Last year, the study showed an increase in compensation for both CEOs and CFOs, but at much lower levels than the prior year. This leveling off of pay was partially driven by a stabilizing economy and increased confidence in goal setting, leading to less volatility in corporate performance results in incentive plans. To determine if this trend is continuing, we conducted a similar study in 2013 using a sample set of 62 US public companies. The study analyzes executive pay data disclosed by companies with revenues ranging from $1 to $145 billion, with median revenues of $9 billion. Only companies with the same CEO and CFO incumbents from 2010 to 2012 were included in order to focus on year-over-year changes for an individual incumbent. Similar to our methodology in prior years, financial services firms were excluded from the study, as this industry’s compensation practices continue to evolve in the years post the financial crisis.

Our findings, summarized below, indicate that overall, increases in total compensation levels for both CEOs and CFOs slowed in 2011-2012 compared to double-digit pay increases in the 2009-2010 period and mid-single-digit increases in the 2010-2011 period. This dramatic slowdown suggests that the halting economic recovery is having an impact. Percentage pay increases in all three years were higher for CFOs compared to CEOs, driven by slightly higher increases in long-term compensation and smaller decreases in annual bonus. The slower rate of growth in CEO compensation may be driven by the continued focus on CEO pay by shareholders and proxy advisory firms and the increased demand for pay and performance alignment. On an absolute basis, CFO pay continues to be approximately one-third of CEO pay.

Study Results

Salaries

In 2012, approximately 85% of CFOs received salary increases. The median increase was 3.0% and the 75th percentile increase was 4.9%. In comparison, only 53% of CEOs received salary increases and the increases were smaller — 0.5% at median and 3.1% at the 75th percentile. The prevalence of salary increases for CFOs remained similar to last year with about 85% of incumbents receiving a salary increase. Among CEOs, approximately 55% received a salary increase, similar to 2010.

|

Salary Increase Prevalence |

||||||

|

|

2009 – 2010 |

2010 – 2011 |

2011 – 2012 |

|||

|

|

No Increase |

Increase |

No Increase |

Increase |

No Increase |

Increase |

|

CEO |

43.8% |

56.3% |

34.4% |

65.6% |

46.8% |

53.2% |

|

CFO |

25.0% |

75.0% |

12.5% |

87.5% |

14.5% |

85.5% |

Actual Pay Levels

Overall, actual total direct compensation (salary plus actual annual incentive plus the grant date value of long-term incentives) for CEOs and CFOs leveled off in 2011-2012. These lower, single-digit changes in pay levels are consistent with the increased focus on pay for performance we have seen over the last few years. They also likely reflect the slow pace of economic recovery. At the median, salary increases were higher for CFOs than CEOs in 2011-2012. Bonus levels decreased for both CEOs and CFOs and long-term incentives increased modestly (2%) for CFOs and remained flat (0%) for CEOs.

|

Median Percentage Change in Pay Components |

||||||

|

|

2009 – 2010 |

2010 – 2011 |

2011 – 2012 |

|||

|

Pay Components |

CEO |

CFO |

CEO |

CFO |

CEO |

CFO |

|

Salary |

1.0% |

3.7% |

1.8% |

3.5% |

0.5% |

3.0% |

|

Actual Bonus |

19.0% |

22.7% |

0.0% |

3.5% |

-2.8% |

-1.2% |

|

Long-Term Incentives |

10.1% |

14.8% |

10.0% |

10.3% |

0.0% |

2.0% |

|

Actual Total Direct Comp. |

14.4% |

20.0% |

3.6% |

7.5% |

-0.3% |

1.4% |

|

Financial Performance (Median Levels) |

|||

|

Year |

Total Shareholder Return (as of 12/31) |

1-Year Revenue Growth |

1-Year Net Income Growth |

|

2010 |

24% |

10% |

19% |

|

2011 |

5% |

9% |

13% |

|

2012 |

14% |

3% |

2% |

While movement in pay among CFOs and CEOs was directionally aligned, absolute CFO total direct compensation levels, on average, have been approximately 30% of CEO total direct compensation levels over the last three years.

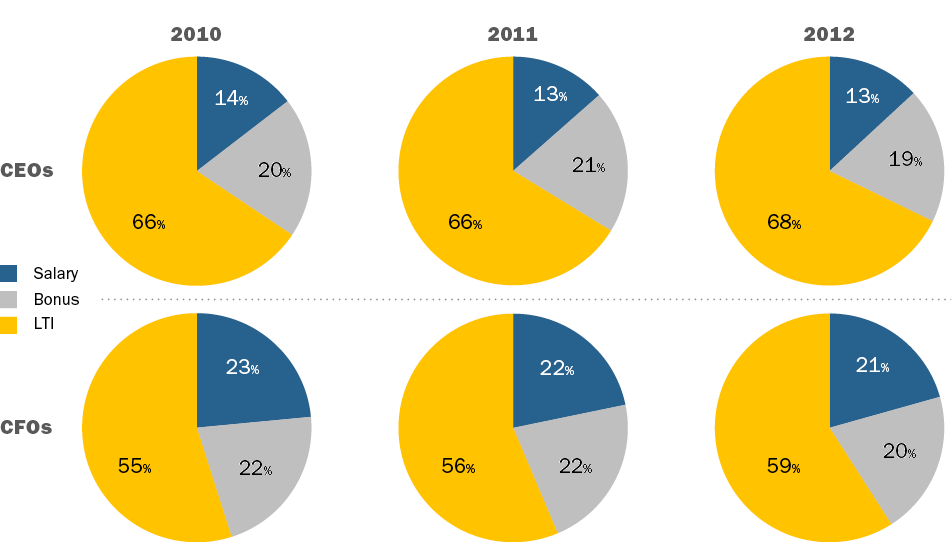

Target Pay Mix

In terms of target compensation levels, the overall pay mix remained largely unchanged from 2010 to 2012, with a greater emphasis on at-risk pay for CEOs than for CFOs.

