| 80% – 90% | 43 | 15% |

| 70% – 80% | 26 | 9% |

| 50% – 70% | 24 | 8% |

| 0% – 50% | 5 | 2% |

CAP Comment: While a company does not “fail” its Say on Pay vote unless a majority of shareholders vote against the compensation program, an “acceptable” shareholder support threshold is likely to emerge. To-date, results indicate this threshold will be around 80% shareholder support.

CAP Comment: The final SEC rules require additional disclosure in the CD&A regarding whether, and if so how, companies have considered the results of the most recent Say on Pay vote.

Some notable companies have been proactive during this proxy season, filing supplementary soliciting materials. Select examples include: General Electric, Disney, ExxonMobil, Johnson & Johnson, Hewlett-Packard, and Northern Trust. While these filings were generally in reaction to negative vote recommendations from shareholder advisory services such as ISS, ExxonMobil went a step further by filing supplementary materials (essentially an executive pay brochure) on the same day as the proxy. ExxonMobil still received a negative vote recommendation from ISS, and later filed additional soliciting material rebutting ISS’ vote recommendation.

New Fidelity Compensation-Related Voting Guidelines

Fidelity recently released revised proxy voting guidelines that are effective immediately[4]. Our discussion below focuses on guidelines for Say on Pay proposals and new share requests[5].

Say on Pay Proposals

Fidelity will generally vote for proposals to approve executive compensation unless such compensation is misaligned with shareholder interests or otherwise problematic[6]. In determining any misalignment, Fidelity will take into account, among other factors, whether:

- A company has an independent Compensation Committee

- The Compensation Committee engaged independent compensation consultants

- The Compensation Committee waived equity vesting restrictions

- The company adopted or extended a golden parachute without shareholder approval[7]

Fidelity will also:

- Support annual advisory votes on executive compensation

- Generally vote against proposals to support golden parachutesix

Equity Plan Votes – New Share Requests

The guideline for determining votes related to new share requests is now based on a company’s three-year average burn rate, instead of the dilutive effect of the proposed plan (the basis for the previous guideline)[8]. The guidelines state that Fidelity will generally vote against approval of additional shares if a company’s three-year average burn rate exceeds certain caps.

| Companies | 3-Yr. Avg. Burn Rate |

| Large Capitalization (A company included in the Russell 1000 Index) |

1.5% |

| Small Capitalization (A company not included in the Russell 1000 Index that is not a Micro-Capitalization Company) |

2.5% |

| Micro Capitalization (A company with market capitalization below US $300 million) |

3.5% |

CAP Comment: Similar to the prior dilution caps, if a burn rate exceeds the caps Fidelity will consider circumstances specific to the company or plans that lead it to conclude the burn rate is acceptable; details on mitigating factors not yet available.

CAP Comment: While Fidelity will be reviewing historic burn rate, it is not clear if they will consider prospective burn rate in terms of how many years the shares are expected to last. A duration of greater than five years is considered problematic by ISS. Glass Lewis has a similar policy, but uses a three-to-four year threshold.

CAP Comment: The guidelines do not make allowances for companies in industry groups that have historically had higher burn rates, such as technology. In contrast, ISS does vary burn rate caps by industry.

CAP Comment: Unlike ISS, Fidelity will not use a multiplier for full-value awards in its burn rate calculation. Since the calculation does not differentiate stock option awards and full-value stock awards, it could encourage greater use of full-value stock awards and less use of stock options.

Additional equity plan voting guidelines include:

- Vote against equity plans where:

- Stock option exercise price is less than fair value on the grant date, unless the discount is 15% or less and is expressly granted in lieu of salary or cash bonus

- The plan’s terms allow repricing of underwater stock options

- The Board or Compensation Committee has repriced outstanding options in the past two years without shareholder approval

- Vote against equity plans that include an evergreen provision[9]

- Vote against equity plans that provide for acceleration of equity award vesting without an actual change-in-control occurring

- Require a restriction period of no less than three years for time-based share awards and a performance period of no less than one year for performance-based awards[10]

Conclusion

A clear shareholder preference for an annual Say on Pay vote frequency has emerged. In terms of the actual Say on Pay vote, it will be interesting to see what level of shareholder support becomes viewed as “acceptable,” likely a higher hurdle than simply a pass / fail test. Based on current results, the acceptable “threshold” will be near 80% support, but that may change as the proxy season continues. Differences among industries may also emerge.

Where Fidelity’s support is desired for Say on Pay votes or new share requests, it will be important to take their policies into account when: making compensation-related decisions, putting together the Compensation Discussion and Analysis, and preparing shareholder proposals (Say on Pay, new long-term incentive plans and/or share requests, etc.).

Please contact us at (212) 921-9350 if you have any questions about the issues discussed above or would like to discuss your own executive compensation issues. You can access our website at www.capartners.com for more information on executive compensation.

