Short-term cash incentives continue to be popular motivational tools at U.S. privately owned companies, nonprofits and government organizations (NGOs), according to recent research conducted by Vivient Consulting and WorldatWork. The 2017 executive and employee compensation research spotlights short- and long-term incentive pay practices and is unique in its focus on entities that are not publicly traded.

Vivient and WorldatWork surveyed WorldatWork members in late 2017 and published the results in May 2018 in two reports:

- “Incentive Pay Practices: Privately Held Companies”

- “Incentive Pay Practices: Nonprofit/Government Organizations.”

This 2017 compensation survey provides a long-term view of typical incentive pay practices at private companies and NGOs as well as a snapshot of current and emerging pay practices and compensation trends.

Typical Incentive Pay Practices

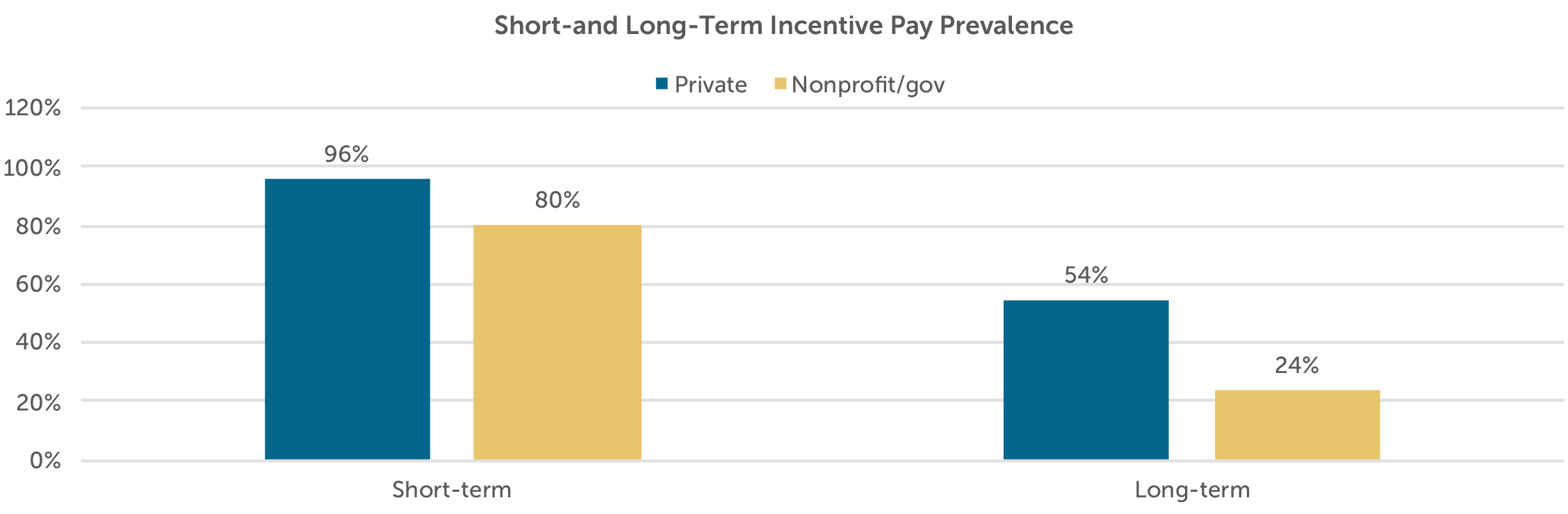

What do typical incentive pay practices look like at non-publicly traded entities? Nearly all private, for-profit companies provide some form of short-term incentive (STI), with annual incentive plans (AIPs) being the most common type. Other STIs include:

- Discretionary bonuses

- Spot awards

- Team/small-group incentives

- Project bonuses

- Profit sharing.

The survey excludes sales and commission plans. Although not as prevalent as at for-profit counterparts, some form of short-term incentive compensation is used by 80% of the NGOs represented in the survey. And short term incentives at nonprofit organizations have increased in the decade that the survey has been conducted, as these organizations have to compete for talent with the for-profit sector.

On the long-term incentive (LTI) side, more than half of private companies provide LTIs, with multi-year, cash-based performance awards being the most common vehicles. Other types of long term compensation incentives include:

- Real equity, which includes restricted stock and stock options

- Phantom equity, which includes phantom stock and stock appreciation rights (SARs).

Long term incentives at private companies continue to be primarily reserved for executives. Private companies reported using LTIs for retention, alignment with long-term goals and market competitiveness. At NGOs, longer term pay incentives continues to be rare, but prevalence increased to 24% in 2017 from 16% in 2015. Future compensation research will determine whether this trend continues.

