Short-term, cash incentives continue to dominate the incentive-pay landscape at private companies according to salary and compensation survey research released in May 2018 by WorldatWork in partnership with Vivient Consulting.

“Spending on short-term incentives (STIs) increased modestly at private companies from 2015 to 2017, which reflects the tight labor market and competition for talent,” said Bonnie Schindler, partner and co-founder of Vivient Consulting.

Additional Key Findings from the WorldatWork-Vivient Survey

Private Company Compensation Survey Results:

- Spending on STIs increased to 6% of operating profit at median, from 5% in prior years.

- The prevalence of exempt, salaried employees and nonexempt (salaried or hourly) employees included in annual incentive plans increased in 2017. The biggest jump occurred for nonexempt employees. Approximately two-thirds of nonexempt employees are eligible for annual incentives, up from half in 2015.

- The majority of respondents consider their annual incentive plans to be only moderately effective, with plan communication, the level of discretion, goal setting and the risk-reward trade-off noted as areas for improvement.

The compensation survey Incentive Pay Practices: Privately Held Companies was conducted in December 2017 among WorldatWork members. The salary and pay survey is the fifth edition of the compensation report produced for privately held companies with the last report data released in 2015.

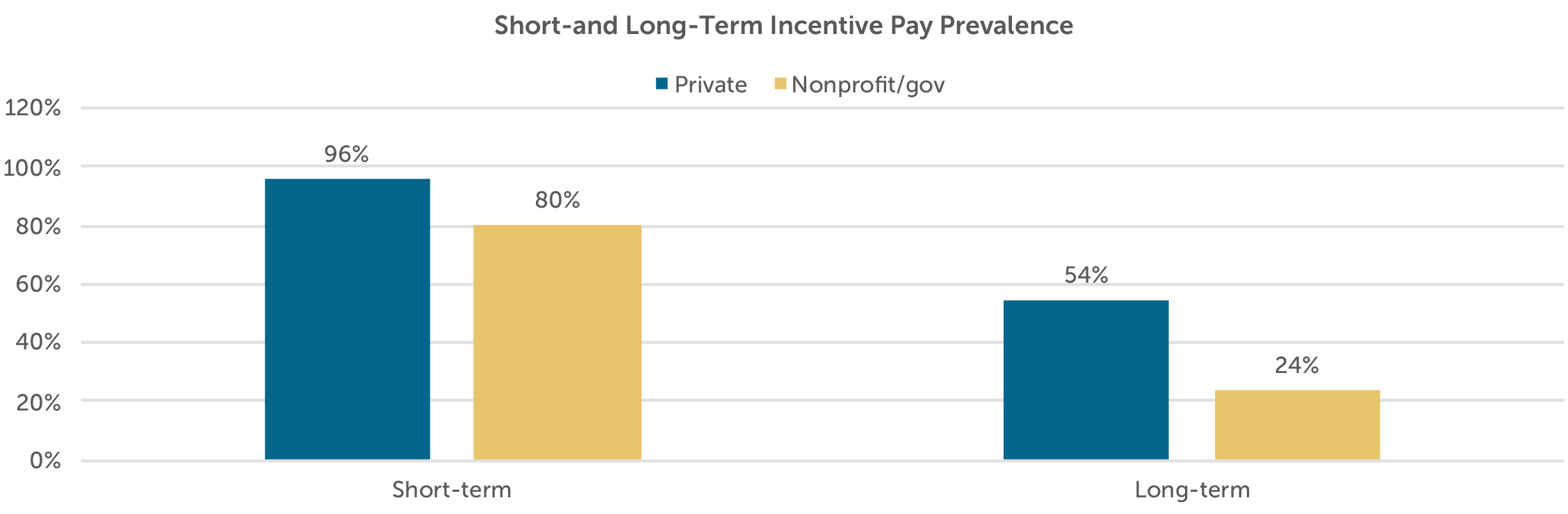

Short-term cash incentives continue to be popular motivational tools at U.S. privately owned companies, nonprofits and government organizations (NGOs), according to recent research conducted by Vivient Consulting and WorldatWork. The 2017 executive and employee compensation research spotlights short- and long-term incentive pay practices and is unique in its focus on entities that are not publicly traded.

Vivient and WorldatWork surveyed WorldatWork members in late 2017 and published the results in May 2018 in two reports:

- “Incentive Pay Practices: Privately Held Companies”

- “Incentive Pay Practices: Nonprofit/Government Organizations.”

