- Perquisites represent only a small portion of the total pay program for a CEO or CFO. However, perquisite based pay is – and we expect will continue to be – highly scrutinized

- In 2014 83% of companies provided perquisites to their CEO, and 81% of companies provided perquisites to their CFO

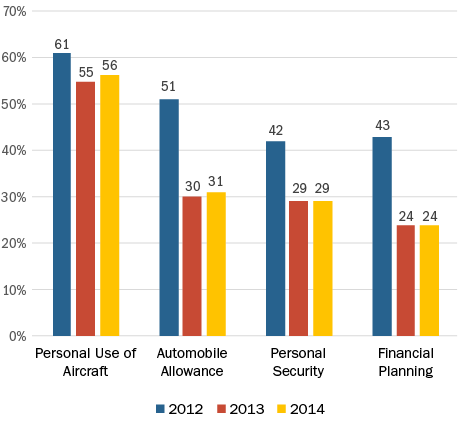

- The four most common CEO/CFO perquisites in 2014 were: personal use of corporate aircraft, auto allowance, personal security and financial planning

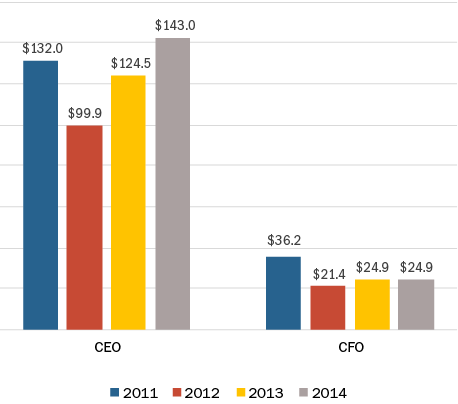

- The median value of total perquisites provided to CEOs increased by approximately 15% to $143,000 in 2014, and was flat at approximately $25,000 for CFOs

Our Survey Sample

Compensation Advisory Partners (“CAP”) reviewed 2015 proxy disclosures at a sample of 100 companies among the Fortune 500, representing nine industry groups. Industry groups included: Automotive, Consumer Goods, Financial Services, Health Care, Insurance, Manufacturing, Pharmaceutical, Retail, and Technology. For the companies studied, the median revenue size and market capitalization was $34 billion and $56 billion respectively.

What We Found

The percentage of companies in our research sample providing perquisites to their CEO stayed constant at 83% from 2013 to 2014. The percentage of companies providing perquisites to CFOs increased 5% from 2013 to 2014 to 81%.

In 2014, the four most common CEO perquisites were: personal use of corporate aircraft (56%), automobile allowance (31%), personal security (29%) and financial planning (24%). While the prevalence of personal use of corporate aircraft was generally flat from 2012 to 2014, the prevalence of automobile allowances, personal security and financial planning decreased sharply (approximately 30– 40%) over the past two years.

CEO Perquisite Prevalence

Although the prevalence of major perquisites remained steady in 2014 for CEOs compared to the prior year, the median total value for CEO perquisites increased 15% to $143,000. This value has ranged from $100,000 to $143,000 over the last four years. In contrast, the median value of perquisites for CFOs was relatively flat year-over-year, and has ranged from $21,000 to $36,000 since 2011.

Median CEO and CFO Perquisites Value ($000s)

Perquisites represent only a small portion of an executive’s total compensation, yet are often highly scrutinized. Shareholders prefer that pay be delivered in performance-based vehicles instead of through perquisites. Over the past few years, a number of companies changed their perquisite programs in reaction to increased shareholder scrutiny and specific feedback received from shareholders or proxy advisory firms. However, given fairly consistent prevalence over the past 2 years, data suggests that changes to company perquisite programs may have leveled off. PNC was the only company making a change to a perquisite program in our sample for 2014, increasing their annual perquisite limit from $10,000 to $20,000 for each NEO, other than for the CEO.

|

Perquisites Change Reported in CD&A |

2014 n=1 |

2013 n=7 |

2012 n=9 |

2011 n=14 |

||||

|

# of Cos. |

# of Cos. |

# of Cos. |

# of Cos. |

# of Cos. |

# of Cos. |

# of Cos. |

# of Cos. |

|

|

Eliminated perquisites |

0 |

0% |

6 |

75% |

2 |

22% |

9 |

56% |

|

Eliminated tax gross-ups on perquisites |

0 |

0% |

1 |

13% |

4 |

44% |

6 |

38% |

|

Reduced perquisite program/value |

0 |

0% |

1 |

13% |

2 |

22% |

1 |

6% |

|

Changed perquisite program |

1 |

100% |

0 |

0% |

1 |

11% |

0 |

0% |

Note: Percentages do not add up to 100% due to multiple changes by companies

Conclusion

While Compensation Committees continue to monitor the appropriateness (and competitiveness) of perquisite programs, as well as dollar values and overall executive usage, the degree to which executive perquisites are provided appears to have leveled off. We expect that companies will continue to closely align executive compensation with shareholder interests by limiting non-performance-based compensation, such as perquisites. We caution that any potential (perceived) misuse of executive perquisites will continue to raise the ire of shareholders and proxy advisory firms and provide for headline news.

Introduction

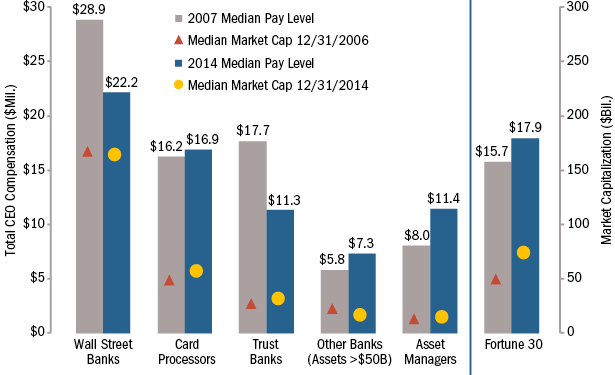

CAP set out to see if CEO pay levels among Wall Street Banks have returned to pre-crisis levels (i.e., 2007). In addition, we reviewed other financial sector firms1 to see how CEO pay levels have moved over the same time period. Hedge funds and private equity firms were not included in the review.

For reference, comparisons were also made to large non-bank companies across other industries ("Fortune 30"). In total, 65 companies were examined.