Long-Term Incentive (LTI) Vehicle Prevalence and Mix

The use of at least two long-term incentive vehicles continues to be the majority practice when awarding LTI to CEOs and CFOs. The role of stock options has remained steady in the overall mix with companies delivering about 30% of LTI using this vehicle. On average, performance-based LTI continues to comprise approximately 50% of LTI for CEOs and CFOs. Data shows that 80% of CFOs and 85% of CEOs received some form of performance-based awards as part of their LTI program in 2012.

|

Number of LTI Vehicles Used in 2012 |

||

|

|

% in Total |

|

|

CEO |

CFO |

|

|

1 |

24% |

17% |

|

2 |

47% |

53% |

|

3 |

27% |

28% |

|

Average |

2 |

2 |

|

LTI Mix |

||||||

|

2010 |

2011 |

2012 |

||||

|

Vehicle |

CEO |

CFO |

CEO |

CFO |

CEO |

CFO |

|

Stock Options |

33% |

30% |

32% |

32% |

30% |

32% |

|

Time Vested Restricted Stock |

20% |

23% |

17% |

22% |

16% |

20% |

|

Perf. Based LTI |

48% |

47% |

51% |

46% |

53% |

48% |

Conclusion

As companies and Boards focus on the alignment between pay and performance, and the economic recovery continues at a slow pace, it is not surprising that pay increases have slowed over the last 3 years. The rates of increases continue to be for higher CFOs compared to CEOs; however, the increases for both have slowed dramatically in 2011-2012. We expect future changes in compensation for these positions to continue to be closely linked to overall company performance, as well stock price performance, since the majority of pay for CEOs and CFOs is delivered through long-term incentives.

Key 1: Committee Composition

Composition of the board Compensation Committee is the first step toward achieving an effective Committee. Below are some tips to keep in mind when determining which Board members should be on the Compensation Committee:

- Compensation Committees are typically composed

of 3 – 5 board members with different, yet complementary backgrounds and skills - The Committee should have representation from an active senior executive, an academic, an industry expert, etc., as appropriate. If the Compensation Committee is composed of members with different backgrounds it will allow for more comprehensive and fully vetted discussions

- The Chair of the Committee should be a strong facilitator who pushes forth open discussion and is willing to hear opposing viewpoints, while being an effective communicator and consensus builder

- The Chair works to bring meetings to resolution and to conduct efficient meetings

Key 2: Planning

A second important factor for having an effective Compensation Committee is proper planning. Providing Committee members with a road map of what is going to happen at each meeting and throughout the year allows for a more thoughtful approach to topics. Some planning tips include:

- Annually review the Compensation Committee charter to ensure that the Committee complies with their responsibilities and to see if any changes are required based on regulatory and legislative changes, or evolving practices

- Review the annual calendar at the beginning of each fiscal/calendar year and highlight any key priorities for the year (e.g., long-term incentive plan re-design)

- Provide Committee member education on key and emerging topics on an ongoing basis so they can make informed decisions. Recent emerging topics include the risk assessment process, SEC disclosure rules, shareholder red flags, and the voting policies of the two main proxy advisory firms – Institutional Shareholder Services (“ISS”) and Glass Lewis

- Obtain views of shareholders on an ongoing basis; listen closely to shareholders to get ahead of any potential issues on an annual basis

- Educate new members to provide them with a background on the company’s historical pay practices and performance

Key 3: Establish Processes

Finally, another important factor for having an effective Compensation Committee is having proper and systematic processes for each Committee meeting. Effective Committee processes include:

- Set meeting dates with plenty of lead time to allow for well attended meetings by Committee members, management and external advisors

- Preview each meeting agenda with Committee Chair; establish time limits for topics

- Preview meeting materials well in advance of meetings to address all issues that may potentially arise

- Allow major decision points to be covered at two meetings to give the Committee time to preview and fully vet prior to final approval

- Ensure open and ongoing communication with management to have context for decision making

- Involve the Audit Committee and company Finance during the goal setting process for absolute performance plan goals in the annual incentive and long-term incentive plans

- Involve Legal in CD&A and proxy disclosure, potential filings related to any pay decisions and other technical issues

- Annually test effectiveness of pay plans relative to actual company and stock price performance as well as pre-established goals

- Monitor evolving regulatory, legislative and corporate governance practices by including the topic as an annual or biannual agenda item

- Conduct an executive session at each Committee meeting to ensure any concerns are addressed

- Schedule calls after each Committee meeting with Committee Chair, management and external advisors to debrief and confirm next steps

- Annually assess the performance of the Compensation Committee and its external advisors during the self-assessment process

In our experience, Compensation Committees that incorporate these three keys have more efficient meetings and are more effective in bringing tough decisions to resolution. While not all approaches will be the same, using a framework with similar characteristics often leads to more engaged Committee members and more organized meetings. In today’s environment, with Say on Pay and increased shareholder concerns, it is increasingly important to have a best-in-class Compensation Committee.

If a separate Chair role is desired, the position may be occupied by either an executive or a non-executive. An Executive Chair is frequently a founder or a recently retired CEO who continues on as Chair for a transition period. In a few cases, particularly where a high level of Board independence is necessary, an outsider is hired into the role. In contrast, a non-executive Chair is often a sitting member of the Board whose role is expanded.