Incentive Pay Trend: Increase in Short Term Incentive Spending

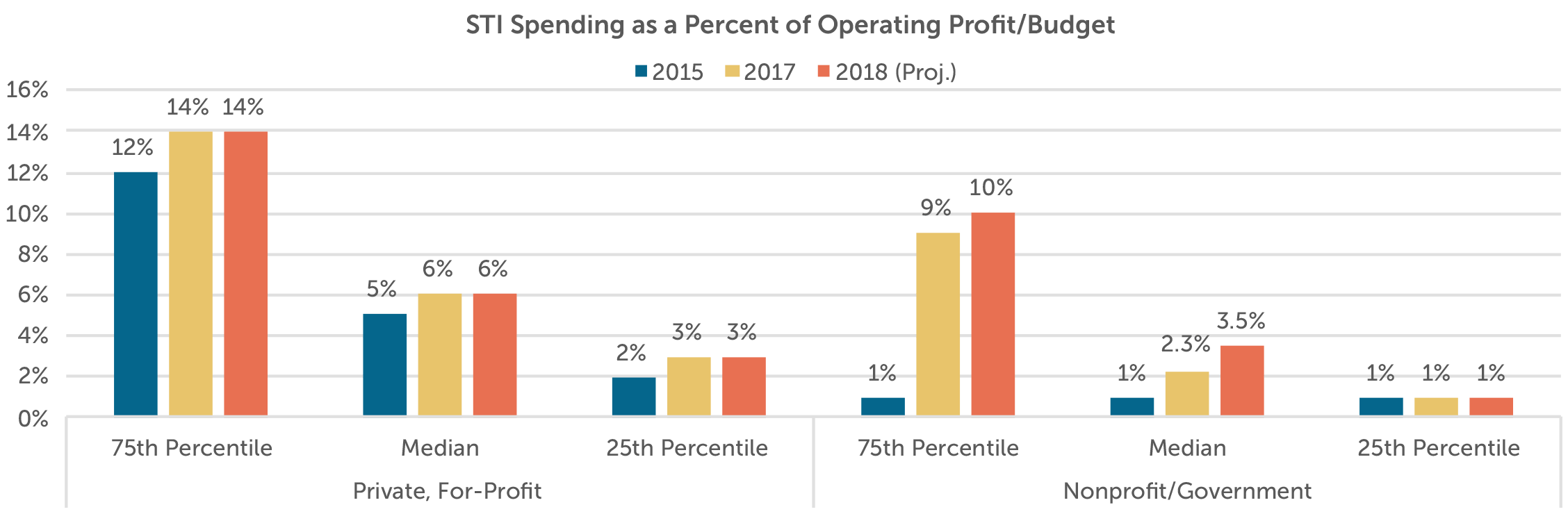

Private companies are spending more on STIs to motivate employees and compete for talent in a tight labor market. Private-company spending on short term incentives increased to 6% of operating profit at median from 5% in prior years. In addition, spending on STIs increased to 3% (from 2% in 2015) at the 25th percentile. At the 75th percentile, spending increased to 14% from 12% in 2015.

At NGOs, compensation survey respondents provided nonprofit estimated spending on short term incentives as a percentage of net organizational surplus (revenue minus expenses). In contrast to private companies, NGO spending on STIs slightly dropped at the median to 2.3% in 2017 from 3% in 2015. Similarly, reported spending by NGOs at the 75th percentile dropped to 9% in 2017 from 10% in 2015. However, participants expected STI spending as a percentage of their operating surplus to increase to 3.5% at median in 2018, as the budgetary outlook for 2018 appeared positive.

Incentive Pay Trend: Increased Annual Incentive Plan Eligibility

At private companies, the prevalence of exempt, salaried employees and nonexempt (salaried or hourly) employees included in Annual Incentive Plans increased in 2017. The biggest jump occurred for nonexempt employees. About two-thirds of nonexempt employees are now eligible for annual incentives, a significant increase from half in 2015. Annual incentive plan eligibility is now offered organization-wide at most private companies, reflecting the tight labor market and increased competition for talent. Eligibility for incentive plans is good news for employees who are now able to earn annual incentive awards and increase their overall compensation levels based on performance.

For nonprofit and government organizations, AIP eligibility increased for all organizational levels from manager/supervisor and above. Annul Incentive Plan eligibility decreased slightly for exempt employees and remained stable for nonexempt employees. The increased AIP eligibility for supervisory and management positions and above at NGOs indicates that these entities are using their limited annual incentive dollars within their salary and compensation budgets to compete with for-profit peers for top managerial and executive talent.

Incentive Pay Trend: Annual Incentive and Long-term Incentive Targets as a Percentage of Salary

For the first time in the Vivient/WorldatWork Private Company & NGO Compensation Survey’s history, participants were asked to provide typical AIP and LTI targets as a percentage of salary for broad position levels. For-profit, private companies that provide Annual Incentive Plans offer CEOs a median target award of 80% of salary. Target AIP awards decrease by approximately half for each broad position band below CEO. NGOs that provide Annual Incentive Plans tend to offer more modest target awards than for-profit counterparts.

|

Target Annual Incentive Award at Private Companies & NGOs (Percent of Salary) |

||

|

For-Profit Private |

NGO | |

| CEO | 80% | 40% |

| Other Executives/Officers | 40% | 25% |

| Managers/Supervisors | 15% | 10% |

| Exempt Salaried | 10% | Insufficient data |

|

Nonexempt Salaried and Hourly |

5% | Insufficient data |

NOTE: Excludes companies that do not offer Annual Incentive Plans

For Long Term Incentive Plans, private companies reported target long-term awards as a percentage of salary for executives. Data specific to private companies is difficult to find in published compensation surveys, which shows the value of this survey to WorldatWork members. The survey findings indicate that private companies offer an annual Long Term Incentive benefit that is approximately equal to the Annual Incentive Plan opportunity. This rule of thumb provides private companies that offer long-term incentives with a starting point for evaluating appropriate LTI levels for executives.

|

Target Long Term Incentive Awards at For-Profit Private Companies (Percent of Salary) |

|

| CEO | 80% |

| CEO’s Direct Reports | 50% |

| Vice Presidents/Officers | 30% |

NOTE: Excludes companies that do not offer Long Term Incentive Compensation

Incentive Pay Trend: Concerns About Annual Incentive Plan Effectiveness

Both private, for-profit companies and nonprofits reported a downward trend in the effectiveness of their Annual Incentive Plans. The risk-reward trade off was the biggest AIP weakness noted at both private companies and nonprofit/government organizations. This indicates that award payouts may not be adequately calibrated with results in terms of employee performance. For example, outstanding performance may result in only a moderate increase in the annual incentive payout. Conversely, below-target performance may result in a disproportionately small decrease from the targeted award level.

