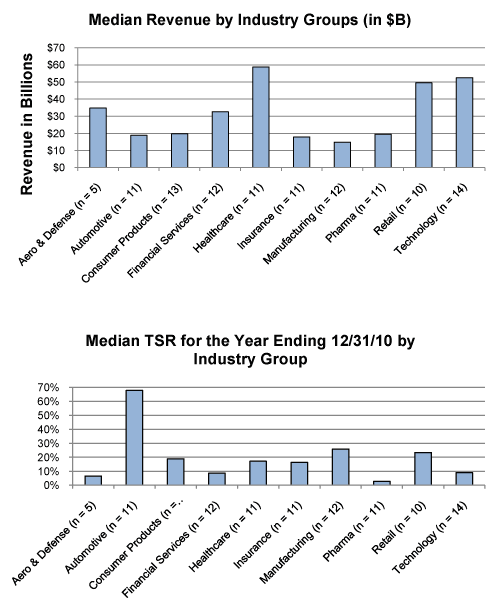

For the 111 company sample, median revenue was $27B, market capitalization was $30B and Total Shareholder Return (TSR) was 16% for 2010.

What We Found

Highlights of our research findings are below. Most companies did not make sweeping changes to their executive compensation programs. But many companies continued to refine annual and long-term incentive plans to strengthen the alignment between executive rewards and financial performance and to focus executives on the overall health of the organization.

Compensation Strategy Changes

Similar to 2009, most companies did not make significant changes to their compensation strategy. Financial Service firms were more likely to make changes to the strategy (e.g., increase at-risk pay) as they emerged from compensation restrictions imposed by TARP.

Peer Groups Used For Benchmarking

In 2010, companies continued to review and modify their peer group, although wholesale changes were not the norm. Approximately 40% of companies made some modification to their peer group by selecting peers that more closely aligned with their size and business mix. Pharmaceutical companies, in particular, continued to make changes to the peer group as industry consolidation continued.

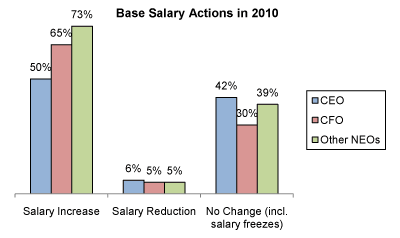

Base Salary Actions

2010 saw the return of salary increases for senior executives with a majority of companies providing salary increases to Named Executive Officers (NEOs) in 2010 (vs. 20% in 2009) as the economy improved. Within the NEO ranks, companies provided increases more frequently to executives below the CEO as they focused on retaining top talent and remaining competitive with the market. Salary reductions were most prevalent in companies that emerged from TARP, as these companies reverted to a compensation mix that provides a greater emphasis on incentive-based pay. Fewer companies froze base salaries for NEOs in 2010; companies in the Consumer Goods, Retail and Technology industry groups were more likely to maintain salaries at 2009 levels.

Annual Incentive Plan Design

Approximately 50% of companies disclosed a change in 2010 or planned changes for 2011 to their annual incentive plan design. Companies continued to refine the metrics and weightings that determine plan funding and payout as pay for performance remains a major focus for companies. 26% of companies increased the target annual incentive opportunity for at least one NEO illustrating that companies are focusing on the competitive market given the improvements in the economy. Although changes to annual incentive plans vary by company, there continues to be an attempt to reward executives based on appropriate indicators of company success.

The chart below presents the reported AIP changes:

| % of Cos. Reporting Changes | |||

| Type of Change Reported in CD&A | No. of Cos. | 2010 (n = 57) | 2009 (n = 34) |

| Change in performance metrics used to fund awards | 19 | 33% | 44% |

| Change in performance metric weighting mix* | 10 | 18% | n/a |

| Increased target award opportunities | 15 | 26% | 26% |

| Adopted / amended annual incentive plan | 13 | 23% | 6% |

| Modified performance scale | 6 | 11% | n/a |

| Reduced maximum award payout leverage | 2 | 4% | 12% |

| Other changes | 9 | 16% | 9% |

Note: Percentages do not add up to 100% due to multiple responses.

* Not captured separately in 2009 and is included in preceding category.

Change in Performance Metrics

Of the 19 companies that made changes to performance metrics, most (10 companies) added metrics to the plan design. Additionally, 10 companies changed the weighting of the AIP metrics. In general, these changes were focused on basic company performance indicators such as profitability and cash flow. For example,

- Computer Sciences: Added free cash flow as a measure to emphasize the importance of liquidity and profitability

- Morgan Stanley: Added capital adequacy and credit rating measures to the metrics used to determine financial achievements

- Visteon: Added product quality and free cash flow as performance metrics

Many companies added cash flow as an annual incentive metric in 2010 indicating that in the wake of the recent economic downturn, companies are balancing profitability with liquidity.

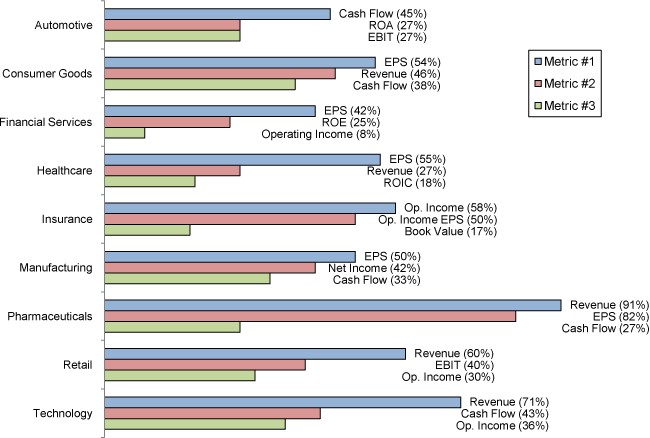

Annual Incentive Plan Metrics

In 2010, the most common metrics used across all industry groups were revenue or revenue growth, EPS and cash flow. Cash flow was one of the three most common metrics in five industry groups (Automotive, Consumer Goods, Manufacturing, Pharmaceuticals and Technology). More than other industries, annual incentive metrics for insurance companies tend to focus on industry-specific measures. The most prevalent metrics in the Automotive industry are cash flow and return on assets (ROA) denoting a focus on company operating performance during the economic recovery.

The three most prevalent metrics for each industry group are detailed below:

Note: Excludes Aerospace and Defense due to limited sample size (n = 5).

2010 Bonus Payout Details

Nearly all companies (95%) paid a bonus to an NEO for 2010. Most companies (90%) used financial performance to calculate the payout, although many of these companies (19%) also used discretion (positive and negative) to account for non-financial performance. Actual bonus payouts for CEOs on average were approximately 135% of the target incentive opportunity for 2010, indicating a rebound in financial performance in 2010 over 2009.