CEO Compensation – Highlights

- Wall Street CEO pay continues to exceed all other financial services companies studied; however, the gap between Wall Street Banks and other companies studied has narrowed significantly since 2007

- Pay levels for most Wall Street and Trust Bank CEOs have not returned to pre-crisis levels

- CEO pay among Asset Managers had the most significant increase, with median pay increasing 42% since 2007

- Regional Bank (assets >$50 billion) and Card Processor CEO pay exceeds pre-crisis levels

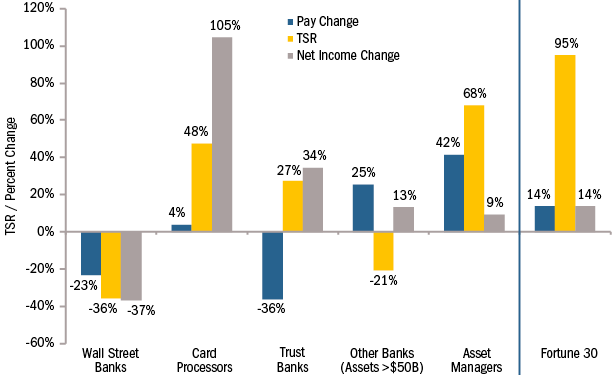

- From 2007 to 2014, changes in pay levels did not directly align with changes in stock price or Total Shareholder Return2 (“TSR”), with two exceptions. Asset Managers with strong stock appreciation also received significant growth in pay. Wall Street banks with decreases in stock price reported lower pay levels.

Current Pay Levels

As shown in Chart 1, CEO compensation at Wall Street Banks remains higher than other companies studied, however the differential has decreased since 2007. Wall Street Banks are also significantly larger than most of the other companies studied, in terms of market capitalization and net income.

Chart 1: Pay Levels vs. Company Size

Change in Compensation Since 2007

Have financial services companies returned to pre-crisis pay levels?

|

No |

|

|

Yes |

|

Chart 2: Pay vs. Performance

Conclusion

By 2014, most of the groups of companies studied have recovered from the financial crisis, as evidenced by increases in net income and TSR versus their 2007 results (Chart 2). It appears that companies have used restraint in making corresponding increases to CEO pay, recognizing that (1) shareholders sustained significant losses during the crisis, (2) material increases in pay should follow improved results for shareholders, and (3) public and regulatory scrutiny on financial company pay practices has been unrelenting.

As we look ahead, for both financial and non-financial firms, we expect continued sensitivity to executive pay levels, especially CEO pay levels. While companies have recouped losses from 2007, there will be ongoing pressure to demonstrate that CEO pay is aligned with performance, in terms of financial success and shareholder returns.

Appendix – Methodology

|

Item |

Definition |

|

Total Compensation |

Represents compensation as reported in Summary Compensation Table, excluding change in pension value and/or above market interest on non-qualified deferred compensation. For 2007 compensation, equity award values were taken from the Grants of Plan-Based Awards Table to consistently reflect the fair market value of equity awards granted in the year reviewed. |

|

Median |

Median was calculated for data sets with 5 or more companies. For data sets with less than 5 companies, average was used. |

|

Data Set |

Description |

|

Fortune 30 |

Includes the largest companies based on 2013 revenues, excluding any financial services companies, controlled companies, companies that were not public in 2007, or any companies that did not file a proxy statement between 9/1/2014 and 5/15/2015. AmerisourceBergen, Archer-Daniels-Midland, AT&T, Boeing, Cardinal Health, Chevron, Costco, CVS Health, Express Scripts, Exxon Mobil, Ford Motor, General Electric, General Motors, Hewlett-Packard, IBM, Kroger, Valero, Verizon, and Wal-Mart |

|

Wall Street Banks |

Bank of America, Citigroup, Goldman Sachs, JPMorgan Chase, and Morgan Stanley |

|

Card Processors |

American Express, Capital One, and Discover Financial |

|

Trust Banks |

BNY Mellon, Northern Trust, and State Street |

|

Other Banks |

All banks with assets greater than $50B, not listed above. BB&T, Comerica, Fifth Third, Huntington Bancshares, KeyCorp, M&T Bank, PNC, Regions Financial, SunTrust, U.S. Bancorp, Wells Fargo, and Zions |

|

Asset Managers |

10 largest Asset Managers by market capitalization on 12/31/2014. Affiliated Managers Group, BlackRock, Charles Schwab, Eaton Vance, Federated Investors, Franklin Resources, Invesco, Legg Mason, SEI Investments, T. Rowe Price (excludes Blackstone) |

1 Card Processors (that are also Bank Holding Companies), Trust Banks, Other Banks (with assets >$50B), and Asset Managers. For a complete list of companies in each category, see Appendix.

2 Stock price plus reinvested dividends.

Annually, Compensation Advisory Partners (CAP) evaluates pay levels for Chief Financial Officers (CFOs) and Chief Executive Officers (CEOs). This year’s analysis is based on a sample of 108 companies with median revenues of $12.4 billion. For more information on how we developed the sample of companies, please see below under Sample Screening Methodology.

Highlights

- Salary increases were provided much more frequently to CFOs, with approximately 70% receiving a salary increase, than to CEOs

- The median salary increase was only 0.3% for CEOs, while CFO salaries grew by 3.0%

- Similar to last year, the median increases in actual total direct compensation (i.e., cash plus equity) for both CEOs and CFOs, were in the low single-digits

- 2014 median increases in actual total direct compensation were 3.2% for CEOs and 5.2% for CFOs

- Slightly higher pay growth for CFOs was partially driven by higher annual bonus target opportunities in 2014

- On an absolute basis, CFO total compensation continues to approximate one-third of CEO total compensation

- Little or no changes observed in how long-term incentives are delivered to CEOs and CFOs; Long-term incentive mix continues to emphasize performance-based equity

Study Results

Salaries

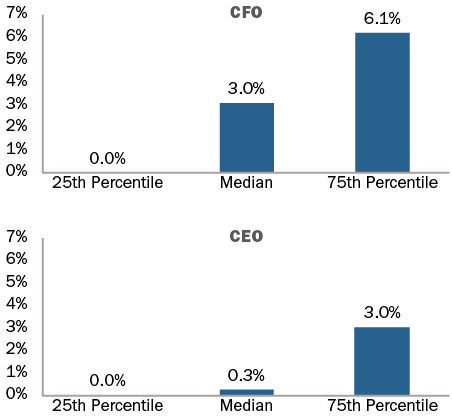

In the last 2 years, approximately 70% of CFOs received salary increases. The median salary increase for CFOs was 3.0% and the 75th percentile salary increase was 6.1%. In comparison, only about half of CEOs received salary increases. The median salary increase for CEOs was only 0.3% at median and the 75th percentile salary increase was 3.0%.

|

% of Executives Receiving Salary Increases |

||||

|

|

2012 – 2013 |

2013 – 2014 |

||

|

|

No Increase |

Receiving Increase |

No Increase |

Receiving Increase |

|

CEO |

52% |

48% |

49% |

51% |

|

CFO |

31% |

69% |

28% |

72% |

2014 Salary Increases

Actual Pay Levels

Our findings indicate a median rate of increase in actual total direct compensation levels for both CEOs and CFOs in the low-single digits. The median increases over the last two years ranged between 3% and 5%. During 2013-2014, actual total direct compensation (salary plus actual annual incentive plus the grant date value of long-term incentives) for CEOs and CFOs increased by 3.2% and 5.2%, respectively.