The level of discretion also was cited as a common weakness in Annual Incentive Plans, especially at private companies. The survey asked participants to provide information on strengths and weaknesses in the use of discretion. Private companies cited communication of the rationale for discretion, and the perception of fairness and consistency across the organization as the biggest weaknesses in the use of discretion. In contrast, NGOs do not seem to use discretion as much as private-company counterparts and did not report on specific weaknesses in its use. This lack of response may indicate that NGOs may see the need for a greater role for discretion in their AIPs, as it is more difficult to quantify performance at these organizations.

Incentive Pay Trend: More Cash-Based and Less Real Equity for Private-Company Long Term Incentives

With respect to Long Term Incentives, LTI performance awards — long-term cash plans, performance units and performance shares — continue to be the most popular vehicles at private companies. Because private companies do not have equity that is traded and valued on a stock exchange, cash-based plans are simpler and less expensive to design, operate and administer. The use of real equity decreased in 2017 after an uptick in the use of stock options in the 2015 survey. Private companies appear to now favor simpler, cash-based long-term incentives to avoid equity-related complexities such as valuation, liquidity and the dilution of ownership.

Incentive Pay at Family-Owned Private Companies

Nearly one-third of the private-company sample was family-owned, and these firms mirrored the broader private-company sample results although with some key distinctions:

- Higher short term incentive spending at family-owned companies

- Family-owned companies reported higher spending on short term incentives as a percentage of operating profit relative to the broader sample. Family-owned companies spent 10% of operating profit at median in 2017 and project an 8% STI budget for 2018. In contrast, the broader sample of private companies spends a median of 6% of operating profit annually.

- The higher spending on STIs at family-owned companies may be a strategy to attract external talent to help manage the business. Also, family-owned businesses typically provide a pay mix that is heavier on short-term cash compensation, as they tend to be more selective in providing longer term incentives.

- Lower use of long term incentives at family-owned companies

- Family-owned companies are less likely than the broader sample to offer an LTI plan. Only 44% of family-owned companies offer LTI plans, compared to 54% in the broader sample.

- Like the broader sample, family-owned companies favor performance awards, such as cash plans or performance units, over real equity or phantom equity that requires a company valuation.

Compensation Trends at Private Equity-Owned Companies

For the first time in this 2017 compensation survey research, respondents were asked to report whether private-equity firms own a stake in their companies. About a quarter of the respondents reported private equity investments in their companies and had some key distinctions in survey findings:

- Lower Short term incentive spending at private-equity owned companies

- Private equity-owned companies spend slightly less than the broader sample on STIs. These companies spend 5.5% of operating profit at median on STIs, in contrast to 6% for the broader sample.

- Private equity owners have the strategy of aligning executives’ economic interests with their own (i.e., creating a value realization event). As a result, executive compensation is focused more on LTIs than on short-term incentives.

- More long-term incentives and real equity ownership at private-equity companies

- Private-equity owned companies are more likely to provide LTIs than the broader sample. Almost two-thirds of private-equity-owned companies reported having an LTI plan.

- LTIs based on real equity — stock options and restricted stock — are favored by private equity investors, as these vehicles align the incentives of management with the shareholders and provide a retention mechanism. Also, private-equity owned companies tend to grant LTIs deeper into the organization versus the broader survey sample.

Where Private Company and NGO Compensation Preferences Are Trending

Private companies and NGOs continue to favor short-term and cash-based incentives. Future compensation research by Vivient Consulting and WorldatWork will focus on whether the tight labor market and competition for talent continue to drive non-publicly traded entities to spend more on incentives and broaden incentive participation across more employees.

Principal Bonnie Schindler discusses the compensation survey research conducted by Vivient and WorldatWork around incentive pay practices for private, non-profits and government entities.

The transition from a private company to a public company is an exciting time for most organizations. For employees, moving from private to public status provides the first opportunity to potentially gain liquidity from equity-based. For venture capital or private equity investors, it typically represents the first opportunity to realize gains from their investment and risk-taking. However, becoming a public company creates new disclosure requirements and opens up compensation programs to scrutiny from a new group of public shareholders and shareholder advisory firms.

Not all newly public companies are the same. In this white paper, we will speak generally about newly public companies, but also address differences that may apply across categories. The categories we most typically see are the following:

- Recent Start-ups: Companies that have been funded primarily by venture capital backers and are in early stages of development

- Often these companies are in the biotech or internet/technology industry and some, in particular in biotech, may be pre-revenue and likely pre-profit when they go public.