At companies where the roles of Chair and CEO are combined, the Lead Director position has become common. In CAP’s annual survey of director compensation at the 100 largest U.S. public companies, the percentage of companies with a Lead Director increased from 38% to 47% in three years, from 2009 to 2011. The percentage of companies reporting a separate non-executive Chair has stayed more stable over the period, at approximately 20%. (In public companies where there is not an independent non-executive Chair or Lead Director, there will be an independent Presiding Director, at times a rotating position.)

When determining the appropriate Board leadership structure, directors must consider which structure will be optimal for their company and its culture. If a Lead Director or a separate Chair is elected, it is essential that the separate roles are clearly defined. This will allow the Board to work more effectively with the CEO and other members of the management team, as well as to best determine the appropriate compensation for the role.

Typical Responsibilities of Various Board Leadership Roles

Typical responsibilities are summarized below. As the typical responsibilities and related time commitment can vary substantially, so does the typical compensation for each role.

|

Role |

Responsibilities |

|

Executive Chair |

Provides counsel to the CEO on organization structure, financial structure and related topics Plays integral part in strengthening relationships with external stakeholders, including shareholders and regulatory bodies Develops and executes the company strategy with the CEO |

|

Non-Executive Chair |

Takes primary responsibility for shaping Board agendas, with input from the CEO Facilitates discussions between independent directors on key issues outside of Board meetings Has a critical role in succession planning May represent the organization to external stakeholders and employees (at the board’s discretion) Does not typically have a direct role in the company’s operations |

|

Lead Director |

Chairs executive sessions of the Board Works with the Chairman & CEO to set agendas for Board meetings Serves as liaison between the Board and the CEO Facilitates discussions between independent directors on key issues outside of Board meetings Does not typically represent the company to external stakeholders Does not typically have a role in the company’s operations |

Executive Chairman

The role of Executive Chair is often viewed as a transitional role. The role’s influence on the business can vary dramatically from company to company. As such, compensation practices vary widely across companies and will reflect each company’s specific circumstances, including:

- Balance of responsibilities between the CEO and the Executive Chair

- Time commitment/involvement (e.g., 1 vs. 3 days per week)

- Expected tenure of the Executive Chair

- Tenure and experience of the CEO

- Equity ownership – equity grants are less likely if the Executive Chair already has a large ownership stake or if the position is viewed as short-term in nature

- Founder vs. non-founder status

For an Executive Chair, compensation levels often reflect the individual’s prior pay package as CEO, as well as the compensation program and pay levels of the current CEO.

- Typical pay elements include base salary, annual bonus opportunity and long-term incentive awards

- Base salary levels may reflect the salary earned in the individual’s prior position. If the time commitment is reduced, a salary reduction may also apply

- Long-term incentive opportunities of an Executive Chair are normally lower than what the CEO receives

- Long-term incentive vehicles granted may vary from the company’s core executive compensation program, due in part to the expectation of a shorter tenure and less ability/time to impact long-term results

CAP consultants reviewed compensation data among 57 general industry companies with an Executive Chair, comparing Executive Chair pay to that of the CEO. We found that, at median, Executive Chair compensation (including salary, bonus and long-term incentives) was approximately 70% of the CEO’s compensation.

|

2012 Executive Chair Data |

Exec Chair Salary |

Exec Chair TCC |

Exec Chair TDC |

||||||

|

25th |

Median |

75th |

25th |

Median |

75th |

25th |

Median |

75th |

|

|

57 General Industry Cos. (Median Revenues of $2.4B) |

70% |

90% |

100% |

65% |

85% |

105% |

35% |

70% |

100% |

For reference, below is a breakout of the pay package for three recent, high profile Executive Chairs.

|

Recent Executive Chairman Compensation Packages at Large Organizations |

|||

|

Company |

Hewlett-Packard |

Kraft Foods Inc. |

Sara Lee |

|

Revenue |

$127.2B |

$54.3B |

$8.7B |

|

Executive Chairman |

Raymond J. Lane |

John T. Cahill |

Jan Bennink |

|

Date Hired as Executive Chairman |

September 2011 |

January 2012 |

January 2011 |

|

Previous Role |

Non-Executive Chair |

Outside / New Hire |

Non-Employee Director |

|

Base Salary |

None |

$0.75M |

$1.00M |

|

Target Bonus |

None |

$0.75M (100% of base) |

$1.75M (175% of base) |

|

Long-Term Incentives |

$8.44M (1) |

$4.50M |

$5.25M |

|

Target Total Direct Compensation (TDC) |

$8.44M |

$6.00M |

$8.00M |

|

TDC as a % of CEO |

46% |

97% |

129% |

|

LTI Award Vehicle LTI Grant Frequency (annual, one-time) |

20% Time-Based Stock Options 80% Performance-Based Stock Options One-Time(2) |

75% RSUs 25% Stock Options Not disclosed |

50% RSUs 50% Stock Options Not disclosed |

|

Vesting |

Time-Based: 3 Year Ratable Vesting Performance-Based: Requires 120-140% price appreciation |

3 Year Cliff Vesting (RS) 3 Year Ratable Vesting (SO) |

2 Year Cliff Vesting |

|

LTI Award Vehicles Different from Executive LTI Program |

Yes |

Yes |

Yes |

- Excludes fees as non-executive Chair, including $2.19M RSU award

- 1M stock options were awarded (200,000 options with 3-year ratable vesting; 400,000 options vest upon stock price appreciation of 120% from grant price; 400,000 options vest upon stock price appreciation of 140% from grant price).