Industry Trends

2014 Median Salary Increase by Industry

2014 Median Actual Total Compensation Increase by Industry

|

Median Percentage Change in Pay Components |

||||

|

|

2012 – 2013 |

2013 – 2014 |

||

|

Pay Components |

CEO |

CFO |

CEO |

CFO |

|

Salary |

0% |

3.0% |

0.3% |

3.0% |

|

Actual Bonus |

4.1% |

3.7% |

4.3% |

7.8% |

|

Long-Term Incentives |

2.3% |

3.1% |

3.7% |

4.2% |

|

Actual Total Direct Compensation |

3.7% |

3.6% |

3.2% |

5.2% |

As seen in the table above, the median 2014 increase in actual bonus for CFOs was double the median increase for CEOs. This large increase in annual bonus is partially driven by higher bonus target opportunities in 2014 for CFOs, with the median target bonus increasing from 90% to 100% of salary. In contrast, CEO target bonus opportunities remained relatively flat at approximately 150% of salary.

|

Target Bonus as % of Salary |

||||

|

|

2013 |

2014 |

||

|

Pay Components |

CEO |

CFO |

CEO |

CFO |

|

25th Percentile |

125% |

75% |

125% |

80% |

|

Median |

147% |

90% |

150% |

100% |

|

75th Percentile |

170% |

100% |

165% |

105% |

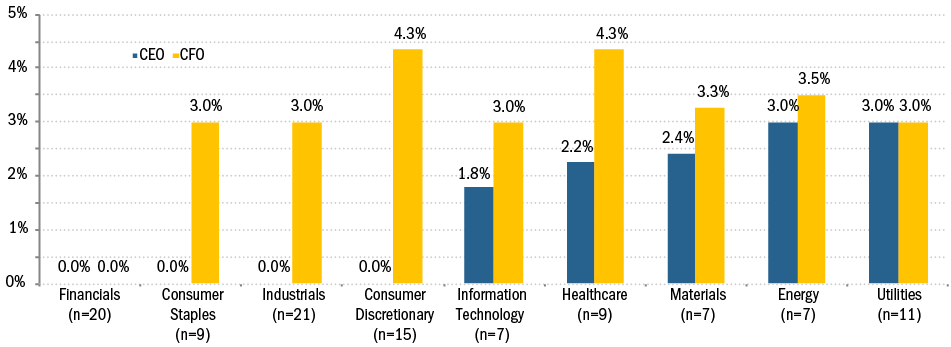

When analyzed by industry, median increases in salary for CEOs are generally less than 3%. Median salary increases to CFOs are much more robust, generally in the range of 3-4%. Median salary increases over 3% are seen for CFOs in the following industries: Consumer Discretionary, Energy, Healthcare, and Materials. The Financials industry is the only industry were the median change in salary was 0% for both CEOs and CFOs.

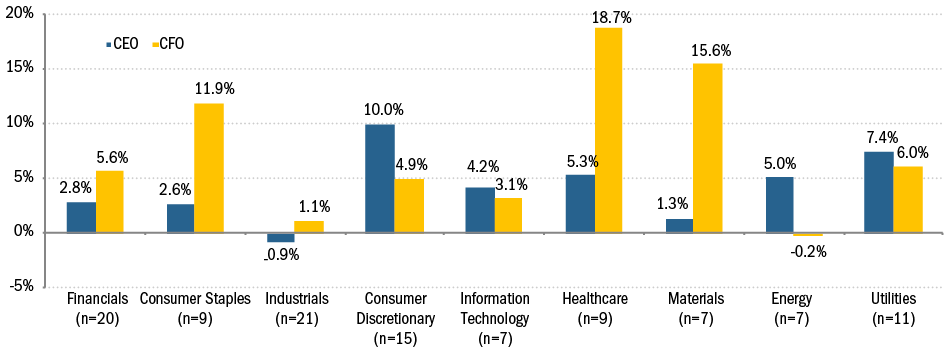

When we look at actual total direct compensation by industry, greater volatility is observed. The volatility in year-over-year changes is primarily driven by industry and company performance. Some of the largest increases in compensation levels are seen in Consumer Staples, Healthcare and Materials.

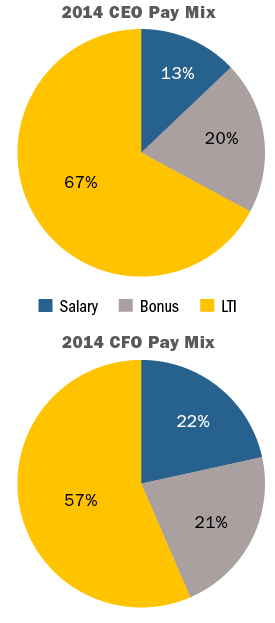

Target Pay Mix

The average total target compensation pay mix remained largely unchanged. At-risk pay continues to be more emphasized for CEOs than for CFOs.

Long-Term Incentive (LTI) Vehicle Prevalence and Mix

Equity mix and vehicles used for LTI awards remained fairly consistent for the past several years. The majority of companies continue to use two different vehicles to deliver long-term incentives to CEOs/CFOs and a quarter of companies studied use all three equity vehicles (time-based stock awards, awards under a performance plan, and stock options)

Performance plans account for roughly 50% of LTI awards, about 25% is delievered in stock options, and about 25% in time-vested restricted stock awards. The overall percentage of performance-based awards (performance plans and stock options) for both CEOs and CFOs continues to range between 75% – 80%.

|

LTI Mix |

||||

|

|

2013 |

2014 |

||

|

|

CEO |

CFO |

CEO |

CFO |

|

Stock Options |

27% |

27% |

26% |

25% |

|

Time Vested Restricted Stock |

17% |

22% |

21% |

26% |

|

Performance Plans |

56% |

51% |

53% |

49% |

Conclusion

In terms of performance, 2014 was a good year for our sample of companies with median total shareholder return of 15%, median revenue growth of 5% and median net income growth of 9%. We believe the 2014 pay changes were aligned with performance for the year. For CEOs, salary increases were modest, but increases in actual bonus and long-term incentives contributed to a median increase in actual total direct compensation of 3.2%. Pay progression opportunities for CFOs were even stronger, with a median increase of 7.8% in actual bonus and 4.2% in long-term incentives yielding a 5.2% median increase in actual total direct compensation.