[1] For additional detail, see 12/5/10 CAPFlash: “ISS 2011 Policy Updates – Here Comes Say on Pay.”

[2] Required no later than 150 calendar days after the date of the annual meeting in which the vote took place, but in any event no later than 60 calendar days prior to the deadline for submission of Rule 14a-8 shareholder proposals for the subsequent annual meeting.

[3] Outside of the S&P 500, an additional 18 companies did not receive majority shareholder support for their NEO compensation program (as of 5/20/11): Ameron International, Beazer Homes, Cincinnati Bell, Cogent Communications, Curtiss-Wright, Dex One Corporation, Helix Energy Solutions, Hercules Offshore, Intersil Corp., M.D.C. Holdings, Navigant Consulting, NutriSystem, NVR, Inc., Penn Virginia Corporation, PICO Holdings, Shuffle Master, Stewart Information Services Corporation and Umpqua Holdings Corporation.

[4] Available at: http://personal.fidelity.com/myfidelity/InsideFidelity/InvestExpertise/governance.shtml.tvsr.

[5] The guidelines also cover additional compensation-related topics, such as: bonus plan proposals (162m), equity exchanges/repricings, and employee stock purchase plans.

[6] Fidelity funds sub-advised by Geode Capital Management LLC, which discloses its own set of proxy voting guidelines, will generally vote for proposals to approve executive compensation unless it believes the company has engaged in poor compensation practices (similar to Fidelity’s general guidelines) or provided poor compensation disclosure (different from Fidelity’s general guidelines).

[7] Fidelity defines a “golden parachute” as: “employment contracts, agreements, or policies that include an excise tax gross-up provision; single trigger for cash incentives; or may result in a lump sum payment of cash and acceleration of equity that may total more than three times annual compensation (salary and bonus) in the event of a termination following a change-in-control.”

[8]Fidelity funds sub-advised by Geode Capital Management LLC, which discloses its own set of proxy voting guidelines, will continue to focus on the dilutive effect of the plan; dilution may not be greater than 10% (15% for companies with a smaller market capitalization). If the plan fails this test, the dilution effect may be evaluated relative to any unusual factor involving the company.

[9] A feature which provides for an automatic increase in the shares available for grant under an equity plan on a regular basis.

[10] Shorter periods are permitted for up to 5% of a plan’s shares for Large-Capitalization companies (10% for Small- or Micro-Capitalization companies).

To determine if this trend is continuing, Compensation Advisory Partners conducted a study to determine how CFO pay has changed over the last three years and how the year-over-year trends in compensation compare to trends in CEO pay. The study analyzes executive pay data disclosed by early proxy filers and includes 55 US public companies with revenues ranging from $1 billion to $150 billion, with median revenues of $10 billion. Only companies with the same incumbent CEO and CFO from 2008 to 2010 were included in order to focus on year-over-year changes for an individual. Financial services firms were excluded from the study as this industry, in particular, saw the emergence of several atypical compensation arrangements and special awards that were both temporary and unique to the financial services industry.

Our findings, summarized below, indicate that CFO pay is generally moving at the same rate as CEO pay. Salaries are increasing at a slightly faster rate for CFOs but incentive compensation, both annual and long-term, is moving at the same rate for CFOs and CEOs, illustrating that incentive levels are tied to company results. For 2010, incentives are up for both CFOs and CEOs, reflective of a slowly rebounding economy.

Study Results

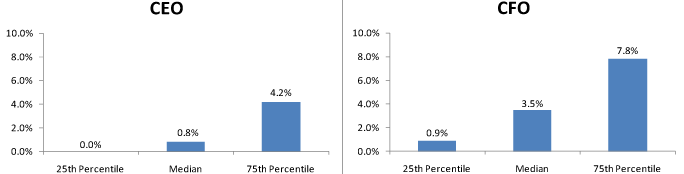

Salaries

In 2010, 78% of CFOs received salary increases at a rate of 3.5% at median and 7.8% at the 75th percentile. In comparison, only 55% of CEOs received salary increases at lower levels (0.8% at median and 4.2% at the 75th percentile). The prevalence of no salary increases also rose among CEOs from 40% in the 2008-2009 period to 46% in the 2009-2010 period while for CFOs, the prevalence of no salary increases decreased to 22% in the 2009-2010 period versus 31% in the 2008-2009 period.

