DOWNLOAD A PDF OF THIS REPORT pdf(0.1MB)

Contact

Eric HoskenPartner [email protected] 212-921-9363 Daniel Laddin

Founding Partner [email protected] 212-921-9359

Larry Fink, the CEO of BlackRock, issued a letter to the chief executive officers of the S&P 500 challenging each to disclose a strategic framework for long-term value creation that has been reviewed and approved by their board. The strategic framework would highlight for shareholders how the company expects to drive value creation and discuss the competitive threats and strategic opportunities that the company faces. Mr. Fink’s letter also highlights the importance of identifying metrics that track performance against this framework and incentives that reward for long-term success.

We believe Mr. Fink raises an important point on linking incentives to business strategy. A clearly communicated business strategy would help to avoid pitfalls that we see frequently today. These include incentives that are designed primarily to respond to pressure from proxy advisory firms, often driving a “one size – fits all” approach or encouraging short-term thinking.

“We are asking that every CEO lay out for shareholders each year a strategic framework for long-term value creation. Additionally, because boards have a critical role to play in strategic planning, we believe CEOs should explicitly affirm that their boards have reviewed those plans. BlackRock’s corporate governance team, in their engagement with companies, will be looking for this framework and board review.”

Larry Fink, BlackRock CEO

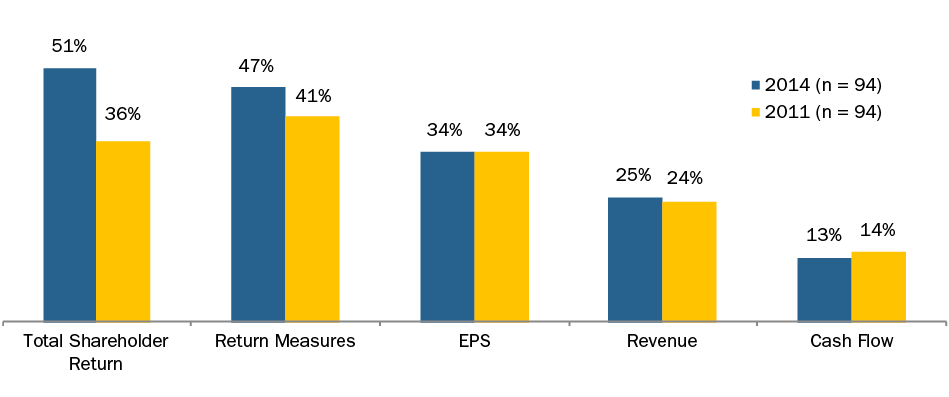

As highlighted by our articles Are You Rewarding Short-Termism? in The Corporate Board and Balancing pay for performance with shareholder alignment in the Ethical Boardroom, it is important that compensation, in particular long-term incentive compensation, links directly to the company’s strategy. We agree that providing shareholders with a voice on compensation programs through Say on Pay has been beneficial, but we have observed a chilling effect on creative compensation programs. Today most public companies are very reluctant to be an outlier on compensation. If we look at CAP’s sample of 100 large market cap companies, 51% use Total Shareholder Return (TSR) and 34% use EPS as metrics in their long-term incentive plans. Are these universal metrics appropriate in almost any situation? We question that premise. Why do so many companies have similar metrics when they have unique business strategies, operate in diverse industries and are positioned at different points in their lifecycle?

The good news is that we have observed modest increases in the use of return metrics, from 41% in 2011 to 47% in 2014 (e.g., return on assets, return on capital and return on equity). In several cases, activist investors have intervened to champion the adoption of return metrics. Traditional institutional investors with concerns over the effectiveness of corporate business strategies have also been vocal in encouraging companies to focus on returns. Both camps frequently push companies to move to adopt balanced metrics that encourage profitability in combination with growth as opposed to growth alone.

The chart below provides a snapshot of how long-term incentive plan metrics have evolved over time. Use of TSR has grown most since 2011, from 36% to 51% and this is after dramatic increases prior to 2011. We believe this is the direct outcome of the influence of proxy advisory firms, who have pushed hard on companies to incorporate relative TSR in their programs. The good news is that since 2011, the number of companies relying on a single metric has declined, with over 1/3 of companies using 3 or more metrics which may indicate they are tailoring plans more to their specific situation.

|

# of Metrics |

2011 |

2014 |

|

1 |

33% |

26% |

|

2 |

40% |

37% |

|

3 or More |

27% |

37% |

While EPS and TSR may make sense for many companies, companies should consider various factors when selecting measures, including:

- Is relative TSR the best answer for your company? We see it as an outcome-oriented metric that lacks a clear linkage to strategic priorities and is not well suited to driving behaviors that create shareholder value.

- Does over-reliance on TSR encourage risk-taking behaviors? Companies may make decisions that drive TSR in the short-term (e.g., share buybacks or higher dividends), rather than identifying better uses of capital that can lead to sustained long-term growth.

- Does an EPS metric create an incentive to buy back shares rather than re-investing for growth? Financial experts have mixed views on the utility of share buybacks. The jury is still out.

- Are the current time horizons for TSR performance optimal? Almost all plans measure TSR over 3 years. Why is a 3-year time frame the default for most companies? Since TSR is usually defined as a relative metric, eliminating the need to set goals in advance, should companies be evaluating longer timeframes that align with their business cycles?

- If relative TSR is your company’s metric, where are you in the cycle? Companies and boards need to ask and analyze whether relative TSR goals will pay out for sustained long-term stock price appreciation or for volatility in relative stock price performance. Companies and boards need to understand whether the stock is only recovering from earlier losses that occurred prior to the start of the performance period.

We don’t believe that either EPS or TSR are inherently poor metrics. In many cases, it makes sense for companies to incorporate these metrics into their overall incentive framework. However, it is critical to determine if these metrics are right for a particular company at a -particular time in its life cycle. Keep in mind that long-term incentives are the largest component of pay for many executives. As companies and boards design long-term incentives, they should consider the following questions:

- Does the compensation program support our strategy and do the metrics and goals align with our long-term business plan?

- Can we communicate clearly and succinctly how the program ties to our strategic framework for both shareholders and program participants?

- What behaviors, good or bad, could the design encourage? For example:

- Does it send clear signals throughout the organization on the strategic priorities?

- Is short-term upside emphasized at the expense of long-term sustained value?

- Do we encourage growth at the expense of returns that exceed our cost of capital?

- Does the program encourage excessive or inappropriate risk-taking?

- For metrics other than TSR, will achievement of goals lead to company and shareholder value creation?

- Are there alternative metrics, including strategic metrics (e.g., increase in market share, diversification of revenue, etc.) that might be better indicators of successful execution of the strategy?

Overall, we think Mr. Fink’s commentary on the importance of defining and communicating a company’s strategic framework for value creation serve shareholders well. His comments point to a fundamental principle of compensation design: incentive compensation should be used to reward the company’s success in achieving its strategy and creating long-term value for shareholders. The performance measures used to determine incentive compensation need to track progress on the strategy over the near term and over the long-term. We believe we will see a migration in this direction as long-term incentives evolve, companies continue to dialogue with their shareholders and perhaps as they enhance disclosure around their strategic framework as Mr. Fink suggests.