In terms of compensation program design for senior executives, we saw relatively little change. The increase in annual target bonus opportunity for CFOs was noteworthy, but long-term incentives practices are similar to last year’s study. The increase in performance-based long-term incentives is significant and we expect this to remain the mainstream practice.

Sample Screening Methodology

Based on the screening criteria below, we arrived at a sample of 108 public companies with median 2014 revenue of $12.4B.

|

Revenue |

At least $5B in revenue for fiscal year 2014 |

|

Fiscal year-end |

Fiscal year-end between 9/1/2014 and 12/31/2014 |

|

Proxy Statement Filing Date |

Proxy statement filed before 3/31/2015 |

|

Tenure |

No change in CEO and CFO incumbents in the past three years |

|

Industry |

All industries have been considered for this analysis |

Highlights

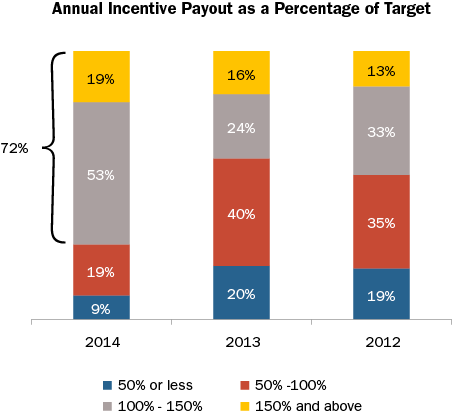

- Median increase of 15% in total compensation for CEOs delivered through both above target bonus payouts and higher long-term incentive awards (“LTI”)

- More companies are paying above target bonuses for 2014 performance. 72% of companies had a payout at or above target versus 40% and 46% of companies in 2013 and 2012, respectively

- Companies with higher bonus payouts demonstrated correspondingly higher levels of financial performance, including stronger top-line growth and greater profitability

- Companies continue to shift a greater portion of total LTI into a performance-based vehicle although time-based stock options and restricted stock remain prevalent

- Performance-based long-term vehicles represent the largest portion of LTI with many companies incorporating TSR as a metric

Total Compensation

Among Early Filers with CEOs who held their position for at least two years (37 companies), actual total compensation in 2014 increased 15% from 2013. The increase in total pay was delivered mostly through the annual and long-term incentive awards, with median increases of 18% and 14% increases year over year, respectively.

|

Compensation Element |

% Increase at Median |

|

Base Salary |

1.5% |

|

Annual Incentive |

18% |

|

Total Cash |

9% |

|

Long-Term Incentive (LTI) |

14% |

|

Total Compensation |

15% |

Base Salary

Among the Early Filers, companies continue to provide modest salary increases to the NEOs. Salary increases for incumbent CEOs ranged from 0 – 5%. Approximately 50% of companies did not increase their CEO's salary in 2014.

Annual Incentive Compensation

2014 was a strong financial year for the Early Filers, reflected in 8.8% EPS growth at median and 15% TSR for the year. This resulted in higher annual incentive payouts compared to both 2013 and 2012. 72% of companies had a payout at or above target versus 40% and 46% of companies in 2013 and 2012, respectively.

The companies that paid a bonus at or above target had stronger financial performance than both the S&P 500 and all Early Filers. Higher performance among companies with higher bonus payouts was evident in all three financial metrics examined, including Revenue growth, Pre-tax Income growth and EPS growth. For example, median EPS growth for these higher performers was 13.3% (versus 9.9% among the S&P 500 and 8.8% among all 50 Early Filers). Higher performance for companies with above target bonus payouts demonstrates that pay and performance is well-aligned. One-year TSR performance (as of February 2015) was similar across all groups.

|

Financial Metric |

Median 1-Yr Performance |

||

|

S&P 500 |

All Early Filers (n=50) |

Companies with at or above target payout (n=36) |

|

|

Revenue Growth |

5.2% |

5.7% |

6.4% |

|

Pre-Tax Income Growth |

8.3% |

6.2% |

9.7% |

|

EPS Growth |

9.9% |

8.8% |

13.3% |

|

TSR |

15.7% |

15.2% |

15.2% |

Median annual incentive payout as a percentage of target for all Early Filers was 111% in 2014 which was higher than the median in both 2013 and 2012.

|

Summary Statistics |

Annual Incentive Payout as a % of Target |

||

|

2014 |

2013 |

2012 |

|

|

75th Percentile |

136% |

116% |

130% |

|

Median |

111% |

94% |

100% |

|

25th Percentile |

99% |

75% |

72% |

Although 2014 was a strong year, companies are continually refining their annual incentive plan to ensure executive pay is aligned with performance. Among companies in our study, 34% made changes to the annual incentive plan with a majority of companies making changes to annual incentive metrics.

The chart below illustrates all changes companies made to their annual incentive plan:

|

Type of Change Reported |

Companies Reporting Changes (n = 17) |

|

|

# of Cos. |

% of Cos. |

|

|

Change in performance metrics used to fund awards |

12 |

71% |

|

Change in performance metric weighting / mix |

4 |

24% |

|

Increased target annual incentive award opportunity (CEO and/or CFO) |

4 |

24% |

|

Other |

4 |

24% |

Note: Percentages add to greater than 100% due to multiple changes by select companies.

Long-Term Incentive Compensation

The use of time-based LTI (stock options and restricted stock) continues to be prevalent, yet performance-based LTI continues to play the strongest role in the overall LTI mix.

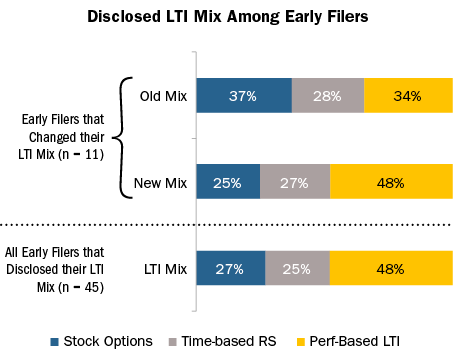

Approximately 50% of companies in our study made changes to their overall LTI program. Most changes involved the mix of vehicles, which continues the recent trend of increasing performance-based LTI and reducing the reliance on time-based long-term incentives. The table below indicates all changes made by the Early Filers:

|

Type of Change Reported |

Companies Reporting Changes (n = 26) |

|

|

# of Cos. |

% of Cos. |

|

|

Mix of LTI award vehicles |

11 |

42% |

|

Increased or reduced LTI award target opportunity level (CEO and/or CFO) |

8 |

31% |

|

Performance plan metric |

7 |

27% |

|

Add or eliminate LTI vehicle |

7 |

27% |

|

Vesting/performance period |

4 |

15% |

|

Other |

2 |

8% |

Note: Percentages add to greater than 100% due to multiple changes by select companies.