- Companies in this category are usually emerging growth companies (revenue less than $1 billion at IPO) under the JOBS act, subject to less stringent disclosure requirements and exempt from Say on Pay votes for up to five years following IPO

- Private Equity Portfolio Companies: More mature businesses that may have been taken private to improve operating performance

- Typically are profitable businesses and trade based on multiples of earnings or EBITDA

- May or may not be “emerging growth companies” under the JOBS act

- Private equity owners may continue to maintain a majority interest following IPO

- Spin-off Companies: Business units of a publicly traded company that become public through a spin-off event

- Spin-off may occur in one stage, an initial IPO and then a spin-off of remaining shares, or a multi-stage sell-down

- In most cases, the spin-offs are mature companies that are viewed as being able to generate more value on their own through greater strategic focus than as part of the parent company

Establishing Public Company Compensation Processes

As a public company, there is an increased requirement for processes governing the company’s compensation decisions. All public companies (other than those controlled by a 50% or greater shareholder) need to have a Compensation Committee of two or more independent directors. The Compensation Committee needs to have a Charter that lays out the responsibilities of the Committee, including its responsibility for overseeing the pay of the CEO and the other executive officers of the company.

In practice, there is a lot of work to set-up a functioning Compensation Committee. Key steps to get a Committee up and running include the following:

- Identify Members: The Board needs to determine which directors have the capabilities and experience to effectively serve on the Compensation Committee;

- Appoint a Chair: The Board needs to identify a Chair for the Committee who can ensure that the Committee operates effectively and meets its responsibilities under the Charter;

- Draft Charter: Company’s counsel needs to draft a Charter outlining the Committee’s responsibilities in compliance with the listing standards of its respective exchange and addresses the expectations of the Board for the Committee;

- Establish Committee Calendar: Human resources needs to work with the Committee Chair to develop a calendar of activities for the year (including the timing and number of Committee meetings) and cross-reference with the Charter to ensure that all responsibilities are addressed;

- Assess Need for External Advisor: The Committee needs to assess whether or not they need an advisor; if they elect to use an advisor, they need to conduct a selection process and assess the independence of the advisor;

- Develop Committee Meeting Process: Establish protocols for the companies interaction with the Committee and preparation for meetings; best practices include the following:

- Provide Committee Chair with a draft agenda for the meeting at least one month in advance of the meeting;

- Review draft materials with the Committee Chair (and Committee advisor) at least 1-2 weeks in advance of the meeting;

- Make materials available to Committee members one week in advance of the meeting;

- Ensure that at least 2 meetings are provided for major decisions; one meeting to review and second meeting to approve; and

- Follow-up with Committee Chair following Executive Session to confirm decisions made in the meeting.

Many companies adopt some of the above practices in advance of going public and this tends to make the transition easier. We find that new Committees have some room to learn as they go; however, the fundamentals of the process should be in place upon going public.

Post-IPO Compensation

In most cases, prior to going public, the compensation program likely was comprised of a relatively modest base salary and annual incentive and significant stock option grants. This approach to compensation is very common for emerging growth companies and private equity-backed companies. Spin-off IPOs may vary from this approach, as they often have relied on the more traditional compensation models of their parent companies. Upon going public, the company may need to rethink its approach to compensation. At the very least, there has to be recognition that employees may have opportunities to recognize significant wealth from past equity grants and the company needs to ensure that the compensation program will be effective in retaining top talent following the IPO. In addition, while the company may have had a relatively small shareholder base to address as a private company, once public, there is a larger group of shareholders and the company needs to make sure that the compensation program of the public company is designed with all shareholders in mind.

Pay Philosophy, Peer Group and Target Pay Levels

For a newly public company, one of the most fundamental compensation decisions is to establish a compensation strategy and pay philosophy. Most companies will want to ensure that the compensation program addresses the following objectives:

- Align executives with shareholders’ interests

- Support achievement of the business strategy

- Pay-for-performance

- Attract and retain required talent

A company’s compensation strategy and design can work to achieve these objectives in a variety of ways and there are tradeoffs among the objectives. For example, compensating executives with equity can serve to align their interests with shareholders; however, executives may place a higher value on cash compensation. Companies will take a variety of approaches based on the relative priority of the different objectives and their views on which compensation design elements best meet the objectives.

As part of the compensation philosophy, while not required, companies will frequently identify a peer group. The peer group is comprised of publicly traded companies and used for pay and/or performance benchmarking. Since one of the primary purposes of the peer group is to assess the competitiveness of pay, a key factor in identifying peers is whether the companies are potential competitors for executive talent. In addition, for external credibility, the peer group should be comprised of companies that are comparable in size (e.g., ~.5x – 2x) your company’s size in terms of revenue and from comparable industries. Ideally, some of the peers will also be newly public companies, though this is less important for more mature companies that are going public.

Most public companies establish a pay philosophy discussing the positioning of target pay levels. The most common pay philosophy statement is along the lines of “our company targets total pay levels at the median of our peer group with variation around median based on individual circumstances.” There is flexibility to have a pay philosophy that targets pay levels above median, but these pay philosophies often attract criticism from shareholders. Alternatively, the company could target below median base salaries and annual incentives and deliver above median long-term incentives. This approach to pay may be more appealing to shareholders, especially with growth companies, with its emphasis on long-term compensation.

Annual Incentive Program

Pre-IPO companies may or may not have a formal annual incentive plan. For some emerging growth companies, there may be a focus on conserving cash and therefore limited cash available for compensation and as a result, the companies may deemphasize annual incentive compensation. In addition, early stage companies in some industries (e.g., biotech, internet) may not have strong income statement performance (e.g., revenue or profitability) and may tie the incentives they pay to the achievement of strategic objectives (e.g., successful clinical trials, product launches, etc.)