This 2017 compensation survey provides a long-term view of typical incentive pay practices at private companies and NGOs as well as a snapshot of current and emerging pay practices and compensation trends.

Typical Incentive Pay Practices

What do typical incentive pay practices look like at non-publicly traded entities? Nearly all private, for-profit companies provide some form of short-term incentive (STI), with annual incentive plans (AIPs) being the most common type. Other STIs include:

- Discretionary bonuses

- Spot awards

- Team/small-group incentives

- Project bonuses

- Profit sharing.

The survey excludes sales and commission plans. Although not as prevalent as at for-profit counterparts, some form of short-term incentive compensation is used by 80% of the NGOs represented in the survey. And short term incentives at nonprofit organizations have increased in the decade that the survey has been conducted, as these organizations have to compete for talent with the for-profit sector.

On the long-term incentive (LTI) side, more than half of private companies provide LTIs, with multi-year, cash-based performance awards being the most common vehicles. Other types of long term compensation incentives include:

- Real equity, which includes restricted stock and stock options

- Phantom equity, which includes phantom stock and stock appreciation rights (SARs).

Long term incentives at private companies continue to be primarily reserved for executives. Private companies reported using LTIs for retention, alignment with long-term goals and market competitiveness. At NGOs, longer term pay incentives continues to be rare, but prevalence increased to 24% in 2017 from 16% in 2015. Future compensation research will determine whether this trend continues.

Incentive Pay Trend: Increase in Short Term Incentive Spending

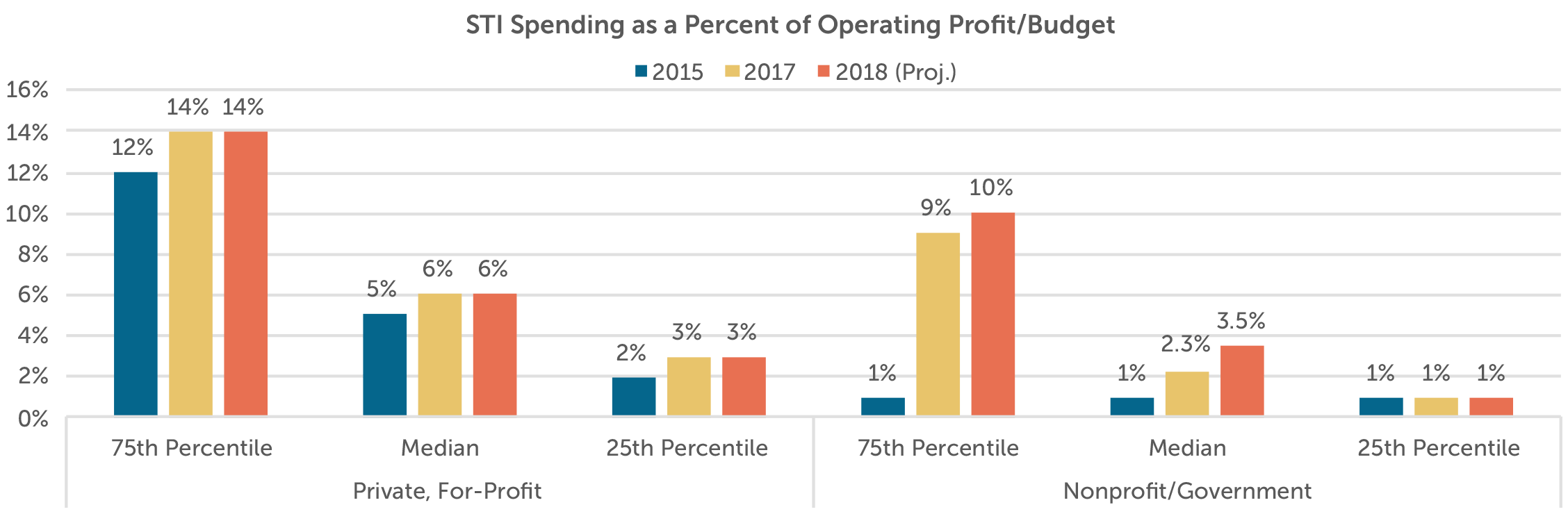

Private companies are spending more on STIs to motivate employees and compete for talent in a tight labor market. Private-company spending on short term incentives increased to 6% of operating profit at median from 5% in prior years. In addition, spending on STIs increased to 3% (from 2% in 2015) at the 25th percentile. At the 75th percentile, spending increased to 14% from 12% in 2015.