Among the companies that changed their LTI mix, most increased the emphasis on performance-based LTI while reducing stock option use. The portion of LTI awarded in the form of time-based restricted stock remained relatively unchanged. Overall, nearly 90% of companies use performance-based LTI, 74% use stock options and 62% use time-based restricted stock.

Among the Early Filers that grant performance-based LTI awards, approximately 60% use two or more metrics. The use of multiple metrics provides balance and rewards executives based on holistic performance.

Approximately two-third of companies use relative Total Shareholder Return ("TSR") as a performance metric. Companies incorporate TSR as a long-term incentive metric for multiple reasons including aligning with the shareholder experience, simplifying the goal-setting process and conforming to proxy advisory firms’ preference for TSR. Among the companies that use relative TSR as a standalone metric, it typically represents 25-50% of the total performance award. Some companies use financial performance (either absolute or relative) to fund the payout of the performance award and use relative TSR to modify the final payout, thereby incorporating it as an LTI metric but reducing its overall effect on payouts.

|

Weighting of TSR Metric in the LTI Plan (n = 28) |

Number of other LTI Metrics |

% of Companies |

|

25% |

1 – 2 |

11% |

|

50% |

1 |

29% |

|

Weighting not disclosed |

2 |

7% |

|

100% |

0 |

32% |

|

Modifier |

2 – 3 |

21% |

Say on Pay (SOP) Vote Results

In 2015, 98% of Early Filers that released SOP results this year received majority shareholder support; most companies (approximately 75%) received greater than 90% support. Compensation program design changes can and do improve Say on Pay results! Among the companies that made changes to either their annual or long-term incentive plan in 2014 (n = 29), 97% received majority shareholder support with approximately 70% receiving greater than 90% support. However, making a change to the incentive program design does not guarantee shareholder approval of the executive compensation program.

When fundamental problems with the compensation program exist – such as high pay levels or misalignment with performance – companies may fail the SOP vote. Additionally, poor SOP results can be attributed to shareholders expressing dissatisfaction with other aspects of the company’s business, its management or TSR performance.

Conclusion

2014 annual incentive payouts among the Early Filers were higher than 2013 which, when combined with the rise in LTI award levels, resulted in a 15% increase in total compensation. We saw a big increase in the number of companies with at or above target bonus payouts, as well as higher performance among these companies. Nearly 65% of companies use TSR as a long-term incentive metric, suggesting that companies are trying to enhance alignment between executive pay and shareholder experience.

Companies continue to make changes to their annual incentive and LTI plans, with a strong focus on enhancing the pay for performance relationship through modification of the annual incentive metrics and/or the long-term vehicle mix. Among companies that changed their LTI vehicle mix, they tended to increase the role of performance-based LTI. Our experience suggests these trends are consistent with the broader market practice. While changes to the incentive plan will likely lead to a favorable Say on Pay vote, companies should be aware of that other factors may affect the vote.

KEY TAKEAWAYS

- The use of performance-based long-term incentives (“LTI”) continues to be the prevailing practice, constituting more than 50% of the typical LTI program for Named Executive Officers (“NEO”)

- Companies have been re-examining the mix of components in their LTI program and actively increasing performance-based awards, while de-emphasizing stock options and time-based restricted stock

- While used to a lesser extent, stock options and time-based restricted stock continue to be part of the LTI program for many NEOs

- The most prevalent metrics used in performance-based LTI plans are return measures, such as ROI, Total Shareholder Return (“TSR”) and Earnings Per Share (“EPS”)

- Many companies have decided that the use of a two-pronged approach of measuring performance results against both internal goals and relative to the external market is a best practice

Compensation Advisory Partners (“CAP”) reviewed 2014 proxy disclosures for a 100 company subset of the Fortune 500 representing a cross-section of nine industry groups. The industry groups included: Automotive, Consumer Goods, Financial Services, Health Care, Insurance, Manufacturing, Pharmaceutical, Retail, and Technology. Our research examined changes in executive compensation practices in 2013, or indicated for 2014, and observations on current trends and pay program design. This CAPflash focuses on long-term incentive plan design and notable trends including changes made in 2013 or planned for 2014.

The companies included in this study have a median revenue size and market capitalization of $32B and $52B, respectively. The median total shareholder return was 43% for 2013.

TRENDS IN LONG-TERM INCENTIVE PLAN DESIGN

51% of companies in our study made changes to the LTI plan design in 2013 or for 2014. Companies continue to reduce the emphasis on time-based restricted stock and stock options and deliver a greater portion of LTI compensation in the form of performance-based equity or cash awards. Among companies that changed their LTI mix, most companies reduced the emphasis on stock options (71%) and/or increased the emphasis on performance-based LTI (67%). 33% of companies that changed the LTI mix reduced the emphasis on time-based restricted stock.

This continued shift towards performance-based LTI compensation reflects an effort by companies to respond to shareholder feedback and align executives’ pay with performance. Target Corporation, for example, responded to a number of shareholder comments calling for a greater link between pay and performance. In 2013, Target eliminated the use of stock options (which represented 75% of total LTI in 2012) in favor of a 100% performance-based LTI program.

The overarching priority for many companies is to use LTI vehicles that best align with their business strategy and unique shareholder value proposition. For example, Aetna, Inc. replaced performance-based market share units (“MSUs”) with time-based stock appreciation rights (“SARs”) in 2014. Aetna disclosed that the longer term nature (10 years) of SARs “…supports the Company’s long-term strategic focus to drive change in the healthcare industry and to create long-term shareholder value.” Another example is Pfizer, Inc. which grants 5- and 7-year Total Shareholder Return Units (“TSRUs”). Pfizer discloses that the value executives realize from TSRUs “…is consistent with the value received by Pfizer’s shareholders.”

The table below outlines the reported changes among companies in our study:

|

Type of Change Reported in CD&A |

2013 No. of Cos. |

% of Cos. |

|

|

2013 (n = 51) |

2012 (n = 55) |

||

|

Change in mix of LTI award vehicles |

21 |

41% |

44% |

|

Change in performance plan metric |

17 |

33% |

27% |

|

Add or eliminate LTI vehicle |

10 |

20% |

36% |

|

Change in LTI award target opportunity level |

7 |

14% |

13% |

|

Change in performance plan comparison/peer group |

2 |

4% |

5% |

|

Other |

10 |

20% |

20% |

Note: Percentages add to greater than 100% due to multiple changes by certain companies.