Long-Term Incentive Plan Design

A majority of companies (approximately 70%) reported making changes to their long-term incentive plan designs in 2010 or for 2011. Similar to the annual incentive plan changes, many companies (32%) reported changes to the performance metrics used to determine award payouts. 26% of companies reported changes to the LTI vehicle mix, with companies placing more emphasis on performance-based awards. This suggests that companies are focusing executives on longer-term goals. The table below outlines the reported changes:

| % of Cos. Reporting Changes | |||

| Type of Change Reported in CD&A | No. of Cos. | 2010 (n = 77) | 2009 (n = 60) |

| Changed long-term performance metric | 24 | 31% | 38% |

| Adopted / amended long-term incentive plan | 24 | 31% | n/a |

| Changed mix of LTI award vehicles | 20 | 26% | 55% |

| Added or eliminated LTI vehicle* | 22 | 29% | n/a |

| Changed LTI award opportunity level | 14 | 18% | 20% |

| Changed performance metrics/weighting | 6 | 8% | n/a |

| Other | 17 | 22% | 35% |

Note: Percentages do not add up to 100% due to multiple responses.

* Not captured separately in 2009 and is included in preceding category.

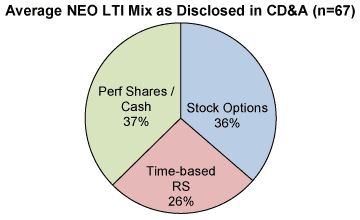

Long-Term Award Mix

From companies making changes to their LTI award mix, a majority (60%) disclosed that they increased the emphasis on performance by shifting a portion of total LTI value from time-based awards (options and restricted stock) to performance-based vehicles. On average, companies are providing approximately 25% of the total LTI awarded to NEOs in time-based restricted stock with the remaining value equally split between performance-based LTI and stock options.

| % of Cos. Reporting Changes | |||

| Type of Change Reported in CD&A | No. of Cos. | 2010 (n = 20) | 2009 (n = 33) |

| Greater emphasis on performance-based awards | 12 | 60% | 55% |

| Reduced emphasis on time-based restricted stock | 7 | 35% | n/a |

| Reduced emphasis on stock options | 5 | 25% | n/a |

| Other | 5 | 25% | 45% |

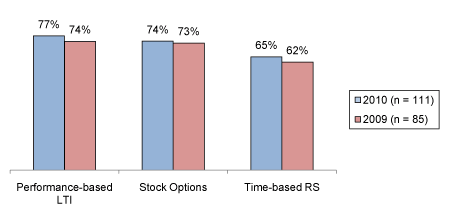

Long-Term Incentive Prevalence

Although companies making a change indicated they are placing a greater emphasis on performance-based awards, equity awards with time-based vesting continue to be prevalent. The prevalence of stock options and restricted stock with time-based vesting remained relatively flat in 2010, with 74% and 65% of companies using these vehicles, respectively.

Below is the breakdown of overall LTI vehicle prevalence for NEOs in 2010 vs. 2009:

Note: Percentages do not add up to 100% due to multiple responses.

Companies typically grant multiple LTI vehicles to NEOs to offer a balanced program with different performance metrics and time horizons. Most companies (77%) grant two or three award vehicles to provide LTI to executives.

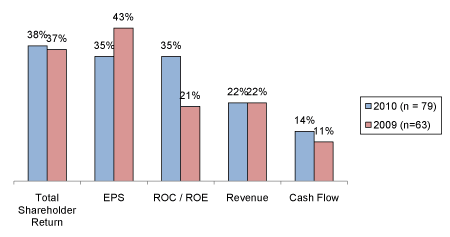

Performance-Based LTI Metrics

For companies using performance-based LTI, TSR (38%) and EPS (35%) continue to be the most prevalent metrics. More companies are incorporating return on capital or return on equity as a metric in 2010 to increase the focus on longer term health/stability and the quality of earnings. The use of revenue and cash flow remained relatively flat year over year.

The chart below displays the prevalence of LTI metrics for performance-based awards in 2010 and 2009:

Note: Percentages do not add up to 100% due to multiple responses.

Treatment of Dividend Equivalents

Approximately 40% of companies that grant restricted stock (either time-based or performance-based) and 20% of companies that grant performance shares / units disclose that they pay dividend equivalents to executive officers. Companies typically pay dividends when the shares have vested or are earned.

Conclusions

2010 saw changes to annual and long-term incentive plan design in response to the rebounding economy, greater shareholder scrutiny, as a result of say on pay, and an attempt to further align pay and performance. With the economy on the rebound companies provided more frequent salary increases to NEOs in 2010 and were less likely to freeze base salaries. Companies modified incentive plan metrics, focusing on both company profitability and cash flow. The executive LTI mix continues to shift, with companies reporting more emphasis on performance-based awards. We expect to see companies continue to refine pay programs overall with the objective of strengthening pay and performance linkages and transparency.

To determine if this trend is continuing, Compensation Advisory Partners conducted a study to determine how CFO pay has changed over the last three years and how the year-over-year trends in compensation compare to trends in CEO pay. The study analyzes executive pay data disclosed by early proxy filers and includes 55 US public companies with revenues ranging from $1 billion to $150 billion, with median revenues of $10 billion. Only companies with the same incumbent CEO and CFO from 2008 to 2010 were included in order to focus on year-over-year changes for an individual. Financial services firms were excluded from the study as this industry, in particular, saw the emergence of several atypical compensation arrangements and special awards that were both temporary and unique to the financial services industry.

Our findings, summarized below, indicate that CFO pay is generally moving at the same rate as CEO pay. Salaries are increasing at a slightly faster rate for CFOs but incentive compensation, both annual and long-term, is moving at the same rate for CFOs and CEOs, illustrating that incentive levels are tied to company results. For 2010, incentives are up for both CFOs and CEOs, reflective of a slowly rebounding economy.

Study Results

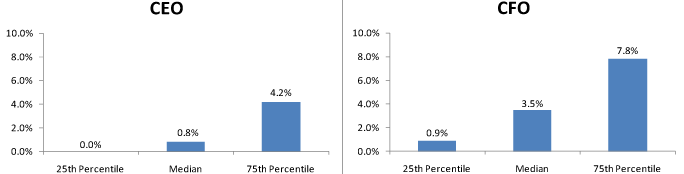

Salaries

In 2010, 78% of CFOs received salary increases at a rate of 3.5% at median and 7.8% at the 75th percentile. In comparison, only 55% of CEOs received salary increases at lower levels (0.8% at median and 4.2% at the 75th percentile). The prevalence of no salary increases also rose among CEOs from 40% in the 2008-2009 period to 46% in the 2009-2010 period while for CFOs, the prevalence of no salary increases decreased to 22% in the 2009-2010 period versus 31% in the 2008-2009 period.

Salary Increase Prevalence

| 2008-2009 | 2009-2010 | |||

| No Increase | Increase | No Increase | Increase | |

| CEO | 40.0% | 60.0% | 45.5% | 54.5% |

| CFO | 30.9% | 69.1% | 21.8% | 78.2% |

2010 Salary Increases

Actual Pay Levels

Overall, actual total direct compensation (salary plus actual annual incentive plus the present value of long-term incentives) for both CFOs and CEOs slightly declined in 2009 and subsequently rebounded in 2010, as illustrated by the chart below. CFO pay fell at a slightly higher rate in 2009 and increased at a higher rate in 2010 compared to CEO pay. The rise in 2010 pay levels was primarily due to increases in incentive (performance-based) compensation. Bonuses increased by approximately 16% and LTI increased by 14% – 19%. These increases in incentive compensation are most likely reflective of the recovering economy, improvements in company financial performance and rebounding stock prices.