At NGOs, compensation survey respondents provided nonprofit estimated spending on short term incentives as a percentage of net organizational surplus (revenue minus expenses). In contrast to private companies, NGO spending on STIs slightly dropped at the median to 2.3% in 2017 from 3% in 2015. Similarly, reported spending by NGOs at the 75th percentile dropped to 9% in 2017 from 10% in 2015. However, participants expected STI spending as a percentage of their operating surplus to increase to 3.5% at median in 2018, as the budgetary outlook for 2018 appeared positive.

Incentive Pay Trend: Increased Annual Incentive Plan Eligibility

At private companies, the prevalence of exempt, salaried employees and nonexempt (salaried or hourly) employees included in Annual Incentive Plans increased in 2017. The biggest jump occurred for nonexempt employees. About two-thirds of nonexempt employees are now eligible for annual incentives, a significant increase from half in 2015. Annual incentive plan eligibility is now offered organization-wide at most private companies, reflecting the tight labor market and increased competition for talent. Eligibility for incentive plans is good news for employees who are now able to earn annual incentive awards and increase their overall compensation levels based on performance.

For nonprofit and government organizations, AIP eligibility increased for all organizational levels from manager/supervisor and above. Annul Incentive Plan eligibility decreased slightly for exempt employees and remained stable for nonexempt employees. The increased AIP eligibility for supervisory and management positions and above at NGOs indicates that these entities are using their limited annual incentive dollars within their salary and compensation budgets to compete with for-profit peers for top managerial and executive talent.

Incentive Pay Trend: Annual Incentive and Long-term Incentive Targets as a Percentage of Salary

For the first time in the Vivient/WorldatWork Private Company & NGO Compensation Survey’s history, participants were asked to provide typical AIP and LTI targets as a percentage of salary for broad position levels. For-profit, private companies that provide Annual Incentive Plans offer CEOs a median target award of 80% of salary. Target AIP awards decrease by approximately half for each broad position band below CEO. NGOs that provide Annual Incentive Plans tend to offer more modest target awards than for-profit counterparts.

|

Target Annual Incentive Award at Private Companies & NGOs (Percent of Salary) |

||

|

For-Profit Private |

NGO | |

| CEO | 80% | 40% |

| Other Executives/Officers | 40% | 25% |

| Managers/Supervisors | 15% | 10% |

| Exempt Salaried | 10% | Insufficient data |

|

Nonexempt Salaried and Hourly |

5% | Insufficient data |

NOTE: Excludes companies that do not offer Annual Incentive Plans

For Long Term Incentive Plans, private companies reported target long-term awards as a percentage of salary for executives. Data specific to private companies is difficult to find in published compensation surveys, which shows the value of this survey to WorldatWork members. The survey findings indicate that private companies offer an annual Long Term Incentive benefit that is approximately equal to the Annual Incentive Plan opportunity. This rule of thumb provides private companies that offer long-term incentives with a starting point for evaluating appropriate LTI levels for executives.

|

Target Long Term Incentive Awards at For-Profit Private Companies (Percent of Salary) |

|

| CEO | 80% |

| CEO’s Direct Reports | 50% |

| Vice Presidents/Officers | 30% |

NOTE: Excludes companies that do not offer Long Term Incentive Compensation

Incentive Pay Trend: Concerns About Annual Incentive Plan Effectiveness

Both private, for-profit companies and nonprofits reported a downward trend in the effectiveness of their Annual Incentive Plans. The risk-reward trade off was the biggest AIP weakness noted at both private companies and nonprofit/government organizations. This indicates that award payouts may not be adequately calibrated with results in terms of employee performance. For example, outstanding performance may result in only a moderate increase in the annual incentive payout. Conversely, below-target performance may result in a disproportionately small decrease from the targeted award level.

The level of discretion also was cited as a common weakness in Annual Incentive Plans, especially at private companies. The survey asked participants to provide information on strengths and weaknesses in the use of discretion. Private companies cited communication of the rationale for discretion, and the perception of fairness and consistency across the organization as the biggest weaknesses in the use of discretion. In contrast, NGOs do not seem to use discretion as much as private-company counterparts and did not report on specific weaknesses in its use. This lack of response may indicate that NGOs may see the need for a greater role for discretion in their AIPs, as it is more difficult to quantify performance at these organizations.