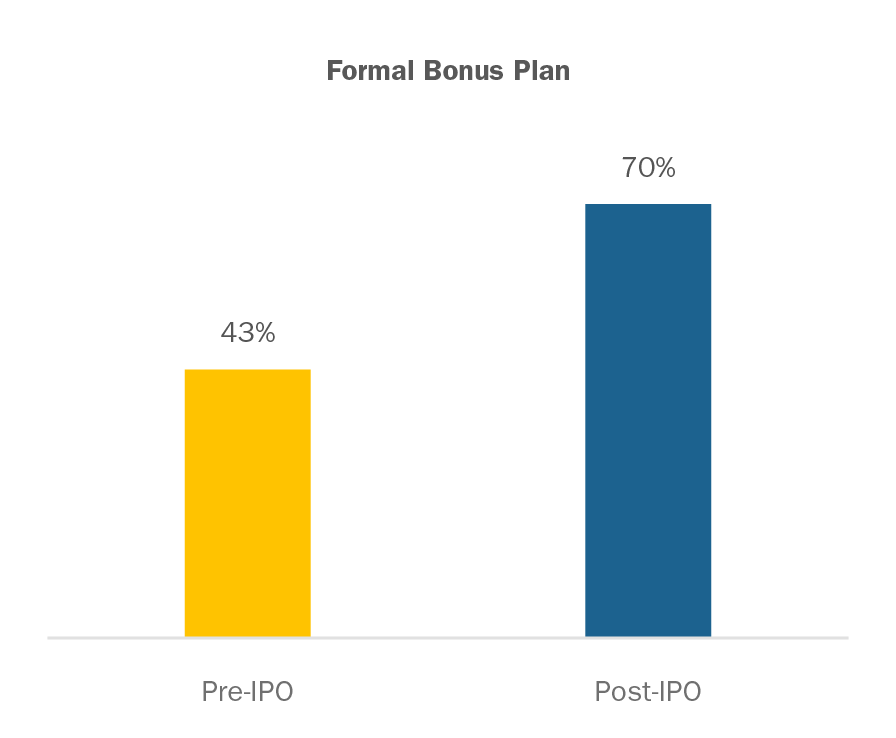

Once companies are public, there are greater expectations from shareholders and shareholder advisory groups that if the company pays an annual incentive, it will be based primarily on the achievement of financial results, with only a small portion based on more qualitative performance criteria. The larger the annual incentive opportunity is as a percentage of total compensation, the greater the expectation that the incentive will be based on financial performance. Shareholders will generally not be happy if a CEO can earn a bonus equal to 50-100 percent of base salary, unless the company has delivered strong financial results. Our analysis of 30 recent IPO’d companies found that 70% have adopted formal bonus plans with quantitative metrics following the IPO.

Note: For both annual and long-term incentives based on the tax code rules (IRC Sec. 162(m), the “performance based compensation” tax exemption for select executive officers), if a company gets an annual and long-term incentive plan approved prior to the IPO and discloses such plan documents in any S-1 filing, the company is exempt from IRC Section 162(m) rules for approximately three years.

Long-term Incentives

Pre-IPO companies typically use stock options as the main long-term incentive vehicle as they tend to closely align the interest of the venture capital or private equity investors. Rather than making annual grants to executives, pre-IPO companies will generally make large up-front grants to lock in on an early (presumably lower) valuation for purposes of determining the exercise price. In many cases, the equity grants are established as a percentage of the company’s common shares outstanding rather than a targeted dollar value. If an executive has served with the company for a number of years prior to the IPO, then it is possible that all or a majority of the stock options that the executive holds are vested by the IPO. This may be a concern for shareholders for potential shareholders and the company needs to demonstrate it has a game plan for locking in the executives post-IPO.

An important first step for the company as it approaches the IPO is to assess whether its existing reserve of shares set aside for grants to employees and directors will be adequate to cover future grants. It is generally preferable to obtain approval of additional shares for future grant prior to the IPO, as the equity plan needs to be approved by shareholders and it is simpler to gain approval from the VC or private equity shareholders than the new public shareholders. We recommend that the equity reserve and overhang (i.e., share reserve plus outstanding awards relative to total shares outstanding) be benchmarked relative to peer practices to ensure that the reserve will not be viewed as excessive by external shareholders, as eventually the company will have to go to public shareholders for purposes of 162(m) compliance and/or additional shares.

In situations where executives’ equity is largely vested by the time of the IPO, the company may use the IPO as an opportunity to “re-up” equity grants to senior executives to “lock them in” for the next few years following the IPO. However, in order to size any grants made at IPO, the company will likely want to rely on competitive market practices for annual grant values among the peer group. In addition, the company may want to consider shifting to an annual grant frequency, as this is the most common equity granting approach among publicly traded companies.

Public companies have moved toward an annual grant frequency for several reasons, including the following:

- Limits the impact of stock price volatility on option values (e.g., lowers the risk that all stock options end up underwater)

- Facilitates compliance with target compensation positioning (i.e., easy to adjust annual compensation to market competitive levels)

- Results in consistent disclosed compensation values over time and tends to be better received by shareholder advisory groups

Over time, larger newly public companies (particularly those with revenue over $1 billion) may be expected to incorporate a long-term incentive vehicle with explicit performance measures into their long-term incentive designs. Institutional Shareholder Services (ISS) expects that 50% of the long-term incentive opportunity be delivered in a performance-based vehicle and they do not view time-vesting stock options as highly performance-based. In practice, newly public companies may have legitimate reasons to delay adopting a performance-based long-term incentive (e.g., limited stock trading history, challenges in forecasting long-term financial performance).