Median Percentage Change in Pay Components

| 2008-2009 | 2009-2010 | |||

| CEO | CFO | CEO | CFO | |

| Salary | 0.7% | 2.0% | 0.8% | 3.5% |

| Actual Bonus | -3.1% | 3.5% | 16.3% | 15.6% |

| Long-Term Incentives | -2.4% | -5.7% | 13.7% | 18.6% |

| Actual Total Direct Comp. | -4.7% | -5.2% | 18.3% | 23.3% |

Financial Performance (Median Levels)

| Year | Total Shareholder Return (as of 12/31) | 1-Year Revenue Growth | 1-Year Revenue Growth |

| 2008 | -32% | 8% | 2% |

| 2009 | 26% | -8% | -6% |

| 2010 | 21% | 9% | 19% |

While movement in pay among CFOs and CEOs was directionally similar, on average, CFO actual total direct compensation was generally 30 – 35% of CEO actual total direct compensation over the last three years.

Target Pay Mix

When considering compensation at target levels, the pay mix remained largely unchanged from 2008 to 2010, with a greater emphasis on at-risk pay for CEOs than for CFOs. The pay mix for CFOs slightly shifted towards incentive-based compensation (from 77% in 2008 to 80% in 2010) showing that the pay mix for CFOs is moving closer to that of CEOs.

Long-Term Incentive (LTI) Vehicle Prevalence

The majority of companies awarded LTI to both CEOs and CFOs using at least two vehicles. The prevalence of stock options in the LTI mix declined over the 3-year period while the prevalence of performance-based awards increased. Overall, 83% of CFOs and 85% of CEOs received some form of performance-based awards as part of their LTI program in 2010.

Number of LTI Vehicles Used in 2010

| % in Total | ||

| CEO | CFO | |

| 1 | 13% | 15% |

| 2 | 61% | 54% |

| 3 | 26% | 31% |

| Average | 2 | 2 |

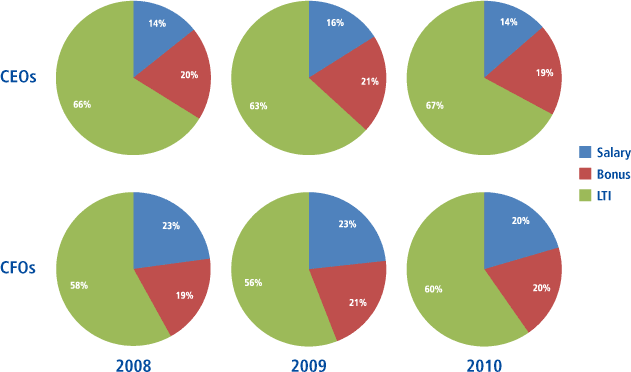

Long-term Incentive Mix

The majority of LTI continues to be delivered in the form of stock options and performance-based LTI, with less emphasis on restricted stock.

LTI Mix

| 2008 | 2009 | 2010 | ||||

| CEO | CFO | CEO | CFO | CEO | CFO | |

| Stock Options | 44% | 41% | 39% | 39% | 34% | 31% |

| Time Vested Restricted Stock | 16% | 22% | 17% | 20% | 17% | 20% |

| Perf. Based LTI | 40% | 37% | 43% | 41% | 49% | 48% |

Conclusion

In the last two years, trends in CFO pay have been directionally aligned with trends in CEO pay. The target pay mix for CFOs has slightly increased the emphasis on incentive compensation relative to fixed compensation, moving closer to the pay mix of CEOs. Salaries are increasing at a faster rate for CFOs but incentive compensation is increasing at about the same pace for both CFOs and CEOs, indicating a link to company performance results, and emphasizing that the role of the CFO continues to be important. We expect companies to continue to ensure that they have the right skill set in the CFO role and develop compensation programs that attract and motivate key talent.

Please contact us at (212) 921-9350 if you have any questions about the issues discussed above or would like to discuss your own executive compensation issues. You can access our website at www.capartners.com for more information on executive compensation.

Seventy companies were invited to participate in the survey and nineteen completed the full survey. Several companies that did not participate expressed interest, but said that they were too early in the decision-making process to respond.

We asked seven questions in the survey. Here is what we found:

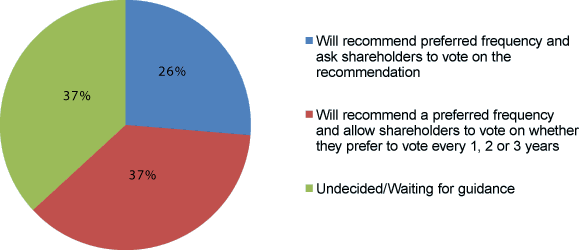

1) Dodd-Frank mandates that companies must solicit a non-binding advisory Say-on-Pay vote from shareholders at least once every three years. Do you anticipate your Board recommending that shareholders approve a specific (preferred) frequency for Say-on-Pay or will you allow shareholders to decide by voting?

The new legislation requires companies to hold a non-binding advisory vote on their executive compensation at least once every three years and to give shareholders the opportunity to vote on the frequency of the Say-on-Pay vote at least every six years. The legislation does not specify the method for the frequency vote (e.g., give shareholders the full range of choices without a recommendation, recommend a preferred frequency but let shareholders pick from the full list, or give the shareholders a yes/no vote on a frequency recommended by management and Board).

The survey results indicate that companies are fairly evenly split between recommending a preferred approach but allowing shareholders to vote on the range of choices (37%) and asking shareholders to vote yes/no on a specific frequency (26%). The remainder of the sample (37%) is undecided or waiting for guidance.

Recommending a Say-on-Pay Vote Frequency to Shareholders

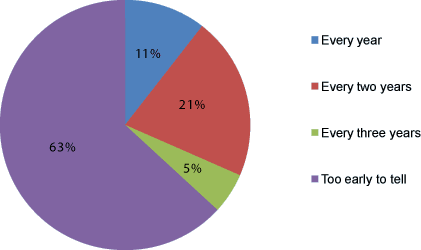

2) If you are going to recommend a preferred frequency to shareholders for Say-on-Pay voting, what do you expect to recommend?

Most companies (63%) say it is too early to tell which frequency they will recommend. Of those that did specify a time period, two years was the most common (21%). But keep in mind that this represents four companies. Given discussions we are having with clients, we would not be surprised if one or three years becomes the more common approach when companies finally implement Say-on Pay.

Choosing a Say-on-Pay Vote Frequency

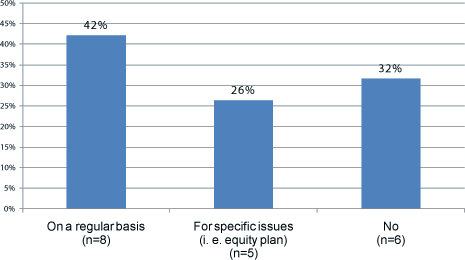

3) Does your company currently engage in active dialogue with your 10 largest shareholders at least once a year on your Company’s executive compensation practices?