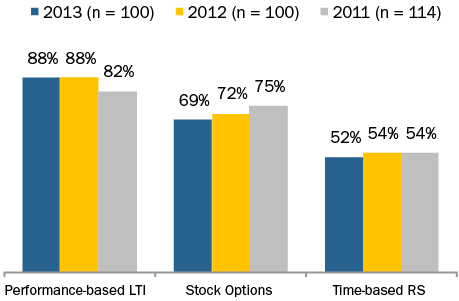

PREVALENCE OF LONG-TERM INCENTIVE VEHICLES

Over the past three years, the prevalence of stock options has declined slightly and the use of time-based restricted stock has been relatively flat. Companies tend to grant these vehicles as a supplement to performance-based LTI.

Below is the breakdown of the percentage of companies granting each LTI vehicle to NEOs from 2011-2013:

Note: Percentages add to greater than 100% because most companies grant a variety of vehicles.

Companies continue to use multiple vehicles to deliver LTI to executives. 51% of companies in our study deliver LTI in the form of two vehicles, 29% use three vehicles and 20% use only one vehicle. Among the companies that deliver LTI compensation through one vehicle, 60% grant only performance-based LTI.

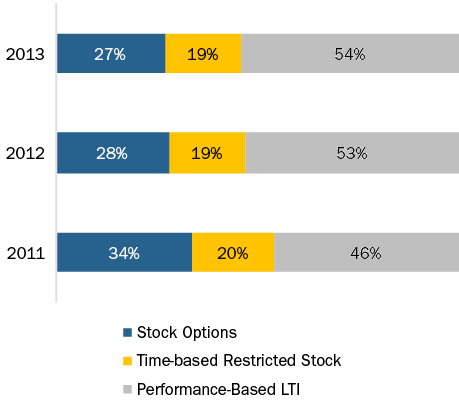

LONG-TERM AWARD MIX

The average LTI mix in 2013 is generally consistent with 2012. Performance-based LTI continues to represent more than half of the LTI mix (approximately 55% of total LTI) while stock options represent approximately 25% and time-based restricted stock represents 20%.

The chart below depicts the average LTI mix for NEOs as disclosed in the CD&A:

PERFORMANCE-BASED LTI METRICS

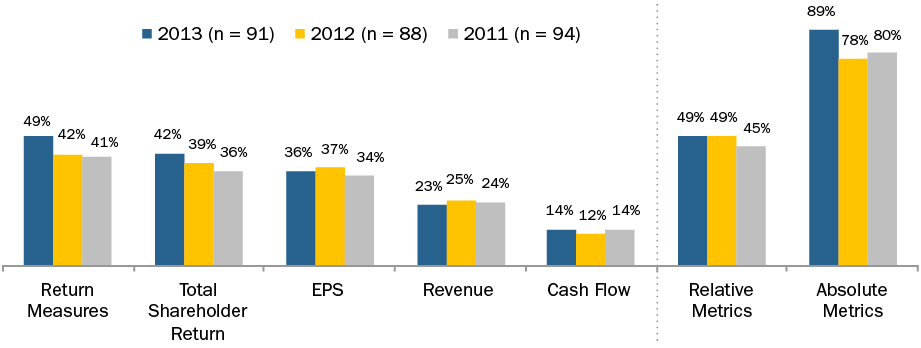

Companies routinely reassess their LTI plan design, including the performance metrics used, to ensure that the design reflects the company’s business strategy and objectives to attract, incentivize and retain executives. Among performance-based LTI plans, the use of a return measure increased to 49% in 2013 (up from 41% in 2011) indicating that companies are trying to encourage operational efficiency, along with profitability and growth. Among the companies that use return measures, 47% use ROI or ROIC, 37% use ROE and 16% use ROA. TSR and EPS are also prevalent long-term incentive metrics, used by 42% and 36% of companies, respectively. In our study, most companies with performance-based LTI plans use two metrics.

Companies are also more likely to use LTI metrics that reflect key measures of success in their industry. The Automotive industry frequently uses Cash Flow as a metric, focusing executives on liquidity to manage the significant cash requirements associated with the industry. In the Pharmaceutical and Technology industries, where the success of a company’s pipeline and current product offerings is reflected in their stock price, TSR is used more frequently as a metric.

Overall, 49% of companies in our study measure performance relative to the external market (typically using TSR) and 89% measure performance against pre-established goals (typically internal financial metrics). Although the use of relative TSR has increased slightly since 2011, the use of absolute internal financial metrics is most prevalent. Approximately 92% of companies that use TSR, measure performance relative to a defined comparator group (54% use a defined peer group, 40% use a broader industry index and 6% use both) while nearly 95% of companies measure financial performance against pre-established goals based on the business plan.

In recent years, companies have moved away from using only absolute or relative performance measures and instead frequently use a two-pronged approach. In 2013, 37% of companies used both absolute and relative performance measures compared with 24% in 2011. The use of both absolute and relative performance measures allows companies to evaluate performance from a balanced perspective, considering both internal and external results.

The chart below displays the prevalence of LTI metrics for performance-based awards in 2011-2013:

Note: Percentages add to greater than 100% due to multiple responses. Return measures reflect ROE, ROIC and ROA

CONCLUSIONS

The role played by performance-based LTI within LTI programs continues to grow. Performance-based LTI constitutes 54% of total LTI, on average, for NEOs. As performance-based LTI grows, the use of stock options and time-based restricted stock has been declining; however, these vehicles often have a role in a well-designed LTI program since stock option value depends on longer-term stock price appreciation and time-based restricted stock serves as an excellent retention vehicle.

The most commonly used metrics are return measures, such as ROI, as well as TSR and EPS. These metrics demonstrate that companies are attempting to use LTI to incentivize operational efficiency, profitability and growth. While most companies evaluate financial performance against internal goals, a growing number of companies have adopted a two-pronged approach to long-term performance measurement. These companies use internal financial goals and also incorporate a relative goal (typically TSR) to measure company performance in the context of the external market.

While most companies have already implemented changes that provide for a stronger link between executive pay and company performance, we expect to see companies continue to refine their performance-based LTI plans to support their business strategy. Additionally, we expect that setting meaningful long-term financial goals will continue to be a challenge for many companies leading some to incorporate relative performance metrics in the LTI program.

HIGHLIGHTS

- Companies rarely make wholesale changes to plans, but frequently revisit the performance metrics used

- Most companies use multiple measures to ensure the plan provides balance and aligns with overall business strategy

- Overall, 2013 annual incentive payouts were higher than in 2012 indicating stronger performance

Survey Sample

Compensation Advisory Partners (“CAP”) reviewed 2014 proxy disclosures at a sample of 100 companies among the Fortune 500 representing nine industry groups. Industry groups included: Automotive, Consumer Goods, Financial Services, Health Care, Insurance, Manufacturing, Pharmaceutical, Retail, and Technology. For the companies studied, the median revenue size and market capitalization was $32B and $52B, respectively. The median 2013 total shareholder return (TSR // change in stock price plus dividends) was 43%.