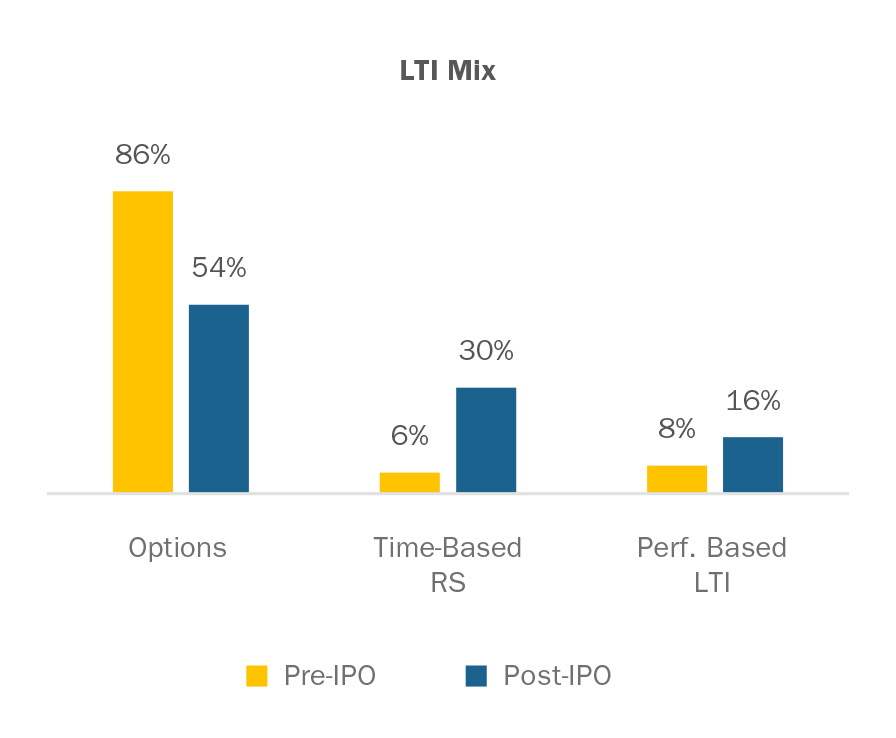

If you decide to adopt a performance-based long-term incentive, the most common design is a performance-share plan. These plans provide for a target opportunity denominated as a number of shares. Performance is typically assessed over a three-year period, with the number of shares earned ranging from a threshold amount (typically 25%-50% of target) to a maximum amount (150%-200% of target) based on an assessment of performance relative to pre-established performance criteria. Plan designs are mixed among measuring performance relative to financial criteria (e.g., EPS, revenue growth), stock price performance (e.g., total shareholder return relative to peers or the broader market), or a combination of financial and stock price performance. Performance share plans are now the single most prevalent form of long-term incentive for executives at large public companies. In our analysis of the post-IPO practices of 30 recent IPOs, we found that the LTI mix for post-IPO grants shifted away from stock options with weight shifted towards time-based restricted stock and performance-based LTI.

Other Compensation Design Features

Severance provisions should be established as part of a formal severance program (change in control or not change in control) or through severance agreements, or less frequently, as part of an employment agreement. These programs should be implemented after careful consideration of potential costs and benefits to the participants, competitive practices for comparable organizations and if the company desires to maintain a formal program. Gross-ups for any 280(g) CIC tax liabilities are no longer common and should not be included. If not already in place, non-compete and non-solicitation provisions should be put in place for the company, as standalone policies or as part of LTI award agreements.