Non-Executive Chairman / Lead Director Compensation

Compensation packages for non-executive Chairs and Lead Directors typically consist of the core compensation program for non-employee directors along with an additional stipend (or premium) that reflects the responsibilities and time commitment of the role. This approach appropriately recognizes the differential between a leadership position and other directors, with the magnitude of the premium reflecting the additional responsibilities.

CAP’s market data indicates that all companies with a non-executive Chair provide a premium for the role, and 69% of companies provide a pay premium for the Lead Director role.

Non-executive Chair pay is typically delivered in one of two ways:

- An additional retainer paid in cash or stock, in addition to the regular outside director pay program

- A separate fixed dollar amount provided in cash, stock or a combination, in lieu of the regular outside director pay program

As indicated below, the premium provided to a Lead Director is often much smaller than the premium provided to a non-executive Chair. Our data indicates that a non-executive Chair receives a median premium of +65% compared to a regular outside director’s package. For a Lead Director, the median premium is +10%.

|

Non-Executive Chairman and Lead Director Premium Compensation General Industry Companies with Median Revenues of $2.3B |

|||||

|

Leadership Position |

No of Cos. |

Prevalence of Cos. Providing Additional Compensation |

Multiple of Non-Employee Director Compensation (Median) Primary Reference |

Additional Premium – Median |

Additional Premium – Range |

|

Non-Executive Chairman |

42 |

100% |

1.65x |

$100,000 |

$20k – $577K |

|

Lead Director |

114 |

69% |

1.10x |

$20,000 |

$5K – $140K |

Conclusions

The structure and amount of compensation paid to Executive Chairs differ from non-executive Chairs and Lead Directors, a direct reflection of the roles, duties and time commitment required for each position.

Executive Chairs participate in the company’s executive compensation programs. Base salary, annual incentive and long-term incentives are commonly offered, yet pay programs are situation-specific and frequently transitional in nature. The Executive Chair’s expected tenure and perceived ability to influence longer term results are considerations that impact the amount and form of incentive compensation used.

As companies increasingly focus on improving Board independence, it will be important to evaluate whether or not separate Chair and CEO roles are appropriate. Companies should assess which organization structure makes sense given its unique circumstances. Companies anticipating a transition period due to executive turnover, the need to improve governance or a corporate transaction should re-assess the appropriate structure necessary to best navigate through turbulent times.

For the 114 company sample, median revenue was $30B, median market capitalization was $29B and median Total Shareholder Return (TSR) was 3% for 2011.

What We Found

Companies have modified their stock ownership guidelines and stock retention (or holding) requirements to enhance their governance practices. Median value of CEO stock ownership guideline has increased to 6x base salary, also more in line with Institutional Shareholder Services’ (ISS) definition of “robust” stock ownership. Overall, the use of stock retention requirements increased to approximately 1/3 of companies, while the use of stock retention requirements alone is flat year over year.

Prevalence Of Stock Ownership Guidelines And Stock Retention Requirements

The prevalence of stock ownership guidelines (approximately 90%) among companies in our database remained relatively flat in 2011 compared to findings in 2010. Companies with both stock ownership guidelines and stock retention requirements increased to 36% (from 22%), demonstrating increased efforts towards good corporate governance. However the prevalence of companies with stock retention requirements only stayed relatively flat year over year at 4%.

Of the 46 companies with stock retention requirements, nearly half (52%) of the companies report retention requirements that are linked to stock ownership guidelines (e.g., companies must hold shares until the stock ownership guideline level is achieved). Companies with stand-alone stock retention requirements that are not linked to stock ownership guidelines decreased slightly to 48% in 2011 (vs. 57% in 2010).

Stock Ownership Requirement

Similar to 2010, most companies (approximately 80%) express stock ownership guidelines as a multiple of salary and 15% express guidelines as a fixed number of shares. Fixed share guidelines are more prevalent in the Financial Services (57%), Technology (31%) and Retail (27%) industries.

|

CEO Stock Ownership Requirement Prevalence |

2011 (n = 104) |

2010 (n = 99) |

||

|

# of Cos |

% of Cos |

# of Cos |

% of Cos |

|

|

Multiple of Salary |

84 |

81% |

80 |

81% |

|

Fixed Shares |

15 |

14% |

15 |

15% |

|

Lesser Of Approach |

3 |

3% |

2 |

2% |

|

Other |

2 |

2% |

2 |

2% |

Stock ownership guidelines for CEOs increased from 2010, with the median CEO requirement increasing from a 5x multiple of salary to 6x salary in 2011 (See chart below for details). The median fixed share guideline also increased to 175,000 shares from 150,000 shares in 2010. This median requirement suggests that companies may be increasing their guidelines to respond to shareholders and provide more favorable optics. For several industries, however, (i.e., Automotive, Financial Services, Healthcare and Retail) the median CEO stock ownership guidelines of 5x salary was the same year over year.

The median stock ownership requirement value for the CEO increased modestly to $7.0M in 2011.

|

CEO Stock Ownership Requirement |

2011 (n=104) |

2010 (n=99) |

||||

|

25th %ile |

50th %ile |

75th %ile |

25th %ile |

50th %ile |

75th %ile |

|

|

Multiple of Salary |

5x |

6x |

6x |

5x |

5x |

6x |

|

Fixed Shares |

120,000 |

175,000 |

300,000 |

100,000 |

150,000 |

300,000 |

|

Total Value |

$5.7M |

$7.0M |

$9.7M |

$5.4M |

$6.7M |

$8.6M |

Most companies require executives to achieve the guideline requirement within 5 years. 20% of companies in our database disclose a penalty for not achieving the required ownership. Common penalties for non-compliance include restrictions on selling shares, requiring annual bonus or performance cash awards to be paid in shares and reducing future total compensation.