Even absent Say-on-Pay, we believe engaging in open and meaningful dialogue with large shareholders is a best practice and can provide insights and avoid surprises. 42% of companies say they currently engage in active dialogue with their shareholders and 26% do so for specific issues (e.g., approval of a new equity plan).

Dialogue with Largest Shareholders

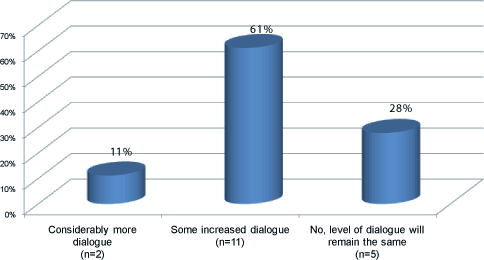

4) Do you anticipate increasing dialogue with your largest shareholders, relative to your executive compensation practices, as a result of the legislation?

We believe companies will increasingly engage their shareholders in dialogue to gain greater insight from them on their views on executive compensation, since this is more informative than a yes/no vote on the full executive compensation program. This is supported by the survey which finds that 70% of respondents expect to increase dialogue with shareholders to at least some degree.

Increasing Dialogue with Largest Shareholders

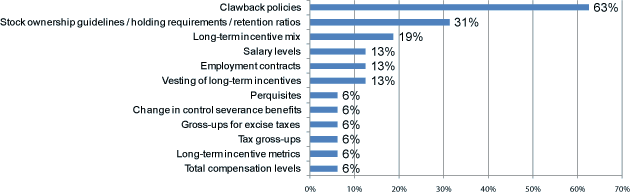

5) Do you anticipate making meaningful changes to any of your executive compensation practices/programs as a result of the Say-on-Pay requirements?

The most commonly anticipated change to executive compensation programs is clawbacks, which is a requirement of the new legislation (63%). Just under one-third of companies anticipate changing their stock ownership and holding requirements. While ownership requirements have been very common, holding requirements (where an executive must hold all or a portion of net shares realized from option exercise (net of taxes and exercise price) and vested equity (net of taxes)) for a specified period time has been an emerging trend. Many more companies may begin to adopt this practice as they try to provide for greater alignment between executives and shareholders.

Anticipated Changes to Executive Compensation Programs*

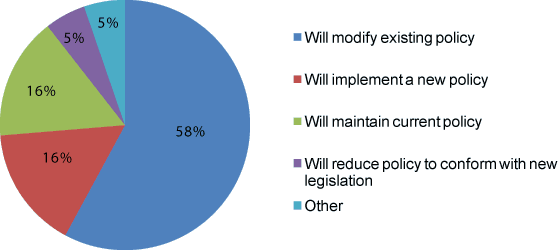

6) Do you anticipate changing or implementing a clawback policy?

Many companies implemented or enhanced their clawback policies in the recent past; however, the new legislation specifies that the period covered span 3 years. Many companies (58%) must adjust their policy to comply with the new requirements.

Clawback Policy

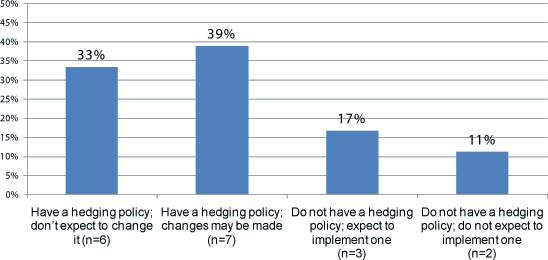

7) Do you anticipate changing or implementing hedging policies?

Unlike the clawback requirement, the new legislation does not require a company to implement a hedging policy; however, a company must disclose if it does not have such a policy. 33% of companies currently have a hedging policy and will leave it unchanged. 56% of companies will either implement a policy or anticipate reviewing or changing their current policy. Only 11% state they do not have a hedging policy and do not anticipate implementing one. These companies will have to disclose that they do not have a hedging policy and this may be a negative for shareholders.

Hedging Policy

We hope you find these early findings helpful. Since the SEC will be providing guidance and there is a lot of uncertainty, where companies land on these issues is something of a moving target. Some of the key steps we believe companies should take in the interim include:

- Discussing the implications of the legislation with their Compensation Committee

- Forming a working team to develop a response, including: Human Resources/Compensation, Legal, Investor Relations, outside consultant and legal counsel

- Engaging in dialogues with large institutional shareholders

If you would like to participate in our CAPFlash survey topics going forward, please feel free to sign up at https://www.capartners.com/signup-surveys

* Responses add to more than 100% due to multiple responses by company

***

Please contact us at (212) 921-9350 if you have any questions about the issues discussed above or would like to discuss your own executive compensation issues. You can access our website at www.capartners.com for more information on executive compensation.

What We Found

In response to continued focus on executive compensation and recently enacted legislation, many companies are strengthening governance and other pay practices. The most significant change is the assessment and identification of any material risks arising from compensation programs, required by the SEC for all public companies for the first time in 2010. We also see widespread use of clawbacks, continuing focus on reducing perquisites, executive benefits and eliminating tax gross-ups on perks. Companies are reducing supplemental retirement benefits and continue to emphasize stock ownership guidelines and stock retention requirements.

Compensation Risk Disclosure

The review of material risk arising from compensation programs is an important process, initially required for TARP companies and now required for all public companies by the SEC. Of the 85 companies in our study, 75 companies or 88% make some type of affirmative disclosure related to their assessment of risk in the compensation program. While some companies disclose changes that were made to the compensation programs to discourage risk, none of the companies in our study indicate that their programs can create material adverse risks. The large number of companies including affirmative disclosure in proxy statements is striking, since the disclosure is not required under current rules. Of the 10 companies that did not address compensation risk in their proxy statements, 5 or 50% filed their proxy statements prior to the publication of the SEC’s final disclosure rules in December 2009.