Salary Increase Prevalence

| 2008-2009 | 2009-2010 | |||

| No Increase | Increase | No Increase | Increase | |

| CEO | 40.0% | 60.0% | 45.5% | 54.5% |

| CFO | 30.9% | 69.1% | 21.8% | 78.2% |

2010 Salary Increases

Actual Pay Levels

Overall, actual total direct compensation (salary plus actual annual incentive plus the present value of long-term incentives) for both CFOs and CEOs slightly declined in 2009 and subsequently rebounded in 2010, as illustrated by the chart below. CFO pay fell at a slightly higher rate in 2009 and increased at a higher rate in 2010 compared to CEO pay. The rise in 2010 pay levels was primarily due to increases in incentive (performance-based) compensation. Bonuses increased by approximately 16% and LTI increased by 14% – 19%. These increases in incentive compensation are most likely reflective of the recovering economy, improvements in company financial performance and rebounding stock prices.

Median Percentage Change in Pay Components

| 2008-2009 | 2009-2010 | |||

| CEO | CFO | CEO | CFO | |

| Salary | 0.7% | 2.0% | 0.8% | 3.5% |

| Actual Bonus | -3.1% | 3.5% | 16.3% | 15.6% |

| Long-Term Incentives | -2.4% | -5.7% | 13.7% | 18.6% |

| Actual Total Direct Comp. | -4.7% | -5.2% | 18.3% | 23.3% |

Financial Performance (Median Levels)

| Year | Total Shareholder Return (as of 12/31) | 1-Year Revenue Growth | 1-Year Revenue Growth |

| 2008 | -32% | 8% | 2% |

| 2009 | 26% | -8% | -6% |

| 2010 | 21% | 9% | 19% |

While movement in pay among CFOs and CEOs was directionally similar, on average, CFO actual total direct compensation was generally 30 – 35% of CEO actual total direct compensation over the last three years.

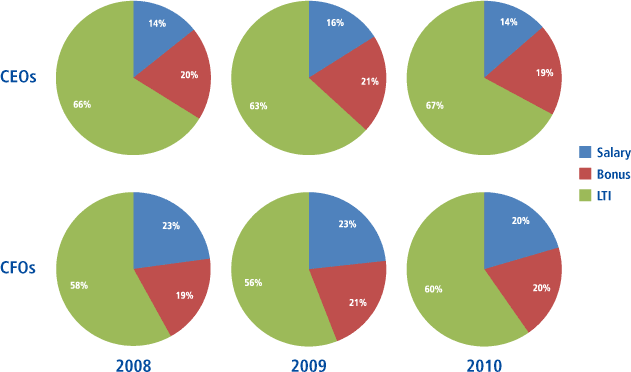

Target Pay Mix

When considering compensation at target levels, the pay mix remained largely unchanged from 2008 to 2010, with a greater emphasis on at-risk pay for CEOs than for CFOs. The pay mix for CFOs slightly shifted towards incentive-based compensation (from 77% in 2008 to 80% in 2010) showing that the pay mix for CFOs is moving closer to that of CEOs.

Long-Term Incentive (LTI) Vehicle Prevalence

The majority of companies awarded LTI to both CEOs and CFOs using at least two vehicles. The prevalence of stock options in the LTI mix declined over the 3-year period while the prevalence of performance-based awards increased. Overall, 83% of CFOs and 85% of CEOs received some form of performance-based awards as part of their LTI program in 2010.

Number of LTI Vehicles Used in 2010

| % in Total | ||

| CEO | CFO | |

| 1 | 13% | 15% |

| 2 | 61% | 54% |

| 3 | 26% | 31% |

| Average | 2 | 2 |

Long-term Incentive Mix

The majority of LTI continues to be delivered in the form of stock options and performance-based LTI, with less emphasis on restricted stock.

LTI Mix

| 2008 | 2009 | 2010 | ||||

| CEO | CFO | CEO | CFO | CEO | CFO | |

| Stock Options | 44% | 41% | 39% | 39% | 34% | 31% |

| Time Vested Restricted Stock | 16% | 22% | 17% | 20% | 17% | 20% |

| Perf. Based LTI | 40% | 37% | 43% | 41% | 49% | 48% |

Conclusion

In the last two years, trends in CFO pay have been directionally aligned with trends in CEO pay. The target pay mix for CFOs has slightly increased the emphasis on incentive compensation relative to fixed compensation, moving closer to the pay mix of CEOs. Salaries are increasing at a faster rate for CFOs but incentive compensation is increasing at about the same pace for both CFOs and CEOs, indicating a link to company performance results, and emphasizing that the role of the CFO continues to be important. We expect companies to continue to ensure that they have the right skill set in the CFO role and develop compensation programs that attract and motivate key talent.

Please contact us at (212) 921-9350 if you have any questions about the issues discussed above or would like to discuss your own executive compensation issues. You can access our website at www.capartners.com for more information on executive compensation.

The proposed rules are generally consistent with expectations and reflect a straight-forward application of Dodd-Frank. Much of the implementation of this aspect of Dodd-Frank will actually be accomplished through the listing standards adopted by the national securities exchanges, subject to approval by the SEC. For the most part, where there was ambiguity in how to interpret Dodd-Frank’s language, the SEC has passed the responsibility for interpretation on to the national securities exchanges or has let the Dodd-Frank language stand, but solicited comments on whether further clarification is necessary.