74 of 104 companies disclose the type of shares that count toward the guideline. While approximately 40% of companies count unvested restricted stock toward the requirement, less than 10% of companies count unearned performance shares or unvested stock options. These findings are similar to our findings in 2010.

|

Shares Counting Toward Guideline Requirement |

2011 (n = 104) |

2010 (n = 99) |

||

|

# of Cos |

% of Cos |

# of Cos |

% of Cos |

|

|

Shares directly owned |

72 |

69% |

55 |

56% |

|

Shares in 401(k) plan |

49 |

47% |

33 |

33% |

|

Unvested RS |

43 |

41% |

33 |

33% |

|

Shares indirectly owned |

36 |

35% |

29 |

29% |

|

Deferred Compensation |

33 |

32% |

25 |

25% |

|

Vested but unexercised options |

11 |

11% |

6 |

6% |

|

Unearned performance shares |

7 |

7% |

5 |

5% |

|

Unvested options |

5 |

5% |

1 |

1% |

|

Not disclosed |

30 |

29% |

29 |

29% |

Note: Percentages add up to greater than 100% due to multiple types of equity counted by various companies.

Stock Retention Requirement

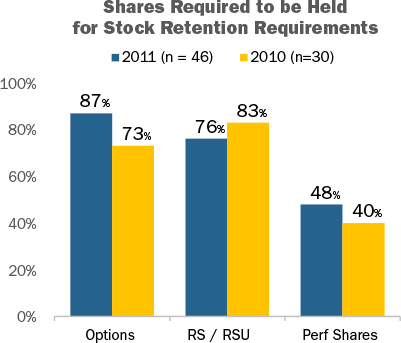

Companies with stock retention requirements most often require executives to hold net shares from option exercises or restricted stock share/unit vesting. Fewer companies, less than 50%, subject net shares from performance-based equity awards to stock retention requirements.

Note: Percentages add up to greater than 100% due to some companies requiring that multiple forms of equity be held.

Most companies require executives to hold net shares after exercise or vesting for a period of 1 year (41%) or through retirement (25%). Few companies require executives to hold shares post-retirement (13%), although the prevalence has increased from 2010.

|

Period Subject |

2011 (n = 32) |

2010 (n = 24) |

||

|

# of Cos |

% of Cos |

# of Cos |

% of Cos |

|

|

1 year post exercise/vest |

13 |

41% |

11 |

46% |

|

2 years post exercise/vest |

1 |

3% |

1 |

4% |

|

Retirement |

8 |

25% |

8 |

33% |

|

Post-retirement |

4 |

13% |

1 |

4% |

|

Other |

4 |

13% |

4 |

17% |

|

Not disclosed |

3 |

9% |

1 |

4% |

Note: Reflects companies with stock retention requirement only. Percentages add up to greater than 100% due to one company requiring different holding periods for CEO and other NEOs.

Disclosed Stock Ownership Guideline Changes

Approximately 20% of companies disclose changes to their stock ownership guideline requirements for 2011 or for 2012. A majority of these companies (55%) increased the ownership requirement for at least one NEO. Other notable changes include the addition of retention requirements (32%) and requiring a more stringent definition of shares that count toward the stock ownership guideline (9%).

|

Changes to Stock Ownership Guidelines |

2011 (n = 22) |

2010 (n = 25) |

||

|

# of Cos |

% of Cos |

# of Cos |

% of Cos |

|

|

Increased guideline requirement |

12 |

55% |

12 |

48% |

|

Added holding requirement |

7 |

32% |

6 |

24% |

|

Modified shares counting toward guideline |

2 |

9% |

n/a |

n/a |

|

Modified penalty for non-compliance |

1 |

5% |

5 |

20% |

|

Newly adopted |

1 |

5% |

1 |

4% |

|

Adopted mandatory holding of shares through retirement |

1 |

5% |

1 |

4% |

|

Extended Participation |

1 |

5% |

n/a |

n/a |

|

Decreased guideline requirement |

1 |

5% |

n/a |

n/a |

Note: Percentages add up to greater than 100% due to multiple changes by several companies.

Summary

In 2011, companies made modest changes to their stock ownership guideline requirements; most often in an effort to make them more robust. Additionally, companies continue to implement stock retention requirements, albeit at a relatively slow pace, to enhance their governance practices. We expect companies to continue to adopt and implement stock retention (holding) requirements and to increase their stock ownership guidelines. Both of these policies address issues that are important to shareholders and proxy advisory groups, and further align senior executives with shareholders.

Companies have modified their stock ownership guidelines and stock retention (or holding) requirements to enhance their governance practices.

While approximately 40% of companies count unvested restricted stock toward the requirement, less than 10% of companies count unearned performance shares or unvested stock options. These findings are similar to our findings in 2010.

In 2011, companies made modest changes to their stock ownership guideline requirements; most often in an effort to make them more robust. We expect companies to continue to adopt and implement stock retention (holding) requirements and to increase their stock ownership guidelines.