Most of the companies make their risk-related disclosures in the CD&A, with the next most common disclosure being in Section 407, the corporate governance section of the proxy statement. The table below summarizes where risk disclosures were made:

| Section of the Proxy Statement with Compensation Risk Disclosure | No. of Cos. | % of Cos. (n = 75) |

| CD&A | 39 | 52% |

| Section 407 | 19 | 25% |

| CD&A and Section 407 | 7 | 9% |

| Comp Committee Report or Comp Committee Report and CD&A | 2 | 3% |

| Separate Stand Alone Section | 8 | 11% |

The type of disclosure varies significantly, ranging from an in-depth description of the process and key safeguards to just one sentence indicating that the company’s programs do not encourage excessive risk-taking. 71% of the companies that make risk-related disclosures indicate that a formal risk review was conducted and comment on their assessment. Among these companies, the most common approach to the risk review is collaboration between the Compensation Committee, management and the Committee’s independent consultant (20%). The table below summarizes the different approaches used:

| Approach to Compensation Risk Reviews | No. of Cos. | % of Cos. (n = 75) |

| Compensation Committee, Committee’s Consultant and Management | 15 | 20% |

| Compensation Committee and Management | 10 | 13% |

| Compensation Committee and Committee’s Consultant | 9 | 12% |

| Compensation Committee | 7 | 9% |

| Management | 7 | 9% |

| Management and Management’s Consultant | 1 | 1% |

| Not Disclosed | 26 | 35% |

29% of the companies do not describe the risk assessment process and only comment on the results of their assessment of the compensation program. A majority of the companies (84%) describe safeguards that are in place to reduce risk-taking. Such safeguards often include:

- Balanced mix of short and long-term pay

- Use of multiple performance metrics

- Vesting requirements for equity vehicles

- Incentive plan caps

- Clawback policies

- Stock ownership requirements

- Committee discretion and oversight

Clawbacks

The use of clawbacks has increased dramatically in the past few years as a result of SOX and TARP regulations. The policies help alleviate shareholder concerns over managing risk and are viewed as stronger corporate governance. Clawbacks are currently mandated by the SEC for all public company CEOs and CFOs under SOX, for the top 25 executives for participants under TARP, and going forward for executive officers at all public companies as part of the Wall Street Reform and Consumer Protection Act of 2010.

Reflecting broad market trends, a significant majority of our research companies—68 of 85 companies or 80%—maintain some form of clawback provision. For 2009 and 2010, 5 of the 68 companies put a new policy in place and 16 modified existing policies, by expanding the type of compensation that can be recouped, the events that trigger a clawback, or the executives covered.

A financial restatement is required in nearly all cases. Further, 48 companies (71% of those with a clawback) disclose that fraud or misconduct are triggering events. Twelve companies (18%) disclose a non-compete/non-solicitation/confidentiality violation as a trigger, and three include improper ‘risk analysis’ as a trigger.

Based on our review of CD&A disclosures, companies with a clawback include the ability to clawback or recoup the following types of compensation: earned, exercised, outstanding, vested or unvested.

| Compensation Covered in Clawback Policies | No. of Cos. | % of Cos. (n = 68) |

| Incentive compensation (cash or equity) | 40 | 59% |

| Annual incentives only | 5 | 17% |

| Equity incentives only | 5 | 17% |

| Deferred cash | 4 | 6% |

| Severance benefits | 1 | 2% |

| 401k plan (company contributions) | 1 | 2% |

| Future compensation | 7 | 10% |

| Company discretion regarding type of compensation to recoup | 10 | 15% |

Note: Percentages add up to greater than 100% due to multiple responses.

Of interest, examples of some of the less common provisions we found include:

- IBM: Expanded clawback provisions by amending the Excess 401(k) Plus Plan to allow the clawback of Company contributions made after March 2010

- JP Morgan: Failure to identify, raise, or assess, in a timely manner as reasonably expected, risks and/or concerns with respect to risks material to the Firm or its activities, leads to recovery of equity awards for Operating/LOB Management Committee members

- McDonalds: Awards under the severance plan can be recovered if the participant engages in willful fraud that causes harm to the company or is intended to manipulate the performance measures that determine award payouts

- Progressive: Limits recoupment to excess bonus payments as a result of incorrect financial results to the extent that the recovery exceeds the lesser of 5% of the bonus paid or $20,000

In many cases, it is difficult to determine precisely who the clawback policy applies to. Where such disclosure is clear, we note that 17 companies cover all executives in the recovery of any ‘unearned’ compensation, regardless of whether the individuals directly caused any inaccuracy leading to a recovery.

A minority of companies tier their clawback policies, with certain parameters applying to Named Executive Officers, and other parameters applying to a broader ‘executive’ group. In some cases, clawback provisions in long-term incentive awards relate broadly to all eligible award participants.

Many companies did not indicate the time period within which compensation can be recovered after a restatement. Of the 17 cos. that did disclose a time frame for the clawback, the most common is 1 year from the date of restatement, and the range is 1 – 5 years. Three companies indicate that there is no time limit.

Since clawback policies are required by the Wall Street Reform and Consumer Protection Act of 2010 that was recently signed into law, companies will need to review and adopt provisions that align with the new legislation. The law applies to current and former executives who received incentive compensation during the 3 years before the restatement date, with employee misconduct not required as a trigger. SEC guidance is pending.

Stock Ownership Requirements

Stock ownership requirements continue to be an important tool for aligning executives with longer-term shareholder value. The majority of companies have stock ownership guidelines for their executives, typically expressed as a multiple of salary. While less common, many companies also have stock holding requirements where executives must hold a percentage of net shares from stock option exercises or vesting of restricted shares for a period of time. Within our sample, 17 companies, or 20% made changes to their stock ownership requirements. The most significant change among the companies in the study was the adoption or implementation of more restrictive stock holding requirements. Other changes, such as eliminating or extending the compliance time frame, suspending or decreasing ownership guidelines and changing to a fixed number of shares are responses to the volatility in the stock market.

| Type of Change Reported in 2010 CD&A | No. of Cos. | % of Cos. (n = 17) |

| Newly Adopted/More Restrictive Stock Holding Requirements | 8 | 47% |

| Eliminated/Extended Compliance Timeframe | 4 | 24% |

| Increased Stock Ownership Guidelines | 3 | 18% |

| Newly Adopted Stock Ownership Guidelines | 2 | 12% |

| Suspended Ownership Guidelines | 2 | 12% |

| Decreased Stock Ownership Guideline | 1 | 6% |

| Changed Stock Ownership Guideline from Multiple of Salary to Fixed Share Guideline | 1 | 6% |

Note: Percentages add up to greater than 100% due to multiple responses.

Perquisites

Companies continued to reduce perquisites in 2009, building on a trend that has been evident for several years. 16 of 85 companies or 19% of the sample made a change to perquisite programs. A number of companies also eliminated tax gross-ups on perquisites, responding to widespread criticism of this practice.

| Type of Change Reported in 2010 CD&A | No. of Cos. | % of Cos. (n = 16) |

| Reduced perks | 11 | 68% |

| Eliminated tax gross-ups on perks | 10 | 63% |

Note: Percentages add up to greater than 100% due to multiple responses.

The most common reduction in perquisites – seen at 6 of 11 companies (38%) that reduced perquisites—involved curbs on personal use of corporate planes by senior executives. Examples include:

- Eli Lilly: No longer allows executive officers to use company planes for travel to outside board meetings

- Genworth Financial: In 2009, suspended all incidental personal use of corporate aircraft

- MetLife: CEO is no longer required to use the company plane for personal travel

- Morgan Stanley: CEO entered into an aircraft time-sharing agreement with the Company and has since fully reimbursed the Company for the cost of his personal use of the Company aircraft up to the maximum amount permitted by federal aviation regulations

- PNC Financial: Required certain executives to pay for all personal trips on corporate aircraft

- Sara Lee: Terminated all use of its corporate aircraft

Severance And Change In Control Benefits

Given the economic and governance climate, change in control severance benefits have garnered a great deal of attention in recent years from shareholders, advisory groups and the media. In response, program changes have gained traction.