Incentive Pay Trend: More Cash-Based and Less Real Equity for Private-Company Long Term Incentives

With respect to Long Term Incentives, LTI performance awards — long-term cash plans, performance units and performance shares — continue to be the most popular vehicles at private companies. Because private companies do not have equity that is traded and valued on a stock exchange, cash-based plans are simpler and less expensive to design, operate and administer. The use of real equity decreased in 2017 after an uptick in the use of stock options in the 2015 survey. Private companies appear to now favor simpler, cash-based long-term incentives to avoid equity-related complexities such as valuation, liquidity and the dilution of ownership.

Incentive Pay at Family-Owned Private Companies

Nearly one-third of the private-company sample was family-owned, and these firms mirrored the broader private-company sample results although with some key distinctions:

- Higher short term incentive spending at family-owned companies

- Family-owned companies reported higher spending on short term incentives as a percentage of operating profit relative to the broader sample. Family-owned companies spent 10% of operating profit at median in 2017 and project an 8% STI budget for 2018. In contrast, the broader sample of private companies spends a median of 6% of operating profit annually.

- The higher spending on STIs at family-owned companies may be a strategy to attract external talent to help manage the business. Also, family-owned businesses typically provide a pay mix that is heavier on short-term cash compensation, as they tend to be more selective in providing longer term incentives.

- Lower use of long term incentives at family-owned companies

- Family-owned companies are less likely than the broader sample to offer an LTI plan. Only 44% of family-owned companies offer LTI plans, compared to 54% in the broader sample.

- Like the broader sample, family-owned companies favor performance awards, such as cash plans or performance units, over real equity or phantom equity that requires a company valuation.

Compensation Trends at Private Equity-Owned Companies

For the first time in this 2017 compensation survey research, respondents were asked to report whether private-equity firms own a stake in their companies. About a quarter of the respondents reported private equity investments in their companies and had some key distinctions in survey findings:

- Lower Short term incentive spending at private-equity owned companies

- Private equity-owned companies spend slightly less than the broader sample on STIs. These companies spend 5.5% of operating profit at median on STIs, in contrast to 6% for the broader sample.

- Private equity owners have the strategy of aligning executives’ economic interests with their own (i.e., creating a value realization event). As a result, executive compensation is focused more on LTIs than on short-term incentives.

- More long-term incentives and real equity ownership at private-equity companies

- Private-equity owned companies are more likely to provide LTIs than the broader sample. Almost two-thirds of private-equity-owned companies reported having an LTI plan.

- LTIs based on real equity — stock options and restricted stock — are favored by private equity investors, as these vehicles align the incentives of management with the shareholders and provide a retention mechanism. Also, private-equity owned companies tend to grant LTIs deeper into the organization versus the broader survey sample.

Where Private Company and NGO Compensation Preferences Are Trending

Private companies and NGOs continue to favor short-term and cash-based incentives. Future compensation research by Vivient Consulting and WorldatWork will focus on whether the tight labor market and competition for talent continue to drive non-publicly traded entities to spend more on incentives and broaden incentive participation across more employees.

Companies use annual bonuses as a tool to reward executives for achieving short-term financial and strategic goals. Setting appropriate annual performance goals is essential to establishing a link between pay and performance. Goals should achieve a balance between rigor and attainability to motivate and reward executives for driving company performance and creating returns for shareholders.

Key Takeaways:

- Based on our analysis of actual incentive payouts over the past 6 years, the degree of difficulty, or “stretch”, embedded in annual performance goals translates to:

- A 95% chance of achieving at least Threshold performance

- A 75% chance of achieving at least Target performance

- A 15% chance of achieving Maximum performance

- This pattern indicates that target performance goals are challenging, but attainable, and maximum goals are achievable through highly superior performance

- The majority of companies use two or more metrics when assessing annual performance

- Annual incentive payouts have been directionally linked with earnings growth over the past 6 years

Summary of Findings

Plan Design

For the purposes of this study, we categorized annual incentive plans as either goal attainment or discretionary. Companies with goal attainment plans define and disclose threshold, target and maximum performance goals and corresponding payout opportunities. Alternatively, companies with discretionary plans do not define the relationship between a particular level of performance and the corresponding payout. Discretionary programs provide committees with the opportunity to determine payouts based on a retrospective review of performance results.