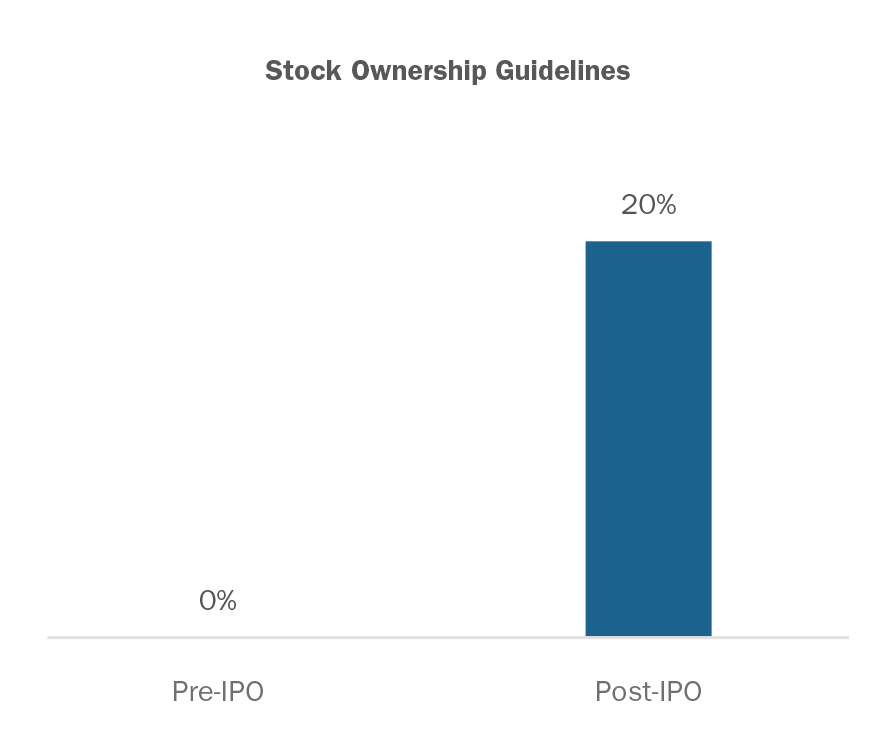

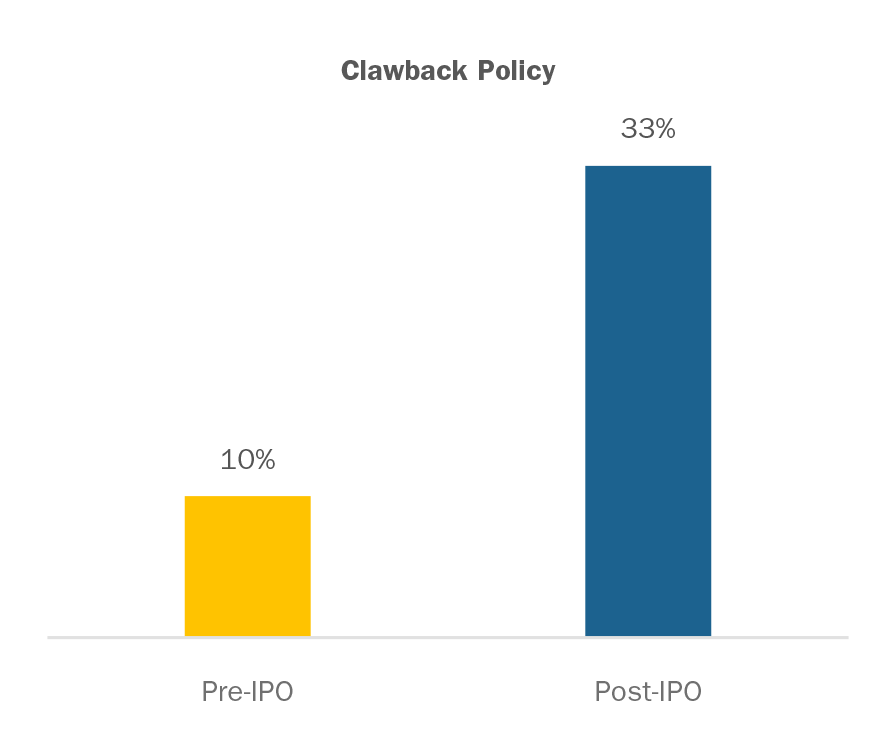

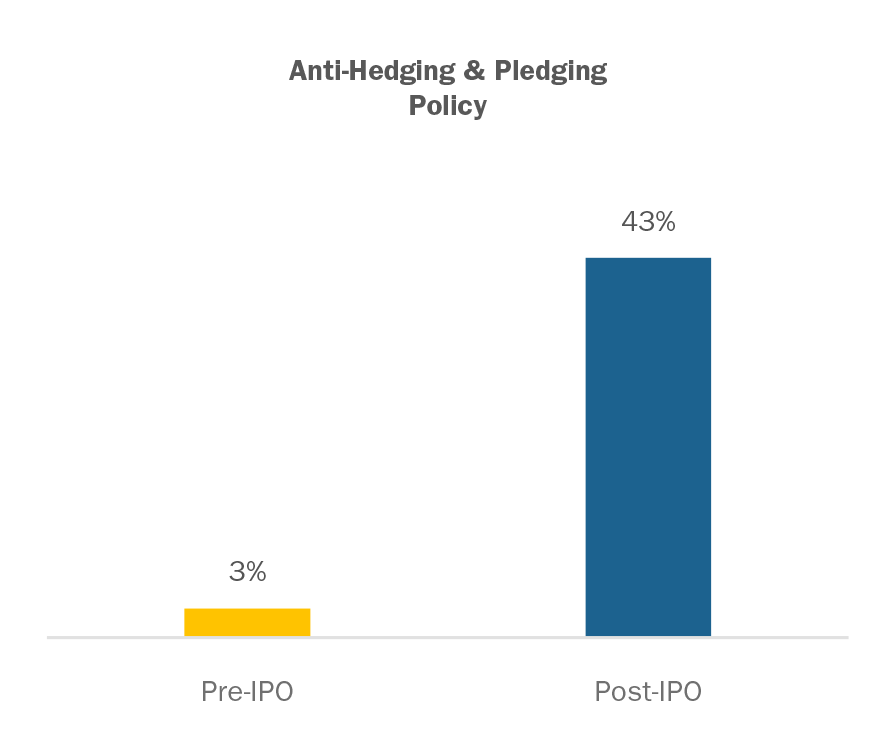

Lastly, other good governance features such as stock ownership guidelines, clawbacks (recoupment policy), and anti-hedging and pledging are considered good practice and are also generally in the best interests shareholders (see data on post-IPO adoption below). How quickly the company adopts these practices depends on how far the company wants to go to be viewed as shareholder friendly.

Conclusions

The IPO is an exciting time for executives and private company shareholders. From a compensation perspective, it is also an exciting time as the company transitions from a model built around an eventual liquidity event to a compensation program that is expected to be maintained over time as a public company. As a public company, the compensation program will be under additional scrutiny and the Compensation Committee will be accountable to a much larger shareholder base. By developing strong compensation governance practices and understanding competitive practices for pay program, Compensation Committees can move forward with confidence that their approach to compensation will meet the strategic needs of the company and stand-up to external scrutiny.