14 of our 85 research companies, or 16%, disclosed changes for 2009/2010 in most recent proxy CD&As consistent with what we are seeing in the broad market:

| Severance and CIC Program Changes | No. of Cos. | % of Cos. (n = 14) |

| Removed excise tax gross up feature – For current participants – For future participants (new hires/ promotions) |

6 2 4 |

43% |

| Changed equity vesting from single to double trigger | 3 | 21% |

| Reduced overall severance and CIC benefits | 2 | 14% |

| Changed definition of pay (bonus) for severance calculation | 2 | 14% |

| Reduced number of eligible participants | 1 | 7% |

| Eliminated executive CIC agreements, introduced exec severance plan | 1 | 7% |

| Increased excise tax cutback threshold above IRS limit | 1 | 7% |

| Eliminated pension supplement | 1 | 7% |

| Reduced benefit continuation period | 1 | 7% |

| Adopted new CIC plan | 1 | 7% |

Note: Percentages add up to greater than 100% due to multiple responses.

Program changes in 8 companies impact current participants and in 6 companies changes apply to new participants only. Five of the 14 companies making changes are in the pharma industry and three are in health care.

Executive Retirement Benefits

Several companies—9 of 85 or 11% of our sample—made changes to executive retirement benefit plans. The most common approach was to reduce supplemental retirement benefits. This might involve closing SERPs to new participants, freezing future benefit accruals or modifying or capping the formula used to calculate benefits.

| Type of Change Reported in 2010 CD&A | No. of Cos. | % of Cos. (n = 9) |

| Froze DB SERP benefits | 4 | 44% |

| Scaled back DB SERP benefits | 2 | 22% |

| Enhanced supplemental DC benefits | 2 | 22% |

| Added retiree medical coverage | 1 | 11% |

Note: Changes to qualified plans available to all employees are not captured here.

Conclusions

In 2009 and 2010, companies continue to reevaluate – and modify – pay and governance practices. Risk assessment disclosure represents the biggest expansion in disclosure requirements. Another trend that emerged is the widespread use of clawbacks. Meanwhile, reductions in perks, change in control severance benefits, and executive retirement benefits, elimination of tax gross-ups, and enhanced stock ownership guidelines continue trends that have been evident for several years. These are all shareholder friendly developments that should improve the alignment between executive compensation and shareholders. We expect companies to continue to re-examine their programs as shareholders continue to demand good governance practices.

***

Please contact us at (212) 921-9350 if you have any questions about the issues discussed above or would like to discuss your own executive compensation issues. You can access our website at www.capartners.com for more information on executive compensation.

The component companies are large industry leaders. The total sample had median revenue of $25B, market cap of $37B and Total Shareholder Return (TSR) of 40% during 2009. The charts below include summary statistics by industry group. Practices at these leading companies are scrutinized closely by shareholders and the shareholder advisory groups. The responses of these companies to the financial strains in the economy during 2009 gives valuable insight into current practice and changes we expect to see in 2010.

What We Found

Highlights of our research results for the entire sample are below. Future CAP-Flashes will focus on particular industry groups and important topical areas, such as annual and long-term incentive design trends.

Compensation Strategy Changes

Outside of Financial Services, few companies reported changes to compensation strategy—i.e., the targeted pay positioning for executives and the targeted pay mix. Most stayed the course despite the challenging economic conditions in 2009.

Within the Financial Services group, most companies reported changes to compensation strategy, responding to their experience under TARP. Changes within the financial services industry include different pay mixes—examples include:

- Increased emphasis on fixed compensation by reducing incentive compensation and increasing base salary

- Increased emphasis on at risk, incentive compensation

- Majority of compensation delivered in restricted stock, deferred for 5 years

- Reduced portion of bonuses paid in cash and increased the portion of bonuses paid with deferred long-term awards subject to clawback

We expect Financial Services companies to continue to re- evaluate their compensation strategies as they exit TARP and emerge from the financial crisis and enter a more steady state.

Peer Groups Used For Benchmarking

Most companies did not make significant changes to their peer groups used for compensation benchmarking. Of those that did make changes, the majority of changes reported were primarily due to M&A activity in the Consumer Products, Insurance and Pharmaceutical industries. Others tweaked their selection criteria to focus more on companies in their industry and within a reasonable size range.

Base Salary Actions

Senior executive base salary actions continued to be restrained by the poor economy in 2009. Slightly more than half the sample did not increase or reduced salaries in 2009. Industry groups where salary freezes and reductions were widespread included Consumer Products, Health Care, Retail and Technology. Industries where salary increases were more common included Insurance and Pharmaceuticals. Merit increases were generally in the range of 2 – 3% when they were awarded.

| Type of Salary Change Reported in 2010 CD&A | No. of Cos. | % of Cos. (n = 85) |

| No Increase / Salary Freeze – All NEOs | 32 | 38% |

| No Increase / Salary Freeze – CEO Only | 6 | 7% |

| No Increase / Salary Freeze – Select NEOs | 1 | 1% |

| Salary Reduction – All NEOs | 4 | 5% |

| Salary Reduction – CEO Only | 1 | 1% |

| Salary Increase – All NEOs | 17 | 20% |

| Salary Increase – Select NEOs | 14 | 16% |

| Salary Increase – CEO Only | 1 | 1% |

| Salary Increase – TARP Related | 6 | 7% |

| Not Specified | 11 | 13% |

Note: Percentages do not add up to 100% due to multiple responses.

Annual Incentive Plan Design

Overall, 34 companies (40% of the full sample) disclosed making a change to their AIP design in 2009 or for 2010. While there was not a universal trend in the type of design changes being made, most companies are dealing with challenges in the goal setting process and maintaining meaningful performance linkages, linking rewards to the company’s ability to pay, and appropriately considering the impact of overall market conditions. In a nutshell, companies are trying to maintain a precise pay and performance calibration while also allowing for appropriate recognition of significant executive accomplishments.

The breakdown of reported AIP changes is as follows:

| Type of Change Reported in 2010 CD&A | No. of Cos. | % of Cos. Reporting Changes (n = 34) |

| Change in performance metrics used to fund awards | 15 | 44% |

| Increased target award opportunities | 9 | 26% |

| Reduced maximum award payout leverage | 4 | 12% |

| Added discretionary award component | 3 | 9% |

| Use of performance scorecard | 3 | 9% |

| New annual incentive plan (overhaul) | 2 | 6% |

| Other changes | 3 | 9% |

Note: Percentages do not add up to 100% due to multiple responses.

Change in Performance Metrics

Of the companies that changed their performance metrics and/or the mix of those metrics, a majority created a stronger linkage to corporate performance results and strategic priorities to support business changes forced by economic conditions. For example,

McKesson: For FY 2010, bonus goals need to significantly exceed the strategic plan to earn a target payout

Computer Sciences: Reduced the number of performance criteria to focus on key financial goals consistent with the company’s business strategy

T. J. Maxx – Eliminated divisional performance measures and focused on total company income

Sara Lee: Eliminated individual objectives and reallocated to corporate adjusted operating income goal

Merck: For 2010 incentive pool will be determined solely on company performance (as reflected by company scorecard)

There was no distinct trend in the changes made to the financial metrics used, though many changes included more emphasis on earnings, and to a lesser degree, revenue growth. Companies in the Insurance, Pharmaceutical and Retail industries made the most changes to metrics.