| Annual Incentive Plan Type | |||

| Industry | Sample Size | Goal Attainment | Discretionary |

| Auto | n= 8 | 100% | 0% |

| Consumer Discretionary | n= 10 | 90% | 10% |

| Consumer Staples | n= 12 | 67% | 33% |

| Financial Services | n= 12 | 17% | 83% |

| Healthcare | n= 9 | 89% | 11% |

| Industrials | n= 14 | 71% | 29% |

| Insurance | n= 12 | 67% | 33% |

| IT | n= 12 | 83% | 17% |

| Pharma | n= 10 | 80% | 20% |

| Total | 72% | 28% | |

Consistent with the findings from our study conducted in 2014, 72% of sample companies have goal attainment plans. Our study focuses on these companies.

Performance Metrics

Most companies (61%) use 3 or more metrics to determine bonus payouts. This reflects a shift from 2014, where 48% of companies used 3 or more metrics. Companies annually review metrics to ensure that they align with the business strategy.

Many companies use financial metrics such as revenue and profitability, which are indicators of market share growth and stock price performance. Some bonus plans also include strategic metrics, which incentivize executives to achieve goals that may contribute to long-term success, but may not be captured by short-term financial performance. Companies in the pharmaceutical industry often use strategic goals, such as pipeline development. Similarly, companies with large manufacturing operations often use quality control metrics.

| # of Metrics Used in Goal Attainment Plan | ||||

| Industry | 1 Metric | 2 Metrics | 3 Metrics | 4+ Metrics |

| Auto | 13% | 13% | 25% | 50% |

| Consumer Discretionary | 11% | 44% | 45% | 0% |

| Consumer Staples | 0% | 37% | 38% | 25% |

| Financial Services | 0% | 50% | 50% | 0% |

| Healthcare | 0% | 38% | 12% | 50% |

| Industrials | 20% | 40% | 20% | 20% |

| Insurance | 37% | 13% | 25% | 25% |

| IT | 10% | 30% | 40% | 20% |

| Pharma | 0% | 0% | 63% | 37% |

| Total | 11% | 28% | 34% | 27% |

Pay and Performance Scales

Compensation committees annually approve threshold, target, and maximum performance goals, and corresponding payout opportunities, for each metric in the incentive plan. Target performance goals are typically set in line with the company’s internal business plan. Executives most often earn 50% of their target bonus opportunity for achieving threshold performance and 200% for achieving maximum performance. Actual payouts are often interpolated between threshold and target and target and maximum.

Annual Incentive Plan Payouts Relative to Goals

All Companies

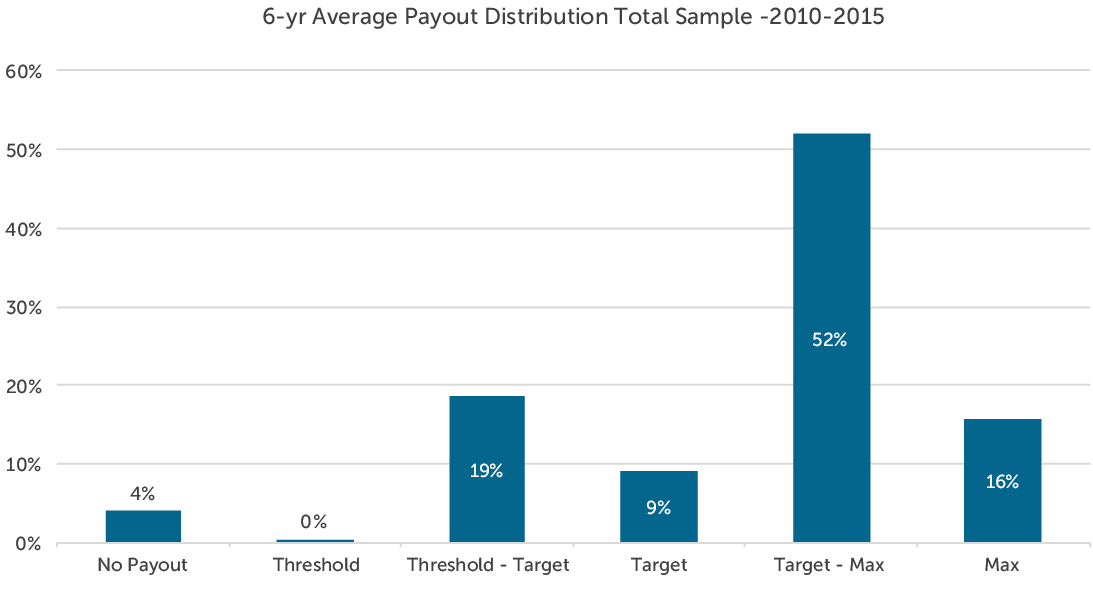

Based on CAP’s analysis, companies paid annual bonuses 95% of the time. Payouts for the total sample are distributed as indicated in the following charts:

This payout distribution indicates that committees set annual performance goals with a degree of difficulty or “stretch” such that executives have:

- A 95% chance of achieving at least Threshold performance

- A 75% chance of achieving at least Target performance

- A 15% chance of achieving Maximum performance

From 2010-2015, no more than 10% of companies failed to reach threshold performance in any given year. By comparison, in both 2008 and 2009, which were challenging years, approximately 15% of companies failed to reach threshold performance goals.

When looking back over 8 years (2008-2015), companies achieved at least threshold and target performance with slightly less frequency. Based on CAP’s analysis of this 8-year period, executives have:

- A 90% chance of achieving at least Threshold performance

- A 70% chance of achieving at least Target performance

- A 15% chance of achieving Maximum performance

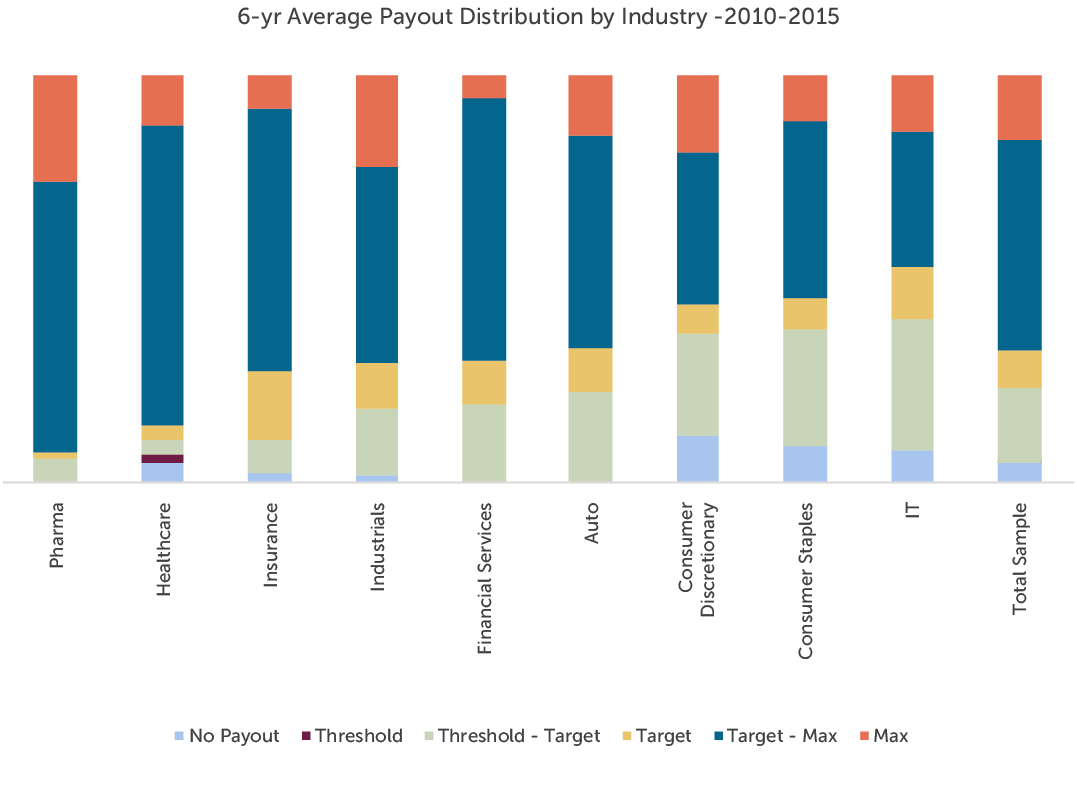

By Industry

Pharmaceutical and healthcare companies have paid at or above target more frequently than companies in any other industry over the past 6 years. Both industries have experienced significant growth over the period in part due to consolidation. The companies in the IT, Consumer Discretionary and Consumer Staples industries tend to pay below target at a higher rate. Average payouts for each industry are distributed as indicated in the following chart:

Relative to Performance

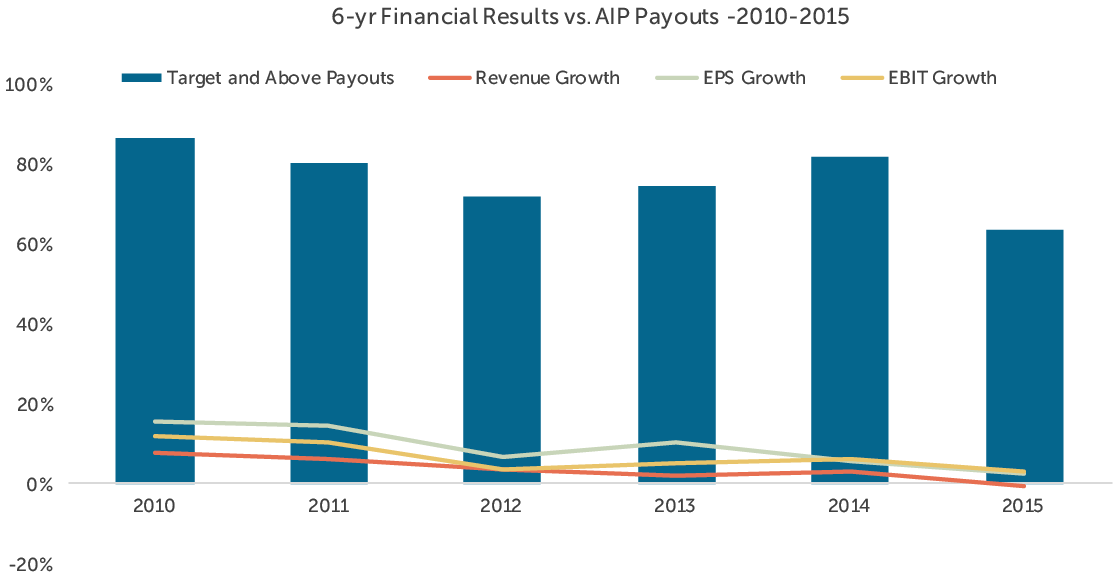

CAP reviewed the relationship between annual incentive payouts and company performance with respect to three metrics: revenue growth, earnings per share (EPS) growth and earnings before interest and taxes (EBIT) growth. While payouts were generally aligned with revenue and EPS growth, they most closely tracked with EBIT growth over the period studied (2010-2015). Companies may seek to align bonus payouts with operating measures, such as EBIT, as they capture an executive’s ability to control costs and improve operational efficiency.

The chart below depicts the relationship between median revenue, EPS, and EBIT growth and target and above annual incentive payouts among the companies studied.

Conclusion

In the first quarter of 2017, committees will certify the results and payouts for the fiscal 2016 bonus cycle and approve performance targets for fiscal 2017. Given the uncertain economic outlook following the 2016 presidential election, establishing performance targets for 2017 may be more challenging than usual. Companies may choose to use a range of performance from threshold to maximum to build flexibility into their plans given the unpredictable environment. Our study of annual bonus payouts over the past 6-8 years supports setting goals such that the degree of difficulty, or “stretch”, embedded in performance goals translates to:

- A 90-95% chance of achieving at least Threshold performance

- A 70-75% chance of achieving at least Target performance

- A 15% chance of achieving Maximum performance.

Companies should continue to set target performance goals that are challenging, but attainable and maximum goals that are achievable through outperformance of internal and external expectations – therefore, establishing a bonus plan that is attractive to executives and responsible to shareholders.

Methodology

CAP’s study consisted of 100 companies from 9 industries, selected to provide a broad representation of market practice across large U.S. public companies. The revenue size of the companies in our sample ranges from $18 billion at the 25th percentile to $70 billion at the 75th percentile.

CAP analyzed the annual incentive plan payouts of the companies in the sample over the past 6-8 years to determine the distribution of incentive payments and the frequency with which executives typically achieve target payouts. In this analysis, CAP categorized actual bonus payments (as a percent of target) into one of six categories based on the following payout ranges:

| Payout Category | Payout Range |

| No Payout | 0% |

| Threshold | Up to 5% above Threshold |

| Threshold – Target | 5% above Threshold to 5% below Target |

| Target | +/- 5% of Target |

| Target – Max | 5% above Target to 5% below Max |

| Max | 5% below Max to Max |

This episode of NACD BoardVision examines the expectations that boards face when setting annual compensation goals. Christopher Y. Clark, Publisher of NACD Directorship Magazine and Kelly Malafis, Partner at Compensation Advisory Partners discuss best practices for rigorous goal setting.