CHANGES IN ANNUAL INCENTIVE PLAN DESIGN

Overall, 34% of companies in CAP’s study changed their annual incentive plan design in 2013 or 2014. The most common changes were to the performance metrics used to fund awards (47% of the companies making a change) or to the weightings applicable to performance metrics (32%). Another frequent change was to increase the target award opportunities offered to Named Executive Officers; reductions in target awards were made much less frequently. These changes, as well as other modifications shown in the chart on the right, illustrate that companies continue to review and enhance the pay-for-performance relationship through changes to the annual incentive program.

|

Type of Change Reported in CD&A |

2013 No. of Cos. |

% of Cos. Reporting Changes |

||

|

2013 (n = 34) |

2012 (n = 37) |

2011 (n = 43) |

||

|

Change in performance metrics used to fund awards |

16 |

47% |

43% |

28% |

|

Change in performance metric weighting/mix |

11 |

32% |

35% |

42% |

|

Increased/Reduced target award opportunities (CEO and/or CFO) |

11 |

32% |

11% |

21% |

|

Other changes |

4 |

12% |

22% |

19% |

|

Change in maximum award payout |

3 |

9% |

8% |

12% |

Note: Due to multiple changes, does not add up to 100%.

Change in Performance Metrics

Among the companies that changed the annual incentive performance metrics, about one-half of companies modified plan metrics while maintaining the current number of metrics to better align pay with performance:

- Ten (10) companies kept the same number of metrics but replaced a metric in the incentive plan

- Four (4) companies reduced the number of metrics, and

- Two (2) companies added metrics to the current plan.

Several companies indicated that their rationale for changing annual incentive metrics was, in large part, to have a more holistic view of overall company performance and to better align incentives with their business strategy:

- AFLAC Inc: Added Operating Return On Equity (OROE) as a performance metric for senior vice presidents and above; this metric allows shareholders to evaluate AFLAC’s financial achievements relative to other organizations in terms of how effectively capital is used to generate earnings

- Danaher Corp: Added Return On Investment Capital (ROIC) in order to help validate the efficiency of earnings and complement the cash flow metric

- United Technologies Corp: Changed the earnings metric from EPS to Net Income since Net Income is not impacted by share repurchases

- Bristol-Myers Squibb: Replaced Adjusted Net Cash Flow from Operations with a metric for pipeline performance that consists of regulatory submissions and approvals and is a better indication of long-term growth potential.

Change in Target Bonus Opportunity

In 2013, median target bonus opportunities for CEOs increased (by 9 percentage points), while the opportunities for CFOs decreased (by 3 percentage points). Most notably, target bonus opportunity for CEOs in the Automotive, Insurance, and Retail industries increased by 10 percentage points year over year. However, the Technology industry experienced a significant decrease (21 percentage points) due to an increase in the base salary for Cisco’s CEO (from $375,000 to $1,100,000) and a decrease in the target opportunity for the new CEO at Intel (from 462.7% of base salary to 239.2%).

Median target bonus opportunity for CFOs in the Automotive industry experienced a decrease of 5 percentage points in 2013 largely due to the promotion of a new CFO at Goodyear (target opportunity decreased from 91% to 63% of base salary). Conversely, target bonus opportunity for CFOs in the Insurance industry increased (8 percentage points) in 2013; all other industries saw little movement to the target bonus opportunity.

|

Industry |

Median Target Bonus as a % of Salary |

|||||

|

CEO |

CFO |

|||||

|

2013 |

2012 |

2011 |

2013 |

2012 |

2011 |

|

|

Automotive |

135% |

125% |

130% |

85% |

90% |

88% |

|

Consumer Goods |

160% |

160% |

170% |

93% |

95% |

100% |

|

Financial Services |

n/m |

n/m |

n/m |

n/m |

n/m |

n/m |

|

Health Care |

150% |

145% |

145% |

100% |

101% |

100% |

|

Insurance |

210% |

200% |

200% |

133% |

125% |

120% |

|

Manufacturing |

157% |

154% |

156% |

100% |

97% |

95% |

|

Pharmaceutical |

150% |

150% |

150% |

98% |

97% |

91% |

|

Retail |

180% |

170% |

168% |

85% |

83% |

85% |

|

Technology |

210% |

231% |

200% |

130% |

131% |

121% |

|

Total Sample |

166% |

157% |

153% |

100% |

103% |

100% |

Note: Financial Services industry is excluded since most companies in our study do not disclose target bonus opportunities for the Named Executive Officers.

ANNUAL INCENTIVE PLAN DESIGN / PRACTICES

Award Leverage

Disclosure of the payout range (i.e., both threshold and maximum payout as a percentage of target) is a limited practice as most companies reviewed did not disclose a threshold level of performance required to receive a bonus payment. For the 37 companies that disclose a threshold bonus, 50% of target is the most common payout percentage. However, 20 companies disclose a minimum bonus payout of less than 50% of target; a majority of these companies provide a payout based on multiple plan metrics.

Approximately 75% of companies disclose the maximum bonus opportunity. A majority (60%) have a maximum bonus opportunity of 200% of target bonus. Ten (10) companies have a maximum bonus of 250% of target or higher. A majority of these companies are in the Consumer Goods, Pharmaceutical, and Technology industries.