The SEC is soliciting comments on a number of aspects of the proposed rules, with a deadline for any comments of April 29, 2011. Below is a summary of the key provisions of the proposed rules based on a review of the full text and accompanying press release. We also provide our own comments on some of the key areas where the SEC is seeking input.

Listing Standards and Compensation Committee Independence

One of the objectives of Dodd-Frank was to ensure the independence of the Compensation Committee. To promote this objective, Dodd-Frank requires that national securities exchanges adopt listing standards to address the following issues:

- Require that Compensation Committee members be independent. Factors that need to be considered in assessing independence include:

- Sources of compensation of a director, including any consulting, advisory or compensatory fee paid by the company to such member of the board of directors

- Whether a member of the board of directors of a company is affiliated with the company, a subsidiary of the company, or an affiliate of a subsidiary of the company

- CAP Comment: The SEC is seeking comments on aspects of this rule including whether they should require minimum independence standards for all exchanges beyond consideration of the two factors above and whether the standards should be based on current relationships only or have a “look back” period. It will be interesting to see if the listing standards converge to a consistent standard or if slight differences remain

- Authority and Funding of the Compensation Committee – Listing standards need to indicate that the Compensation Committee has the authority to obtain a compensation adviser, is directly responsible for the adviser and must be appropriately funded to pay for the adviser

- CAP Comment: This aspect of the rule is more straightforward, but the SEC is seeking comments on technical aspects related to use of legal advisers including the definition of an “independent legal counsel” and the potential need for clarification around the use of in-house legal counsel or the company’s outside counsel. In addition, they are seeking comments on what the typical administrative expenses for Compensation Committees are and whether a provision requiring funding of such expenses would be helpful

- Compensation Adviser Selection: Listing standards must state that the Compensation Committee may select a compensation consultant, legal counsel or other adviser only after considering the following five factors:

- Other services provided to the company by the adviser

- Compensation adviser fees from company as a % of total fees

- Compensation consulting firm’s conflict of interest policies and procedures

- Business or personal relationships between compensation adviser and members of the Compensation Committee

- Compensation adviser’s ownership of company stock

- CAP Comment: In the proposed rules, the SEC did not choose to expand the number of factors to be considered beyond the original five specified in Dodd-Frank. The SEC is soliciting comment on the competitive neutrality of the five factors, potential additions to the factors to consider, and multiple issues for potential clarification (e.g., does adviser refer to the firm or individual providing services?, should there be specific tests/thresholds applied to the five factors?)

- Exemptions: The proposed rules require the exchanges to exempt the following five categories of companies from the Compensation Committee independence requirements:

- Controlled companies

- Limited partnerships

- Companies in bankruptcy proceedings

- Open-end management investment companies

- Foreign private issuers that disclose in annual report why they do not have an independent Compensation Committee

- Note: The proposed rules would authorize exchanges to exempt certain types of relationships or classes of companies from the independence requirements, subject to SEC approval

- CAP Comment: The SEC is soliciting comments on whether certain types of companies (e.g., smaller reporting companies, recent IPOs) should be exempt from the rules or provided with additional time to comply

Compensation Conflicts of Interest Disclosure

The proposed rules will build on the existing disclosure requirements but also require additional disclosure about whether:

- The Compensation Committee has retained or obtained the advice of a Compensation Consultant

- The work of the compensation consultant has raised any conflict of interest, and, if so, the nature of the conflict and how the conflict is being addressed

- The proposed rules would eliminate the current disclosure exception for services that are limited to consulting on broad-based plans and the provision of non-customized benchmark data, but retain the current fee disclosure requirements, including the exemptions from those requirements

- CAP Comment: The SEC is soliciting comments on key aspects of this issue, including whether or not they should attempt to clarify what a “conflict of interest” that must be disclosed is. Another area where they are seeking input is on whether any information related to the five factors under consideration needs to be disclosed

Conclusion

For most of these rules, the impact will be through the new listing standards for the national securities exchanges rather than directly through the SEC’s regulations. For larger companies, Compensation Committee member independence will likely be a non-issue as most already have Compensation Committees made up of all independent directors and it is unlikely that the new listing standards will make the independence requirements significantly more stringent.

On adviser independence, we expect that the outcome will be that companies will likely operate within the general guidance provided by the five factors. Companies will need to develop a process to conduct a review of the five factors and come to their own conclusions about whether or not there is a conflict of interest. Companies may choose to say they evaluated the principles and determined the adviser to be independent. Other may go into more elaborate detail about the process and determination similar to the way companies have addressed the disclosure of risk assessment in compensation.