In January, 2013, Institutional Shareholder Services (ISS) made two announcements of note related to executive compensation

- Realizable Pay: Updated the Evaluating Pay for Performance document to provide a detailed description of its methodology for calculating realizable pay

- QuickScore: Rolled out QuickScore as a replacement for its GRId score

Realizable Pay

For S&P 500 CEOs at companies with an annual meeting after February 1, 2013, the standard ISS research report will show three-year total realizable pay in addition to the three-year total grant date pay that is used in its quantitative analysis. If a company’s quantitative test results in a medium or high level of concern, ISS will discuss realizable pay levels vs. grant date pay as a part of the qualitative review. If realizable pay is significantly lower than grant date pay, it could be a potential indicator that the actual pay-for-performance relationship is more aligned than the quantitative analysis indicates. Conversely, if realizable pay is greater than grant date pay in a company whose quantitative analysis results in a medium or high level of concern, it may aggravate concerns about the pay for performance alignment. Although there are still some limitations to realizable pay analysis (discussed further below), we believe that, on an overall basis, this brings ISS’ analysis one step closer to assessing the true pay-for-performance relationship.

|

ISS methodology for total realized pay is to include all of the following (typically for the three-year period): |

||

|

Compensation Element |

ISS Approach |

CAP Perspective |

|

Base Salary |

As reported for all three years |

We support this approach |

|

Bonus / Short-term Non-Equity Incentives |

As reported for all three years |

We support this approach as it reflects what was actually earned |

|

Long-term Cash |

The earned value of the award (if earned during the same measurement period) or its target value in the case of on-going award cycles (i.e., not completed before the end of the measurement period) |

|

|

Share-based Awards |

The value (based on stock price as of the end of the measurement period) of awards made during the period (less any shares/units forfeited due to failure to meet performance criteria based on complete and clear disclosure); or, if performance awards remain on-going, the target level of such awards |

|

|

Stock Options |

The net value realized with respect to such granted options which were also exercised during the period; for options granted but not exercised during the measurement period, ISS will re-calculate the option value, using the Black-Scholes option pricing model, as of the end of the measurement period |

|

|

Change in Pension Value and Nonqualified Deferred Compensation Earnings |

As reported for all years |

|

CAP Perspective Almost any definition of realizable pay will be subject to criticism and scrutiny. Our main concern with the realizable pay approach proposed by ISS is that it is not directly connected to a review of the firm’s performance over the time period. Comparing realizable pay to grant date pay may be an indicator of the pay for performance relationship, but it is our position that it would be better viewed next to multiple years of performance relative to peers. We suspect that over time ISS will refine how realized pay is defined and could directly incorporate it into the pay-for-performance quantitative test.

ISS notes that it is their intent to collect the required information in a standardized way that is easily obtained from a company’s tabular disclosure. Companies can help improve the accuracy of ISS’ analysis by clearly revealing, in a supplemental table, any performance based awards that have been forfeited prior to the completion of ISS’ assessment period (i.e., most recent three years).

ISS QuickScore

On January 25th, ISS rolled out QuickScore as a replacement of its GRId score. It will apply a scoring system based on the decile ranking of a company relative to others in the respective country.

- Coverage: 3,000 largest U.S. public companies

- Methodology: The scoring will be applied over the same four quadrants used for the GRId score, with several subcategories in each quadrant

|

Categories for the Quickscore |

|||

|

Board Structure |

Compensation/Remuneration |

Shareholder Rights |

Audit Practices |

|

|

|

|

- Screening Process:Assesses companies based on multiple qualitative factors to see if they exceed, meet, or fall short of market practices

- Quantitatively assessed correlation between 16 performance and risk factors

- Factor Criteria: Provides red flag summary of practices that raised concern and green stars for practices that mitigate concern

- Data Verification: Companies have the ability to verify their data between January 28th and February 15th. When the product launches, companies will once again be able to verify their data

CAP Perspective: The structure and criteria of the QuickScore appear very similar to what was used under the GRId score. The main change appears to be the relative scoring approach, which should provide a better indicator of governance risk compared to other companies

Conclusion

While ISS’ evaluation criteria are always challenging for companies to address, the changes made to the ISS pay-for-performance evaluation and the transition from GRId to QuickScore represent directional improvement. We expect that the calculation of realizable pay and its role in the pay for performance evaluation will continue to evolve over time. Similar to GRId, it is not clear what role QuickScore will play in shareholder voting decisions. We expect that it will be a starting point for deeper analysis in cases where the score indicates governance concern.

We are pleased to present the 3nd annual report on non-employee director (NED) compensation produced by Compensation Advisory Partners LLC (CAP). The report provides a review of current director pay practices among the largest public U.S. corporations (trend setting organizations) and Observations regarding trends and outlook.

- Evaluation of Executive Pay (Management Say on Pay)

- Incorporate a company’s selected peers as an input to its peer group selection methodology, while maintaining an approach that includes company size and market capitalization constraints

- Potentially incorporate a comparison of realized pay to grant date pay as part of the qualitative evaluation of pay-for-performance alignment

- Voting on Golden Parachutes in an Acquisition, Merger, Consolidation, or Proposed Sale

- Include existing change in control arrangements maintained with named executive officers rather than focusing only on new or extended agreements

- Place further scrutiny on multiple legacy problematic features in change in control agreements

- Pledging

- Identify significant pledging as a failure of risk oversight with a negative vote recommendation directed against the board of directors

Below CAP summarizes the key policy changes and we also provide perspective on the key implications for companies to consider.

Current Peer Group Selection Process for Pay-for-Performance Evaluation

For 2012, ISS selected the subject company’s peer group using market cap and revenue (or assets for financial firms) and the subject company’s GICS industry group. The peer group is generally comprised of 14-24 companies that are closest to the subject company, and where the subject company is close to median of the peer group in revenue/asset size.