In November 2015, Vivient Consulting and WorldatWork invited a sample of WorldatWork’s non-publicly traded members to participate in their second “Incentive Pay Practices: Privately Held Companies” compensation survey. Approximately 200 private, for-profit companies responded to the survey, representing manufacturing, consulting, professional, scientific and technical services, finance and insurance, media, software and retail trades. This compensation survey updates the original survey completed by Vivient and WorldatWork in 2013.

The new 2016 compensation survey research shows that short-term cash incentives and bonus programs continue to dominate the incentive-pay landscape as a vast majority of organizations use and rely on incentive-based pay practices to recruit, motivate and reward employees.

Vivient’s Bonnie Schindler reports: “While cash continues to dominate long-term incentives at private companies, we are seeing an uptick in the use of real equity in the form of stock options.”

Key Findings from the 2016 Compensation Survey for Private, For-Profit Organizations

- Between 2013 and 2015, the prevalence of short- and long-term incentive programs remained steady at private companies. Short-term incentives decreased slightly to 94% from 97%, while long-term incentives also decreased slightly to 53% from 56%.

- In 2015, almost 75% of privately held companies with a short-term incentive plan offered at least three programs.

- Annual Incentive Plans (AIPs), the most prevalent short-term incentive plan at private companies, are offered to employees at the exempt, salaried level and above at most organizations.

- At the 75th percentile, the majority of private companies increased their short-term incentive budgets to 12% of operating profit in 2015. They forecast an increase to 14% of operating profit for 2016.

Increasingly we find that private companies are adopting public company governance practices such as using formal Compensation Committees consisting of internal or external Board members.

Unlike publicly traded companies where a Board Compensation Committee is a requirement, private companies establish formal Compensation Committees for reasons such as the desire for:

- A more defined and objective process. This is welcome in delicate situations such as where there are conflicting shareholder interests that need to be aligned, or there is a perception that management has undue influence on setting their own pay levels.

- Additional Board-level attention and/or external compensation expertise. This may be necessary when companies establish new key executive compensation plans or need to have one point of contact to negotiate employment contracts with key executives.

A Compensation Committee is able to take a “deep-dive” into specific compensation issues in a manner that would be more difficult and/or impractical with an entire Board.

Below we outline the key aspects of well-run Compensation Committees:

Purpose: Typically, the Compensation Committee’s purpose is to carry out the responsibilities delegated by the Board relating to the review and determination of the performance and compensation of the Chief Executive Officer and the executive team. Each company’s Board needs to decide whether the Compensation Committee itself has the authority to approve compensation decisions, or makes its recommendation for Board approval.

Membership: Compensation Committees are usually comprised of a small select number of members, which can be a sub-set of the Board of Directors and can be supplemented by independent outside advisors, if desired. As an example, one of our private company clients has a Compensation Committee which consists of internal Board members supplemented by an external compensation consultant and a long-time outside advisor. Ideally, the Compensation Committee should include at least one member with compensation experience and/or a member with related, although not necessarily direct, subject matter expertise.

Duties: The duties of the Compensation Committee are to review the compensation and performance of the Chief Executive and, to some extent (to be defined by each company), the members of the executive team. The Compensation Committee also typically reviews compensation levels and plans (annual incentive, long-term incentive, supplemental benefit and perquisites) and major agreements (employment, severance, change of control, etc.). It may also review non-executive officer compensation and broad-based plans on a periodic basis, as and when appropriate. Increasingly, the role of CEO succession planning is also being assigned to the Compensation Committee.

Operations: We recommend that companies establish a Compensation Committee Charter and Calendar. The Charter specifies the Compensation Committee’s role, duties, responsibilities, and membership, as well as its operations (such as the number of meetings per year, review of its own performance, etc.). The Calendar sets the schedule of topics to be addressed at each of its meetings throughout the year. For instance, at the Q1 meeting, the Committee will review and approve salary increases for the upcoming year, bonuses for the prior year and equity grants. Topics would also be outlined for the remaining fiscal quarters. By having both of these documents, the purview and process of the Compensation Committee are clear to all constituents (Board members, shareholders, and management).

While it takes some time for private companies to recognize the benefits of establishing a Compensation Committee, we find that Boards come to appreciate having a dedicated and knowledgeable resource that can regularly address compensation issues on its behalf.

Partner Susan Schroeder and Principal Bonnie Schindler are interviewed on their 2014 survey private company incentive pay practices.

Do incentive-pay practices differ between publicly traded and privately held companies? If so, how? Research released this year by WorldatWork, Deloitte Consulting and Vivient Consulting set out to answer these questions.

Incentive-pay practices do differ between public and private companies. Short-term incentives (STIs), including annual incentive plans, are structured similarly across both organizational types. However, public companies are much more likely than their private counterparts to offer STIs to the broader employee population. In contrast, private companies place greater emphasis on STIs in their total rewards programs, as STIs are the companies’ most effective compensation tool for attracting and retaining talent. However, private companies tend to reserve short-term rewards for exempt employees and above.

On the long-term side, publicly traded companies rely heavily on long-term incentives (LTIs), such as restricted stock and stock options. Restricted stock has surpassed stock options as the LTI vehicle of choice for public companies. In contrast, private companies favor cash LTI plans, such as bonus plans with goals and payouts tied to multiyear performance, over real equity. Public companies are more likely to make broad-based equity grants to the larger employee population, while private companies concentrate LTI awards on top executives.