Discretion and Broad Performance Assessments

Some companies are increasing the role of discretion or broader retrospective performance assessment, to help ensure that significant market factors are considered at year end. For example, Genworth’s compensation committee uses discretionary judgment of performance against strategic objectives, including key financial criteria, to determine payouts. Microsoft’s compensation committee uses business judgment to help determine awards, and considers executive performance across a range of financial, operational, and strategic measures.

Another approach used by some companies includes use of a scorecard, which typically provides parameters for financial, operational, strategic, customer, and/or individual performance measurement. BNY-Mellon adopted such an approach to determine annual bonuses; and for 2010 Merck disclosed new incentive pool funding based on a company scorecard (solely company performance).

Changing Long-Term Incentive Practices

Most companies made changes to long-term incentive programs that either took effect in 2009 or will become effective in 2010—70% (60 out of 85) of companies reported changes. The most commonly reported changes involved changes to the mix of long-term incentive award vehicles granted and changes to the metrics used for long-term incentives. Here is a breakdown of what we found:

| Type of Change Reported in 2010 CD&A | No. of Cos. | % of Cos. Reporting Changes (n = 60) |

| Different mix of award vehicles | 33 | 55% |

| Different long-term performance metrics | 23 | 38% |

| Change in size of long-term award guidelines | 12 | 20% |

| Limits on dividend equivalents | 7 | 12% |

| Change in leverage in performance scales | 6 | 10% |

| Other changes | 9 | 15% |

Note: Percentages do not add up to 100% due to multiple responses.

Long-Term Award Mix

Among the companies that changed the mix of long-term award vehicles, two trends emerged. More than 50% of companies reporting a change in long-term award mix increased the emphasis on performance-based awards. Increased use of time-based awards – particularly among companies that had difficulty setting long-term financial goals during the recent period of economic uncertainty—was also common, but much less so. Finally, a few companies used options to a greater extent citing the difficulty in setting goals and attractive stock prices.

| Changes In Long-Term Incentive Award Mix | No. of Cos. | % of Cos. Reporting Changes (n = 33) |

| Greater emphasis on performance-based awards | 18 | 55% |

| Greater emphasis on time-based restricted stock/unit awards | 8 | 24% |

| Greater emphasis on options | 3 | 9% |

| Other | 4 | 12% |

Size of Long-Term Award Guidelines

Relatively few companies – only 14% of the total sample of 85 companies and 20% of the companies reporting changes to long-term programs—reported changing the size of long-term award target guidelines in 2009. Of the companies reporting a change, 67% decreased award guidelines and 25% increased award guidelines. One company reported migrating from fixed share guidelines to value-based guidelines, but did not indicate whether the change represented an increase or a decrease in value.

Long-Term Performance Metric Changes

Changes in long-term performance metrics were widespread. 25% of the total sample reported changing long-term incentives by adding new metrics; an additional 4% reduced the number of metrics used. Both relative and absolute TSR were selected as metrics by a number of companies. Return on equity/capital, revenue growth and cash flow were also popular choices.

| New Performance Metric | No. of Cos. | % of Cos. (n = 21) |

| Relative TSR | 5 | 24% |

| Absolute TSR of Stock Price Growth | 3 | 14% |

| Return on Equity or Capital | 4 | 19% |

| Revenue Growth | 3 | 14% |

| Cash Flow | 3 | 14% |

| Other Financial Metrics | 7 | 33% |

Note: Percentages do not add up to 100% due to multiple responses

Treatment of Dividend Equivalents and Other Plan Changes

Changes in the treatment of dividend equivalents was the most common plan design change reported. Seven companies moved to limit the payment of dividend equivalents until shares were earned or vested. Other design changes were more subtle, such as changes to the length of performance periods or the amount of leverage in performance scales.

Conclusions

Absent regulatory constraints, we did not see wholesale changes in 2009. Companies tended to stay the course in 2009 as the economic cycle bottomed out and the first signs of a recovery began to appear, but several clear trends did emerge. These include continued restraint on base salary increases, refinements to annual incentive and long-term incentive plan metrics and greater use of performance based long term incentives. These are all shareholder friendly developments that should improve the alignment between executive compensation and shareholders. We expect companies to continue to re-examine their programs as the economy improves and shareholders continue to demand performance and compensation program alignment.

***

Please contact us at (212) 921-9350 if you have any questions about the issues discussed above or would like to discuss your own executive compensation issues. You can access our website at www.capartners.com for more information on executive compensation.

Based on the dialogue we have seen among compensation committees, we believe the 2010 proxy season will demonstrate that a new level of responsibility has taken hold. Management and committees are struggling to ensure they are doing the right thing when it comes to compensation and that pay is closely aligned with performance. Additionally, some of the incentive program designs and governance practices imposed on financial services companies operating under TARP have had an impact on other industries.

Some of the early trends we are seeing in 2010 are detailed below.

Base Salaries

In 2009, roughly one-third of companies did not give salary increases. Many companies even cut salaries for executives, typically by 5-10%. With the economy showing early signs of a recovery, close to 90% of companies are planning for salary increases in 2010. Merit pools are expected to be lower than pre-recession levels, typically ranging from 2-3%. While many companies are providing salary increases, they will use these smaller pools more strategically, by targeting top performers and highest potential executives, and withholding increases to others.

RiskMetrics Group Problematic Pay Practices

While not a complete list, RMG views the following as problematic pay practices:

- Multi-year guarantees for salary increases, non-performance based bonuses, and equity compensation;

- Including additional years of unworked service that results in significant additional benefits, without sufficient justification, or including long-term equity awards in the pension calculation;

- Perquisites for former and/or retired executives, and extraordinary relocation benefits (including home buyouts) for current executives;

- Change-in-control payments exceeding 3 times base salary and target bonus; change-in-control payments without job loss or substantial diminution of duties (“single triggers”); new or materially amended agreements that provide for ‘modified single triggers’ (under which an executive may voluntarily leave for any reason and still receive the change-in-control severance package); new or materially amended agreements that provide for an excise tax gross-up (including “modified gross-ups);

- Tax reimbursements related to executive perquisites or other payments such as personal use of corporate aircraft, executive life insurance, bonus, etc;

- Dividends or dividend equivalents paid on unvested performance shares or units;

- Executive using company stock in hedging activities, such as “cashless” collars, forward sales, equity swaps or other similar arrangements; or

- Repricing or replacing of underwater stock options/stock appreciation rights without prior shareholder approval (including cash buyouts and voluntary surrender/subsequent regrant of underwater options)

In the financial services industry, given the impact of TARP and other regulatory initiatives, compensation is being re-mixed. Many financial service firms had increases to rebalance the mix between fixed and variable compensation. This helps avoid any perception that leveraged compensation packages encourage excessive risk-taking. In addition an annual risk assessment is becoming integral to the committee’s process across industries (this topic will be covered in the upcoming CAPflash on Risk Assessment).