|

Threshold as a % of Target (n=37) |

Maximum as a % of Target (n = 73) |

|||||

|

Range |

# of Cos. |

% of Cos. |

Range |

# of Cos. |

% of Cos. |

|

|

< 25% |

10 |

27% |

> 125% < 150% |

2 |

3% |

|

|

> 25% < 50% |

10 |

27% |

> 150% < 200% |

14 |

19% |

|

|

50% |

13 |

35% |

200% |

44 |

60% |

|

|

> 75% < 100% |

4 |

11% |

> 200% < 250% |

3 |

4% |

|

|

> 250% |

10 |

14% |

||||

Annual Incentive Plan Metrics

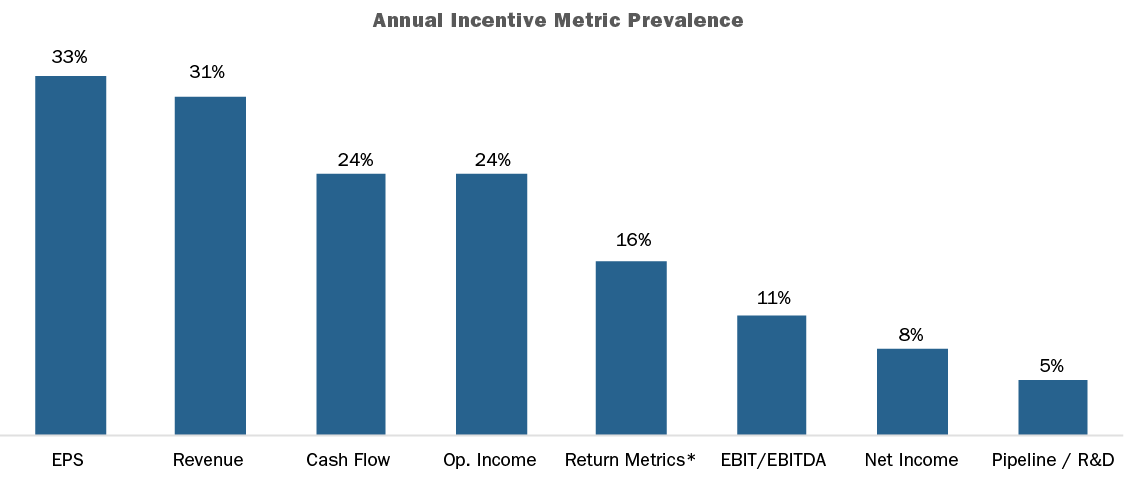

EPS, Revenue, Cash Flow and Operating Income are the most prevalent metrics used in annual incentive plans. Although EPS is the most common metric overall, it is the most common metric for only two industries (Financial Services and Healthcare). Revenue, the second most common metric, is the most prevalent in four industries (Consumer Goods, Pharmaceutical, Retail and Technology). Our findings suggest that EPS is used more broadly across industries while Revenue tends to be used in consumer-driven industries.

Most companies (approximately 70%) use more than one performance metric in the annual incentive plan. 25% of companies disclose using two (2) metrics in their annual incentive programs, 25% use three (3) metrics, and 21% of companies use four (4) or more metrics. Approximately 62% of these companies use a profit-based metric in combination with Revenue and/or Cash Flow.

The chart below shows the three (3) most metrics by industry in 2013:

|

Industry |

Metric #1 |

Metric #2 |

Metric #3 |

|

Automotive |

Cash Flow (45%) |

EBIT (45%) |

ROA (27%) |

|

Consumer Goods |

Revenue (67%) |

EPS (58%) |

Cash Flow (33%) |

|

Financial Services |

EPS (33%) |

ROE (17%) |

Op. Income (8%) |

|

Health Care |

EPS (40%) |

Op. Income (30%) |

EBIT (30%) |

|

Insurance |

Op. Income (46%) |

Op. ROE (23%) |

Op. EPS (15%) |

|

Manufacturing |

Cash Flow (30%) |

EPS (30%) |

Revenue (20%) |

|

Pharmaceutical |

Revenue (70%) |

EPS (70%) |

Pipeline/R&D (50%) |

|

Retail |

Revenue (40%) |

Op. Income (40%) |

EBIT (30%) |

|

Technology |

Revenue (58%) |

Cash Flow (50%) |

Op. Income (33%) |

Note: Percentages reflect the prevalence of companies disclosing the metric.

*Return metrics include: ROE, Op. ROE, ROA, and ROI/ROIC

2013 Actual Bonus Payout

Nearly all companies (98%) in our research awarded bonuses to their Named Executive Officers for 2013 performance. Overall, the median CEO bonus was 121% of target compared to 112% in 2012, indicating that 2013 performance was generally stronger than 2012. Most industries exceeded target bonus payouts by 11 – 65 percentage points. However, two industries (Retail and Technology) fell short of expectations by 22 and 12 percentage points, respectively.

Use of deferral mechanisms in the annual incentive plan is a limited practice and is more common in the Financial Services industry given regulations from the Federal Reserve. However, a few companies across industries also have a deferral policy in place. Companies typically defer annual incentive payment in the form of restricted stock/units.

|

Industry |

Actual Bonus as a % of Target Bonus – CEO |

||||||||

|

75th Percentile |

Median |

25th Percentile |

|||||||

|

2013 |

2012 |

2011 |

2013 |

2012 |

2011 |

2013 |

2012 |

2011 |

|

|

Automotive |

183% |

131% |

186% |

165% |

102% |

153% |

127% |

69% |

130% |

|

Consumer Goods |

133% |

137% |

149% |

112% |

103% |

132% |

70% |

94% |

78% |

|

Financial Services |

142% |

120% |

130% |

126% |

80% |

114% |

101% |

44% |

111% |

|

Health Care |

149% |

157% |

159% |

127% |

127% |

127% |

116% |

103% |

116% |

|

Insurance |

170% |

144% |

130% |

150% |

130% |

106% |

123% |

112% |

85% |

|

Manufacturing |

119% |

146% |

162% |

111% |

107% |

136% |

98% |

100% |

119% |

|

Pharmaceutical |

158% |

156% |

161% |

138% |

142% |

144% |

122% |

125% |

130% |

|

Retail |

119% |

136% |

147% |

78% |

117% |

129% |

68% |

79% |

112% |

|

Technology |

121% |

124% |

149% |

88% |

99% |

100% |

69% |

90% |

75% |

|

Total Sample |

151% |

144% |

156% |

121% |

112% |

133% |

96% |

93% |

105% |

Note: Most companies in the Financial Services industry does not disclose target bonus. Figures for the Financial Services industry reflects bonus as a percentage of 3-year average actual bonus.

Use of Discretion

Approximately 50% of companies in our research disclose the use of discretion in the annual incentive plan. Among these companies, approximately 40% allow only for downward adjustments of the final payout. Approximately 55% allow for both upward and downward adjustments by funding bonuses for Name Executive Officers at maximum based on a financial metric (this is unrelated to the final award allocation which may have additional performance requirements) to ensure compliance with Section162(m) of the Internal Revenue Code. This approach provides the Committee with the most flexibility in determining the bonus payout.

Conclusion

Given significant changes to the annual incentive plan design in recent years, companies rarely made wholesale changes to the overall plan design in 2013 or for 2014. Among the companies that made changes, most were focusing on refining the incentive metrics to ensure a more complete view of company performance and alignment with the overall business strategy. Despite these changes to the incentive metrics, EPS, Revenue, Cash Flow and Operating Income continue to be most common. While we would not expect to see extensive changes to the incentive plan design in the future, we anticipate that companies will continue to refine their metrics and the metric weightings as they continue to ensure executive pay is aligned with performance.

Partner Susan Schroeder and Principal Bonnie Schindler are interviewed on their 2014 survey of non-profit and government incentive pay practices.