Updated Peer Group Selection Process for Pay-for-Performance Evaluation

For 2013, ISS revised the peer group selection process to include companies in GICS industry groups represented in the subject company’s self-selected peer group. The size parameters used in the selection process continue to include market cap and revenue, though assets will be used for certain financial firms. ISS will consider the subject company’s GICS industry group as well as the GICS industry group(s) of companies within the subject company’s self-selected peer group. The peer group continues to generally include 14-24 companies and is designed to emphasize peers that are closest to the subject company in terms of revenue/asset size and industry, are in the subject company’s peer group and have chosen the subject company as a peer. Selected peer companies will also remain within the company’s market cap bucket.

ISS will also use slightly relaxed size constraints, especially at very small and very large companies. For certain financial firms, revenues will be used instead of assets for screening.

ISS Intent and Impact

The new approach incorporates the subject company’s GICS industry group as well as additional GICS industry group(s) represented in the company’s self-selected pay benchmarking peer group. This change was intended to identify and prioritize GICS industry groups beyond the subject company’s GICS industry. Backtesting of the new vs. old methodology indicates that this change will result in a greater degree of overlap between the ISS peer group and the subject company’s self-selected peer group. This revision will not impact the size comparison of the subject company relative to the selected peer group since size revenue/asset and market cap size constraints will be maintained.

CAP Perspective: ISS’ peer group revisions address the criticism that the current “one size fits all” approach to the peer group selection process does not accurately take into account a company’s business model and company-specific considerations. Without taking into consideration the company’s self-selected (and Board approved) peer group, ISS’ current process has limitations and lacks credibility.

The revised approach provides greater alignment between ISS’ peer group and the company’s self-selected peer group. We expect companies and Compensation Committee to find the revised peer groups to be more credible due to the stronger emphasis on the relevance of the company’s business model. In addition, the revised peer groups are more likely to take into account the companies used for compensation benchmarking purposes.

Current Pay-for-Performance Evaluation

The approach for 2012 included quantitative and qualitative components. The quantitative analysis reviews three factors for companies in the Russell 3000 index:

- The degree of alignment between the company’s TSR rank and the CEO’s total pay rank within the peer group, as measured over one-year and three-year periods (weighted 40/60, to put more emphasis on the longer term)

- The multiple of the CEO’s total pay relative to the peer group median

- Alignment between the trend in the CEO’s pay and the company’s TSR over the prior five fiscal years – i.e., the difference between the trend in annual pay changes and the trend in annualized TSR changes during the prior 5-year period

Relative Peer Group Alignment –

Absolute Alignment – this factor measures long-term alignment between pay and company performance, as:

If ISS determines that these analyses demonstrate a weak alignment between pay and performance, ISS will conduct a qualitative review before issuing a final vote recommendation.

Considerations for the qualitative review include:

- The ratio of performance- to time-based equity awards

- The ratio of performance-based compensation to overall compensation

- The completeness of disclosure and rigor of performance goals

- The company’s peer group benchmarking practices

- Actual results of financial/operational metrics, such as growth in revenue, profit, cash flow, etc., both absolute and relative to peers

- Special circumstances related to, for example, a new CEO in the prior FY or anomalous equity grant practices (e.g., biannual awards)

- Any other factors deemed relevant

Updated Pay-for-Performance Evaluation

The pay-for-performance evaluation for 2013 continues to include a quantitative and qualitative component. The three quantitative tests remain unchanged from 2012 although the tests will be performed using the revised peer group described above.

ISS will continue to conduct a qualitative review for companies that demonstrate a weak alignment between pay and performance. The considerations incorporated in the qualitative review for 2013 remain the same as 2012 with the addition of a comparison of realizable pay to grant pay for large cap companies.

Realizable pay will consist of relevant cash and equity-based grants and awards made during a specified period being measured. Equity award values are based on actual earned awards, or target values for ongoing awards, calculated using a stock price at the end of the performance measurement period. Stock options or stock appreciation rights (SARs) will be re-evaluated using the remaining term and updated assumptions, using a Black-Scholes option pricing model.

ISS Intent and Impact

ISS’ revision to potentially incorporate a comparison of realizable pay to grant date pay as part of the qualitative evaluation, when necessary, for large cap companies provides an additional perspective for assessing the pay-for-performance alignment between CEO compensation and company performance. This new factor may either increase or reduce the pay-for-performance concerns identified through the quantitative component of the pay for performance review. Large cap companies will likely be defined as the S&P 500 or a similar group.

CAP Perspective: ISS’ inclusion of realizable pay provides a critical perspective on CEO compensation. If the CEO’s compensation creates a pay-for-performance misalignment, it is important to understand the total value the CEO may be able to realize over a specific performance period or at a given time. We believe this assessment will provide additional context for CEO compensation decisions.

ISS’ final 2013 policy summary is silent on whether the realizable pay will be compared to the ISS peer group or company’s financial performance. An ISS representative indicated that realizable pay will be compared to grant date pay, but not to peer companies. In isolation from financial performance or a relative peer analysis, assessing the CEO’s realizable pay vs. actual compensation has its limitations and does not provide sufficient context for the company’sspecific situation.

One problem with ISS’ definition of realizable pay is that outstanding stock options will be valued using a Black-Scholes model rather than intrinsic value. As a result, a portion of the so-called realizable pay may never be realized, if options are underwater.