Setting goals for long-term incentives has been a persistent problem for companies and Compensation Committees ever since the reliance on long-term performance plans has increased. However, the results of the recent election take the uncertainty to an entirely new level, right around the time when companies are starting to think about setting goals for their upcoming long-term incentive cycle. Examples of challenges various industries will face include:

Energy & Utilities

- Volatility of energy prices given the views on natural gas and oil

- Environmental regulations (i.e. carbon dioxide emissions)

- Traditional sources of energy vs. renewables

Financial Services

- Dodd-Frank implications

- Movement in interest rates

- Return of Glass-Steagall

Industrial and Materials Companies

- Investment in large infrastructure projects

- Renegotiation of trade deals and increased tariffs on goods

None of the above even touches on the implications for businesses if the administration implements a broad-reaching immigration initiative which can have implications on labor costs or if President-elect Donald Trump is successful at dramatically lowering the corporate tax rate.

In many ways, it is similar to the level of uncertainty companies and Boards were dealing with during and immediately following the financial crisis. As Compensation Committees and management plan for 2017 and beyond, a challenge will be setting goals in a company’s 1- and 3-year incentive plans. As such, Compensation Advisory Partners (“CAP”) outlines four things to think about when setting goals to avoid unintended outcomes and maximize flexibility and accountability.

- Scenario Testing – Run scenarios to test sensitivities and potential outcomes. For example, test what will happen if energy prices go up/down/stay flat and what will happen to payouts under the varying scenarios. Discuss this analysis with the Compensation Committee and establish guiding principles for what is a reasonable payout under the varying scenarios.

- Retrospective analysis – Over periods of uncertainty, companies can meet or miss their goals for many reasons. If the next four years are as volatile as currently expected, Compensation Committees should encourage management to do a retrospective analysis at the end of each performance cycle comparing actual performance to expected performance when goals were set. For example, if the company ultimately delivers $3.00 EPS and the goal was $2.50, did the company get there through true outperformance, because of changes in non-controllable events or because corporate tax rates declined? This retrospective analysis can help guide the Compensation Committee in determining how challenging the goals wound up being and if appropriate, make necessary adjustments to payouts.

- Wider range – As the ability to predict the future diminishes, it can often be helpful to rethink the range around target that justifies a threshold and maximum payout. For example, if a company has a high level of confidence in the ability to achieve planned performance, then they might set a relatively narrow range around target (e.g., 95% of plan for threshold and 105% of plan for maximum). However, if the company has less confidence in the ability to set its plan, a wider range (e.g., 90% of plan for threshold and 110% of plan for maximum) may be more appropriate such that deviation from plan does not have as much as much of an impact on payouts.

- 162m Umbrella Plan – With significant uncertainty it may be challenging to predict what, if any, adjustments a Compensation Committee may want to make to their annual or long-term performance plan. This would be a good time to consider implementing, if you have not already, a 162m umbrella plan to provide the Compensation Committee with flexibility to make adjustments and maintain tax deductibility. An umbrella plan is a structure whereby a bonus is effectively “over-funded” for the Named Executive Officers (“NEOs”) such that the Compensation Committee can determine the final payout with some flexibility as long as the final payout is below the umbrella funded amount. For example, in order to qualify as performance-based compensation, a company could establish a maximum to be paid equal to 3% of net income and specify a percentage of the award pool for the each NEO (excluding the CFO). The Compensation Committee then retains negative discretion to pay less than the maximums established. These umbrella plans are very common for annual incentives, but are less common for long-term plans, though this might be a good time to consider whether one might be appropriate.

There are many other ways of addressing uncertainty around goal setting, but these four tips should help maintain a pay for performance structure, hold management accountable and provide Compensation Committees with appropriate flexibility.

Partner Bertha Masuda discusses special considerations for short-term incentives for companies under $500 million in revenue with WorldatWork.

Principal Bonnie Schindler discusses the compensation survey research conducted by Vivient and WorldatWork around incentive pay practices for private, non-profits and government entities.