Annual Incentives

Many companies’ experiences during two recessions within the last decade have highlighted the challenges with setting targets for incentive plan purposes. Beginning in 2009, many companies have started to incorporate a greater level of discretion in their annual incentive plans.

Companies found that strictly formulaic incentive plans sometimes failed to capture the true quality of the financial performance delivered. Additionally, Committees increasingly want the ability to improve the alignment between pay and performance. Providing for a level of discretion over incentive payouts allows Committees to recognize non-financial factors, individual performance and the challenges management faced in delivering the financial results on a retrospective basis.

For 2009 payouts, we expect to see an increased use of discretion by compensation committees, with more in-depth analysis of the factors influencing payout decisions. This may include a review of multiple financial metrics, analysis of performance relative to peers, strategic and operational results.

While results will vary by industry, we expect 2009 annual incentives payouts to exceed 2008 levels, when many companies paid zero or below target awards.

Long-term Incentives

In 2009, companies struggled to reconcile collapsing share prices with the need to recognize and reward their top performers and rising stars. Many companies did not grant equity as deeply or as broadly as they had in the past. In many cases, we saw a reduction in long-term incentive awards ranging from 10% – 30%. This decrease was partly due to efforts to manage annual share usage in a year with significantly lower stock prices In 2010, we are expecting grant values to level off or increase slightly as stock prices recover. We also expect to see a continued focus on performance-based long-term incentive plans and a decline in the use of or emphasis on stock options.

In 2010, individual differentiation will continue to be a key theme in long-term incentives as companies continue to manage their share usage and overall expense. The most dramatic examples occur deeper in the organization. At middle management levels, 100% may be eligible for awards, but typically 50%, and in some companies as few as 25%, actually receive awards.

Time-vested restricted stock and “salary stock” has become commonplace for companies operating under TARP. Outside of financial services, however, compensation committees have sharpened their focus on performance, employing a variety of performance-based awards. Shareholders and the various shareholder advocacy groups support these approaches, encouraging the trend.

Pay Mix

In 2009, many companies reviewed the mix of pay they offered. Companies want to ensure there is an appropriate balance between short and long-term compensation as well as fixed vs. variable pay. Within financial services, many companies re-balanced the amounts executives received in salary, annual cash incentives and equity. This rebalancing is intended to align the time horizon of compensation with the risk profile of the company and will vary by industry.

Clawbacks

Clawback provisions for annual and long-term incentives are becoming more common across industries. This is another example of a practice required by TARP spilling over into general industry. Clawbacks come in a variety of flavors. Some require employees to forfeit or reimburse compensation for a period of time if an executive engages in conduct that results in a restatement of financial results. Other clawbacks are fashioned more broadly, allowing companies to recoup compensation if results deteriorate over time for any reason. Providing for clawbacks helps further align pay and performance and mitigates the potential risks of executives making short-term decisions that have a detrimental impact on the company over time. Some companies, especially in financial services, are increasing the use of deferred compensation to make it easier to recoup compensation later, if the need arises.

Stock Holding Requirements

The requirement to hold stock for a period of time following vesting or exercise of options has become increasingly prevalent over the last few years, although still not a majority practice. Companies with such requirements generally ask executives to hold 50% to 100% of net shares for a period of one to three years, or even to retirement or beyond for a minority of companies. Stock holding requirements continue to be a focus for companies as they are viewed as another practice to mitigate risk in compensation programs. Stock ownership guidelines, most often expressed as a multiple of base salary, are common for most companies. Some companies are re-evaluating their stock ownership guidelines and denominating the guideline in shares as opposed to a multiple of salary as a response to the volatility in the market.

Change in Control Protections

Pressure from shareholder advisory groups and activist investors are leading to reductions in change in control protections. As companies review their programs, many are committing to eliminate gross-ups on 280(g) excise taxes going forward. Some of these companies are grandfathering this provision for existing participants, while select companies are eliminating them completely for all participants. A few companies are asking executives with contractual rights to gross-ups to waive them. These companies recognize that gross-ups are a red flag in the current environment and acknowledge that the potential cost to the company, or acquiring company, far exceeds the benefit to the executive. As companies eliminate the gross-up feature, some provide the executive with the choice to receive the full amount of their change in control benefits and pay the excise tax themselves or reduce the benefits to a level just below the level which would trigger the excise tax payment.

In addition to eliminating gross-ups, more companies are moving to double-trigger vesting on equity following a change in control (i.e., executive must be terminated without cause or terminate for good reason following the change in control).

Summary

The magnitude of the economic crisis increased the level of scrutiny of executive compensation practices over the past two years to unprecedented levels. The actions we have seen companies take in 2009 have been greatly impacted by the environment. As companies release their proxy statements in the next few months, we will get a better sense of the final decisions, but we believe that both senior leaders within companies and compensation committees are supporting a new level of responsibility and accountability.

Please contact us at (212) 921-9350 if you have any questions about the issues discussed above or would like to discuss your own executive compensation issues. You can access our website at www.capartners.com for more information on executive compensation.

We view the report as required reading for outside directors, senior management and HR professionals. The report amounts to a call for action for boards of directors and compensation Committees to re-examine their compensation programs to ensure that the link between pay and performance is strong and the programs reflect best practices and high governance standards.

The report recommends that executive compensation programs reflect the five guiding principles:

- Principle One – Paying for the right things and paying for performance

“Compensation programs should be designed to drive a company’s business strategy and objectives and create shareholder value, consistent with an acceptable risk profile and through legal and ethical means. To that end, a significant portion of pay should be incentive compensation, with payouts demonstrably tied to performance and paid only when performance can be reasonably assessed.” - Principle Two – The “right” total compensation

“Total compensation should be attractive to executives, affordable for the company, proportional to the executive’s contribution, and fair to shareholders and employees, while providing payouts that are clearly aligned with actual performance.” - Principle Three – Avoid controversial pay practices

“Companies should avoid controversial pay practices, unless special justification is present.” - Principle Four – Credible board oversight of executive compensation

“Compensation committees have a critical role is restoring trust in the executive compensation setting process and should demonstate credi ble oversight of executive compensation. To effectively fulfill this role, compensation committees should be independent, experienced, and knowledgeable about the company’s business.” - Principle Five – Transparent communications and increased dialogue with shareholders

“Compensation programs should be transparent, understandable and effectively communicated to shareholders. When questions arise, boards and shareholders should have meaningful dialogue about executive compensation.”

In addition to the guiding principles, the report contains concrete recommendations on how to implement effective executive compensation programs. Click on the link http://www.conference-board.org/pdf_free/ExecCompensation2009.pdf to access the full report of Conference Board?s Task Force on Executive Compensation.

Please contact us at (212) 921-9350 if you have any questions about the issues discussed above or would like to discuss your own executive compensation issues. You can access our website at www.capartners.com for more information on executive compensation.