Voting on Golden Parachutes in an Acquisition, Merger, Consolidation, or Proposed Sale

Current Recommendation

ISS will vote on a case-by-case basis on proposals to approve the company’s golden parachute compensation, consistent with policies on problematic pay practices related to severance packages. Features that may lead to a vote against include:

- Recently adopted or materially amended agreements that include excise tax gross-up provisions (since prior annual meeting);

- Recently adopted or materially amended agreements that include modified single triggers (since prior annual meeting);

- Single trigger payments that will happen immediately upon a change in control, including cash payment and such items as the acceleration of performance-based equity despite the failure to achieve performance measures;

- Single-trigger vesting of equity based on a definition of change in control that requires only shareholder approval of the transaction (rather than consummation);

- Potentially excessive severance payments;

- Recent amendments or other changes that may make packages so attractive as to influence merger agreements that may not be in the best interests of shareholders;

- In the case of a substantial gross-up from pre-existing/grandfathered contract: the element that triggered the gross-up (i.e., option mega-grants at low point in stock price, unusual or outsized payments in cash or equity made or negotiated prior to the merger); or

- The company’s assertion that a proposed transaction is conditioned on shareholder approval of the golden parachute advisory vote. ISS would view this as problematic from a corporate governance perspective.

New Recommendation

For 2013, ISS revised the features that may lead to a vote against the company’s golden parachute compensation to include consideration of existing change in control arrangements maintained with named executive officers, rather than focusing only on new or extended arrangement.

ISS will scrutinize multiple legacy problematic features in change in control agreements and may recommend against the proposal if agreements include one or more of the following, depending on the number, magnitude, and/or timing of issue(s):

- Single- or modified-single-trigger cash severance;

- Single-trigger acceleration of unvested equity awards;

- Excessive cash severance (>3x base salary and bonus);

- Excise tax gross-ups triggered and payable (as opposed to a provision to provide excise tax gross-ups);

- Excessive golden parachute payments (on an absolute basis or as a percentage of transaction equity value); or

- Recent amendments that incorporate any problematic features (such as those above) or recent actions (such as extraordinary equity grants) that may make packages so attractive as to influence merger agreements that may not be in the best interests of shareholders; or

- The company’s assertion that a proposed transaction is conditioned on shareholder approval of the golden parachute advisory vote.

Recently adopted or materially amended agreements that include problematic practices will tend to carry more weight on the overall analysis. However, ISS will closely scrutinize the presence of multiple legacy problematic features.

ISS Intent and Impact

ISS’ revised voting recommendations puts additional pressure on boards of directors and companies to revisit existing contractual obligations. Clearly companies are not able to simply walk away from their obligations, but there may be me greater appetite to renegotiate this arrangement.

The biggest change to the list of problematic practices is the addition of single-trigger acceleration of unvested equity awards. This practice is widespread, even though a number of companies have moved to double trigger vesting.

We look forward to understanding how ISS will define an “excessive” golden parachute going forward.

CAP Perspective: ISS’ revised policies place increasing pressure on companies to make changes to existing contracts with problematic features. ISS’ stringent point of view on single-trigger acceleration of unvested equity awards will likely have an impact on contracts with this provision over time. The pressure to eliminate certain problematic provisions will be stronger for companies that are moving towards a corporate transaction.

Pledging

ISS’ proposed draft policy on the practice of pledging company stock as a problematic pay practice under ISS’ say-on-pay evaluation was viewed negatively by issuers. ISS indicated that discussions with investors led it to conclude that significant pledging is problematic and represents a failure of risk oversight. ISS concluded that the potential negative vote recommendation should be directed towards the election of directors rather than to a company’s say-on-pay proposal.

For 2013, ISS will view pledging on a case-by-case basis to determine whether the pledging rises to a level of serious concern for shareholders. ISS is viewing significant pledging as a failure of risk oversight whereby directors should be held accountable (rather than communicating concern through a say-on-pay recommendation). To determine the vote recommendation for directors, at companies with pledging policies, the following should be considered:

- Presence in the company’s proxy statement of an antipledging policy that prohibits future pledging activity;

- Magnitude of aggregate pledged shares in terms of total common shares outstanding or market value or trading volume;

- Disclosure of progress or lack thereof in reducing the magnitude of aggregate pledged shares over time;

- Disclosure in the proxy statement that stock ownership and holding requirements do not include pledged company stock; and

- Any other relevant factors.

ISS also indicated that any hedging will result in a negative voting recommendation on the election of directors. Hedging includes a variety of strategies used to reduce or eliminate the impact of stock price declines, including puts, covered calls, collars or other derivative transactions.

ISS Intent and Impact

ISS 2013 policy on pledging places pressure on companies to monitor and unwind situations where pledging rises to a level of serious concern for shareholders. ISS is silent on the definition of “significant” pledging, however, ISS indicates that significant pledging may have an impact on the vote recommendations for the election of directors.

CAP Perspective: Pledging provides flexibility by allowing executives access to lower cost financing without having to sell company stock to fund other purposes. It is important to provide balance between this greater flexibility and monitoring of excessive leverage. Excessive leverage is never a good thing and to the extent that executives do pledge shares certain safeguards should be in place.

Pledging causes concern for investors if the stock price could be impacted by an executive’s sale of the shares. In addition, issues may arise if a margin call forces a sale, particularly during a period where the trading window is closed. These concerns could be prevented by requiring the executive to attest that other liquid assets, unrelated to company stock, are readily available to satisfy any potential margin call. Stock ownership guidelines help to mitigate the compensation risk associated with pledging since it ensures that the executive remains invested in the company stock, even while pledging a portion of shares owned.